- Crude steel output falls for 4th straight year to 57-year low, driving scrap surplus

- Freight advantages, steady cargo availability draw in Southeast Asian buyers

- Taiwan, South Korea reduce intake on weak steel demand, high inventories

Morning Brief: Japan’s ferrous scrap exports scaled a five-year peak in CY’25, as crude steel production fell for the fourth consecutive year, reaching a 57-year low last seen in 1968. Lower domestic scrap consumption forced recyclers to redirect supply towards faster-growing Southeast Asian and Bangladeshi markets.

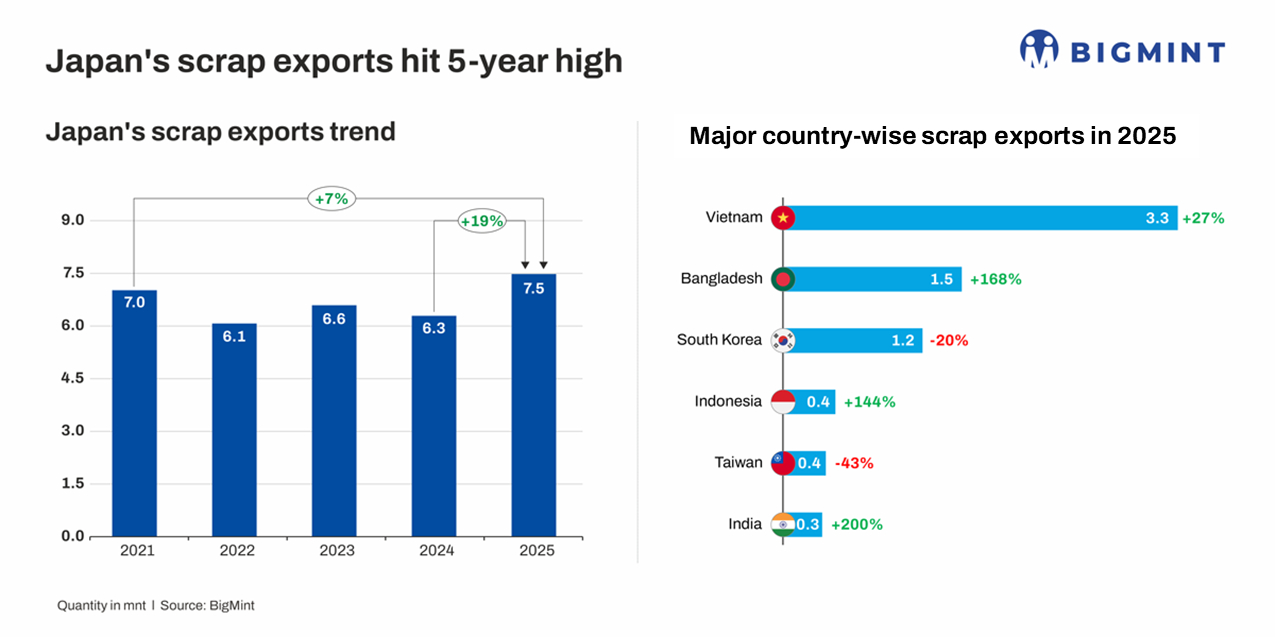

Japan’s total ferrous scrap exports rose 19% y-o-y to 7.5 million tonnes (mnt) in CY’25 from 6.3 mnt in CY’24, as per data compiled by BigMint. Vietnam continued to be the leading importer, while Bangladesh overtook South Korea and Taiwan to emerge as the second-largest buyer.

Notably, Southeast Asia emerged as the key demand centre in CY’25, while Northeast Asian buyers scaled back imports. Higher steel output and expanding electric arc furnace (EAF)-based production supported stronger imports in Vietnam and Indonesia. In contrast, Taiwan and South Korea reduced purchases amid weak steel demand and high inventories.

Why did Japan’s scrap exports surge y-o-y?

Downtrend in crude steel production drives scrap surplus: Japan’s crude steel production declined 4% y-o-y to a 57-year low of 81 mnt in CY’25 amid weaker steel demand. Similarly, both scrap consumption and generation fell to 29.7 mnt and 37.1 mnt, respectively.

Moreover, as generation fell at a relatively slower pace than consumption and scrap availability remained consistently higher than domestic usage, a surplus emerged.

Japan’s steel sector remained under pressure amid US import tariffs and rising Chinese exports, which weighed on external demand. Domestically, weak construction activity, driven by labour shortages and high raw material costs, along with softer manufacturing output, further dampened steel consumption.

In the automotive sector, production increased 2% y-o-y to 8.4 million units in 2025, while domestic sales rose 3% to 4.6 million units. However, exports–accounting for nearly half of total sales–declined 1% y-o-y to 4.2 million units, limiting overall demand support for the steel industry.

Freight advantages, steady supply attract Asian importers: Besides being preferred due to its consistent chemistry and higher yield, Japanese H2/shredded scrap benefits from freight advantages in Asian markets, supported by shorter sailing distances, flexible Handysize vessel shipments, and faster transit times compared with deep-sea suppliers such as the US and Europe, resulting in more competitive landed costs for regional buyers.

Higher European procurement costs due to the Red Sea crisis pushed importers such as Bangladesh and India to shift sourcing toward nearby East Asian scrap. Japanese exporters also offered regular bulk cargoes, helping mills secure steady feedstock amid tight regional supply.

Importer-wise dynamics

Vietnam: Vietnam remained the largest importer of Japanese scrap, accounting for 44% of Japan’s total exports. Vietnam’s crude steel production rose around 9.5% y-o-y to 24 mnt in 2025, with steel demand structurally supported by rapid urbanisation, propelling increased construction activity in townships and higher scrap consumption.

Bangladesh: Scrap exports to Bangladesh more than doubled, supported by active trade and steady cargo availability from Japanese suppliers.

South Korea: Japanese exports to South Korea also dropped 20% y-o-y, reflecting reduced demand. Crude steel production declined by around 4.2% y-o-y to 61 mnt in CY’25, weighing on scrap imports.

Indonesia: Japan’s ferrous scrap exports to Indonesia rose 144% y-o-y, accounting for more than 50% of the country’s total imports. In CY’25 Japan also overtook Hong Kong to jointly become the top supplier with Australia.

Taiwan: Japanese shipments to Taiwan declined by 43%, as buyers continued to favour competitively priced US cargoes. The drop in imports was driven by subdued steel demand, elevated scrap inventories at mills, and increasing competition from cheaper Chinese steel in the local market. Meanwhile, Taiwan’s crude steel production declined by 12% y-o-y to 17 mnt.

India: India’s imports from Japan surged threefold in CY’25, though the volume remained a minor share of its total 8 mnt. Shipments from the US and UK declined amid high prices and freight costs, keeping buyers more interested in Japanese supply.

Price trend

Japanese H2 prices, FOB Tokyo Bay, declined 13% y-o-y to a yearly average of $265/tonne (t) in CY’25 from $304/t in CY’24, as per BigMint’s assessments.

On a monthly average basis, through early 2025, FOB prices remained range-bound at $260-275/t amid sporadic buying interest amid uncertain finished steel demand and volatile freight. At the same time, Japan’s domestic scrap prices remained relatively stable, limiting aggressive export offers.

From mid-2025, prices began to firm up gradually. The recovery was driven by improving steel demand in Bangladesh and Vietnam, reduced scrap generation in Japan, and firmer domestic scrap prices following mill restocking. In addition, a weaker yen improved export competitiveness, encouraging higher FOB offers.

Outlook

Japan’s steel market outlook remains subdued yet supportive for scrap exports, with crude steel production expected at 80-85 mnt in CY’26 amid weak construction activity and moderate export performance. The domestic market continues to face soft demand, labour shortages, and pressure from cheaper imports, particularly from China, limiting steel consumption and keeping scrap generation broadly stable.

Scrap-EAF producers in Japan are expected to maintain a “business-as-usual” approach, with limited expansion or diversification, as they remain heavily dependent on the construction sector, where demand growth is weak. This lack of structural change, combined with stable scrap availability, will continue to support export-oriented scrap flows.

On the demand side, scrap consumption is likely to improve gradually, supported by the government’s GX (Green Transformation) initiatives, although adoption remains slow due to uncertainty around green steel demand and renewable energy costs. Future EAF capacity additions post-FY’28 are expected to tighten scrap availability structurally.

The availability of high-grade scrap (H2, shredded) is expected to remain tight, supporting price levels, while overall supply remains sufficient to sustain export volumes.

Demand from Southeast Asia will continue to anchor exports, driven by infrastructure growth and increasing EAF adoption, particularly in Indonesia and Vietnam. Bangladesh and India will remain consistent buyers due to freight advantages and reliable supply, while Taiwan and South Korea are likely to stay cautious amid weak steel demand and high inventories.

Overall, Japan is expected to remain a stable scrap exporter, with steady supply and firm regional demand shaping market dynamics in the near term.

Leave a Reply