- Japanese port inventories fall to lowest in a decade

- Good Western-origin metal availability remains tight

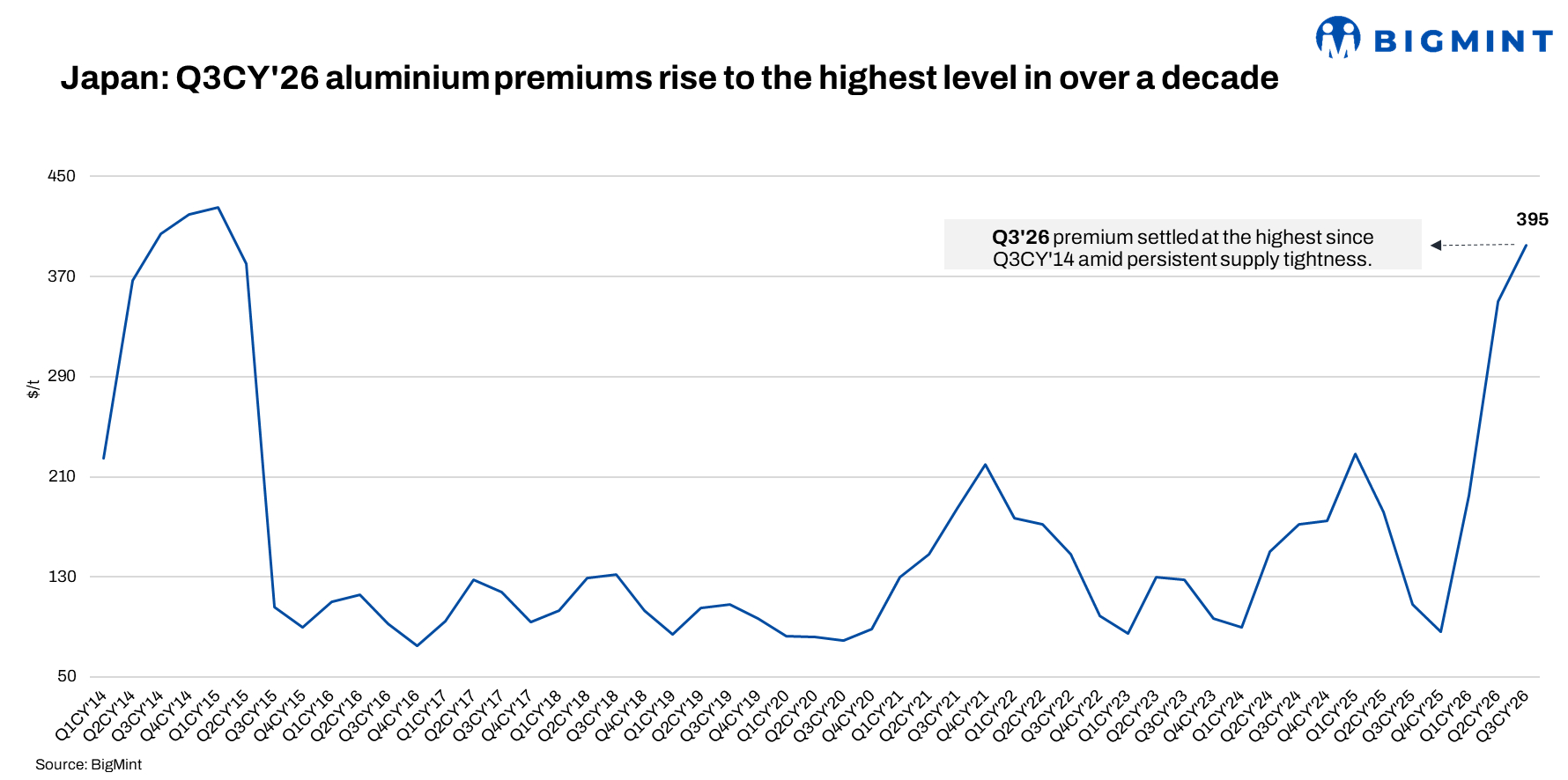

Japan’s Q3CY’26 aluminium premium settled at $395/t CIF Japan, up 13% from $350/t in Q2, marking the highest quarterly premium in more than a decade and the strongest level since Q3CY’14 ($404/t). The settlement was concluded through 10 transactions covering a minimum monthly volume of 15,500 t.

The increase was primarily driven by continued uncertainty surrounding Middle East aluminium supply, despite easing geopolitical tensions and the faster-than-expected restart of Emirates Global Aluminium’s (EGA) Al Taweelah smelter. Market participants believe that while production is recovering, the availability of Good Western-origin aluminium is likely to remain constrained throughout the quarter.

Negotiations also reflected a gradual softening in seller expectations. Initial offers were heard as high as $480/t CIF Japan, before declining to $440/t, with buyers eventually settling at $395/t as concerns over prolonged supply tightness outweighed expectations of improving exports from the Middle East.

Physical market fundamentals also remained supportive. Japanese port inventories declined to 238,000 t at the end of May, the lowest level since 2012, reflecting lower arrivals and continued inventory drawdowns amid the backwardated LME market structure. Meanwhile, Japan’s end-user aluminium demand remained broadly stable, with no significant improvement reported across major consuming sectors.

Looking ahead, market participants expect Q3 premiums to remain well supported as Middle East smelters continue their gradual recovery. However, premiums could begin to moderate in Q4CY’26 if production at EGA normalises further, export flows improve and additional supply from India, Indonesia and China becomes increasingly available in the Asian market.

Leave a Reply