- LME lead prices up 1.7% w-o-w

- SCCL-Altmin JV to build India’s first lithium refinery

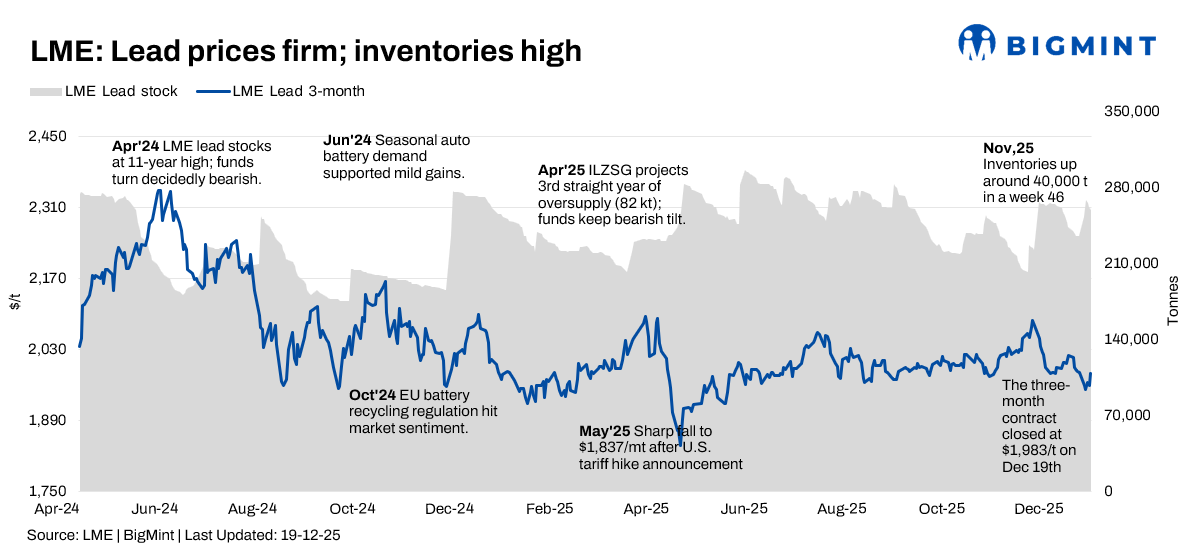

The London Metal Exchange (LME) lead market traded in a narrow, mildly firmer range over 15-19 December 2025, as a softer US dollar and seasonal battery demand helped prices stabilise after earlier weakness, while the well-signalled refined surplus and high inventories continued to cap the upside. Overall sentiment remained cautious but slightly improved versus early December, with traders still focused on large LME stocks and modest demand growth in traditional lead‑acid battery applications.

Price trends

LME lead cash prices rose from about $1,904.50/t on 15 December to roughly $1,913/t by 18 December and approached the $1,937/t area by 19 December, implying a w-o-w gain of around 1.7%. The LME 3-month lead contract followed a similar path, drifting up from the low- $1,985/t on 15 December toward the mid-$1,980/t by 19 December, leaving a modest positive weekly change while still trading slightly below late-November levels

Inventory analysis

LME lead stocks remained high in absolute terms and ended the week slightly higher. Inventories rose from 252,475 t on 15 December to a peak of 268,450 t on 16 December before easing to 258,625 t by 19 December, a net w-o-w increase of 6,150 t or about 2.4%. Even with this modest build, combined on‑warrant and off-warrant inventories are still estimated above 400,000 t, underscoring a structurally oversupplied refined market and leaving visible stocks well above historical averages.

SHFE lead trend

On the Shanghai Futures Exchange (SHFE), the most-traded lead futures contract posted a mild rebound from recent lows. The January 2026 contract oscillated around CNY 16,700-16,900/t, with a weekly gain of about 0.4% as smelter production cuts and lower social inventories offered some cost support. Even so, prices remained close to multi‑month troughs, as persistent concerns over China’s property sector and gradual EV-related substitution for conventional lead-acid batteries continued to weigh on demand expectations.

NavPrakriti plans tie-ups with 150+ battery firms and OEMs

NavPrakriti, a Kolkata-based lithium-ion battery recycling and refurbishment company, has announced plans to partner with over 150 battery manufacturers and original equipment manufacturers (OEMs) over the next three years to build a nationwide network for collection, recycling and refurbishment of spent Li-ion batteries. The initiative will support India’s Extended Producer Responsibility (EPR) framework and aims to enhance safe, efficient and environmentally responsible battery management as battery demand and waste grow.

SCCL-Altmin JV to build India’s first large-scale lithium refinery

State-run Singareni Collieries Company Limited (SCCL) has partnered with Hyderabad-based Altmin Pvt Ltd to establish India’s first large-scale, battery-grade lithium refinery in Telangana with a INR 2,250 crore investment. The joint venture will build a 30,000 t/year lithium carbonate refinery expected to commence operations by 2027, bolstering domestic battery raw material production, reducing import dependence, and supporting the EV and clean energy ecosystem.

Outlook

Across LME, MCX and SHFE, lead enters late December with a neutral-to-slightly-firmer tone: prices have lifted modestly from mid‑month lows, but the sizeable LME inventory overhang and 2025 surplus forecasts still cap any sustained rally. Unless deeper mine or smelter disruptions emerge or macro conditions improve more decisively, lead is likely to remain range‑bound with a slight downside skew, and rallies are expected to be used primarily for hedging rather than to mark the start of a new bullish phase.

Leave a Reply