- Weak domestic demand continues to constrain steel market recovery

- Geopolitical risks and export barriers weigh on near-term outlook

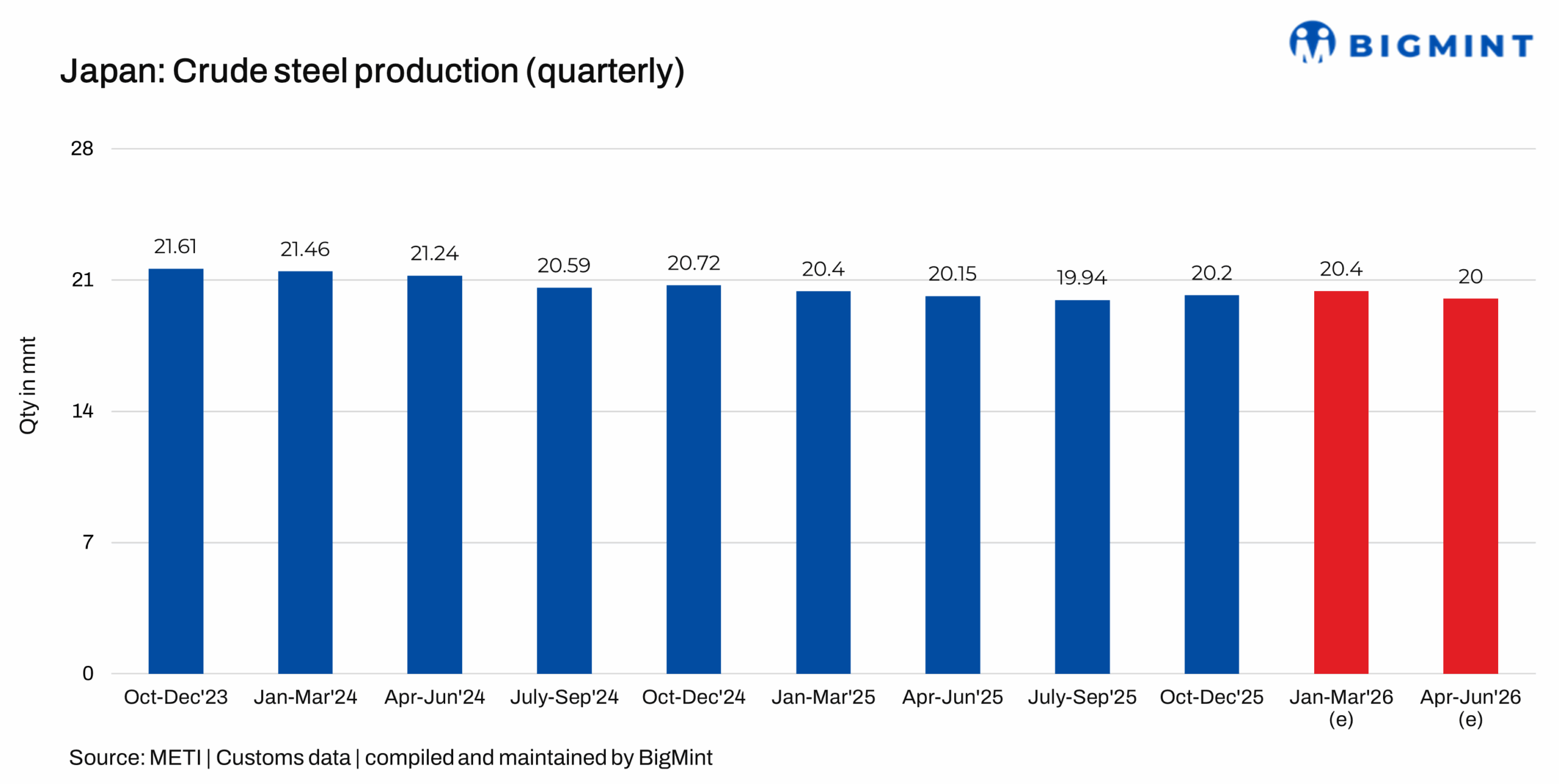

Japan Metal Daily: Japan’s Ministry of Economy, Trade and Industry (METI) forecasts crude steel production to remain subdued at around 20 million tonnes (mnt) in April-June 2026, down 0.7% y-o-y, reflecting persistently weak domestic and overseas demand. The outlook is further clouded by ongoing uncertainty surrounding the Middle East situation, pointing to a soft start for steel demand in FY2026 (April 2026-March 2027).

The projected decline follows a temporary improvement in January-March 2026 output, estimated at 20.41 mnt, around 400,000 tonnes (t), above the initial forecast, marking the first y-o-y increase in nine quarters. This higher base is expected to lead to a quarter-on-quarter reversal, with output likely to contract again in April-June 2026.

METI noted that the current forecast does not incorporate potential disruptions stemming from the Middle East, indicating that downside risks remain. Metals Division Director Manabu Nabeshima stated that authorities will continue to closely monitor developments and respond flexibly to shifts in demand conditions.

Meanwhile, total steel demand for April-June 2026 is projected at 17.98 mnt, down by 1.5% y-o-y and 1.3% lower than the previous quarter, signalling limited momentum across key steel consuming sectors. Demand for ordinary steel is expected to remain at 14.32 mnt, marking a decline of 1.0% y-o-y.

Domestic demand is forecast at around 9.22 mnt, falling by 1.6% y-o-y, as both construction and manufacturing activity remain under pressure. Within manufacturing, industrial machinery is the only segment expected to record growth, while major steel-consuming sectors such as automobiles and shipbuilding are likely to remain sluggish, underscoring the uneven demand recovery.

Export demand is expected to edge up marginally to 5.1 mnt, rising by 0.2% y-o-y, though overall volumes will remain constrained by weak demand in ASEAN markets and the expanding scope of trade measures across multiple regions.

Beyond near-term demand conditions, METI highlighted broader external risks, including the deterioration in China’s steel supply-demand balance and evolving US tariff policies, both of which could further weigh on regional trade flows and pricing dynamics.

Note: This article has been written in accordance with a content exchange agreement between Japan Metal Daily and BigMint.

Leave a Reply