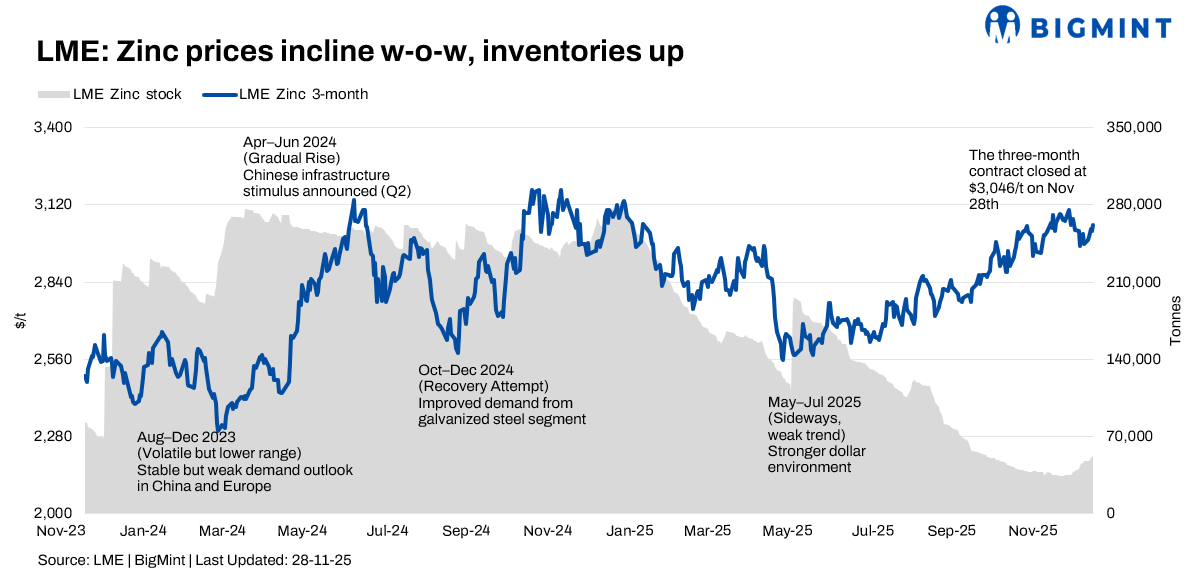

- LME zinc cash prices gain 3.79% w-o-w

- LME zinc stocks continued to trend higher through late November

Zinc prices on the London Metal Exchange (LME) firmed in the week ended 28 Nov, with prices stabilising and edging higher after a sharp correction recorded in the previous week. Prices were supported by dip‑buying and short‑covering, even as a steady build‑up in exchange inventories and signs of a refined market surplus capped the upside.

Market participants continued to weigh prompt availability against a softening macro backdrop and mixed signals from China, where refined zinc exports are expected to remain relatively strong.

Price trends

LME zinc cash prices rose from about $3,136/t on 24 Nov to about $3,255/t by 28 November, gaining roughly 3.79%. The three-month contract increased from $2,992/t to $3,046/t, up around 1.8%, consolidating after mid-November lows near $2,980/t. Despite the rebound, values stayed below the early-November high near $3,300/t, reflecting caution around demand linked to infrastructure and datacenter sectors.

Inventory analysis

LME zinc stocks continued to rise through late November, moving from $47,425 t on 24 Nov to 51,750 t by 28 Nov, an increase of about 9% over the week and close to 52% higher than 33,825 t recorded on 3 Nov.

This inventory buildup signalled some easing in the narrowing gap between demand and available stocks recorded earlier, although stocks remained low by historical standards. Stocks averaged about $148,000 tonnes in 2023-24. Concurrent industry data indicating a refined zinc surplus of around 0.1–0.15 Mnt for the first three quarters of 2025 further limited the immediate upside for prices.

MCX zinc trends

On the MCX, near‑month zinc futures traded roughly between INR 297,000/t and INR 303,000/t in the week, moving from about INR 297,250/t on 24 November to close near INR 303,150/t on 28 November, a week‑on‑week rise of around 1.9%. The intraday strength seen on 27-28 November reflected buying on dips in line with the modest LME recovery and steady demand from galvanising and alloy‑using sectors.

SHFE zinc trend

On the Shanghai Futures Exchange, the main zinc contract fluctuated around the low‑RMB 22,000/t region, edging up from roughly RMB 21,900/t on 24 November to about RMB 22,200/t by 28 November, a gain of around 1.4%. Social inventories in China eased slightly, while SHFE‑registered stocks showed limited net change, pointing to a broadly balanced domestic market after earlier destocking. With the SHFE-LME arbitrage staying relatively tight and Chinese smelters still incentivised to export, domestic prices continued to be shaped by both local demand and export economics

Santacruz Silver – stable Q3 2025 zinc output

Santacruz Silver recorded 21,581 t of zinc in Q3 2025 and 63,449 t year-to-date. Strong performance from Caballo Blanco, Zimapán and San Lucas offset disruptions at the Bolívar mine caused by the May water-inflow event. Remediation is progressing, with full access expected in 2026, reinforcing Santacruz’s role as a key zinc supplier.

Silver Mountain Resources – high-grade results at Reliquias Project

Silver Mountain Resources reported 10-13% zinc grades from channel sampling at the Ayayay and Matacaballo veins. The Reliquias Project hosts 28,800 t of measured & indicated zinc resources and 26,100 t inferred. Commercial production remains on schedule for Q3 2026, supporting medium-term zinc supply growth.

Outlook

Zinc markets consolidated with 1-2% gain at the end of November. Markets trends for December depend on LME stocks staying near 51,750 t, Chinese export strength, and macro trends. Meanwhile, tight mine supply could continue to support dip-buying in the month.

Leave a Reply