- Dec’25 prices rise in the US on tight supply, Turkish buying appetite

- Japanese scrap prices may soften on slow Korean, Vietnamese demand

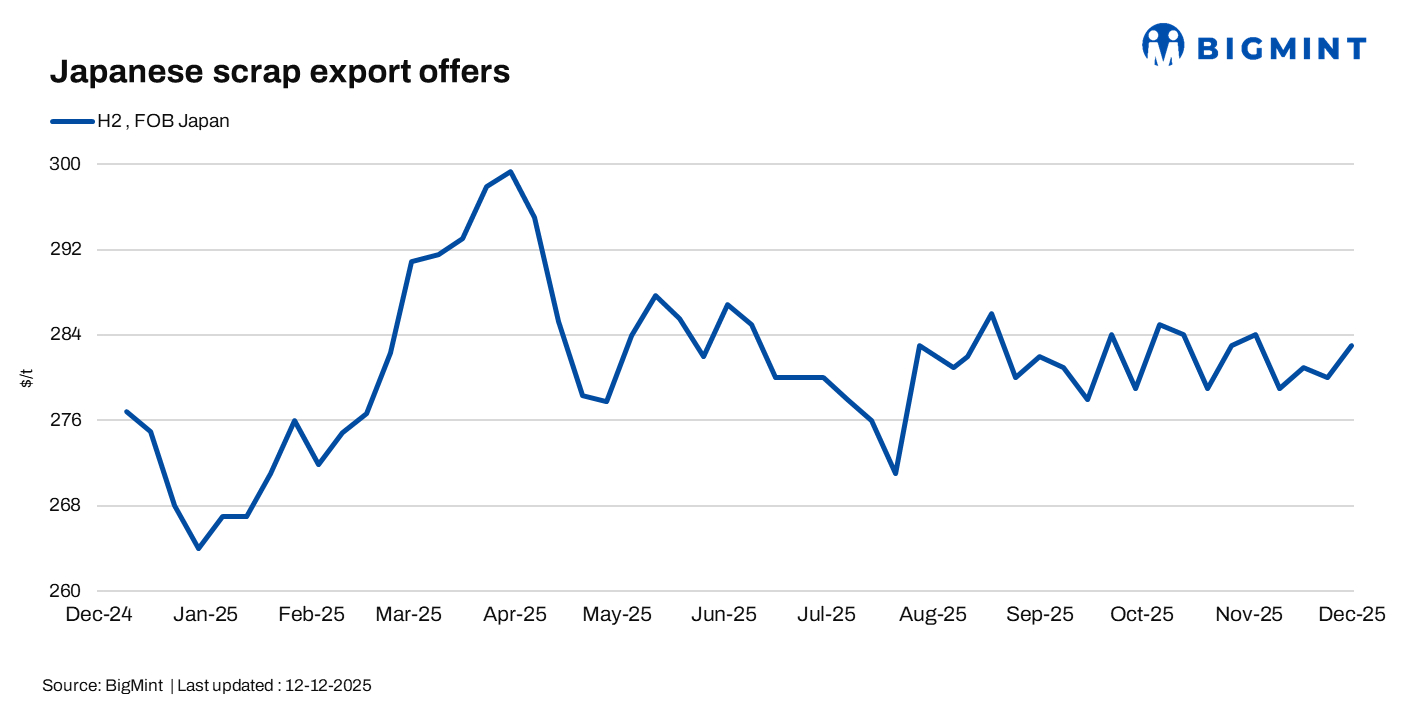

Japan’s H2 export prices firmed up following the Kanto tender, while US export prices remained supported due to tight domestic supply and steady Turkish demand.

Japan’s ferrous scrap export prices up

BigMint assessed Japan’s H2 scrap at JPY 44,000/t ($283/t) FOB Tokyo Bay, up JPY 300/t ($2/t, 1%) from last week.

H2 offers to Vietnam were reported at $325-328/t CFR, stable w-o-w, while some traders paused after the Kanto tender. US-origin HMS 80:20 deep-sea offers and bids remained stable at $350/t and $340-342/t CFR.

The winning bid in December’s Kanto tender was JPY 45,688/t ($292/t) for a 15,000-t cargo bound for Vietnam, up JPY 728/t and about $1/t from last month, though it may not reflect regular spot H2 market levels.

A Japan-based trader noted that sellers may attempt to lift offer levels after the Kanto tender results, while “Vietnam mills are unlikely to adjust their bids.”

US export scrap prices climb on strong Turkish buying

US export scrap prices were largely stable and edged up by $1/t w-o-w, reaching their highest levels since April 2025. Tight domestic HMS supply and firm Turkish demand continued to underpin the market’s upward momentum.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $339/t, up by ($1/t) w-o-w.

- Shredded – $359/t, up by ($1/t) w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – up by ($1/t) w-o-w at $370/t.

- Vietnam – down by ($3/t) w-o-w at $342/t.

- Bangladesh – up by 1% ($2/t) w-o-w at $356/t.

According to a trader, December’s positive fundamentals were tempered by smaller buying programmes as several mills with sufficient scrap inventories skipped procurement to limit year-end spending. Dealers, however, expect pent-up demand to emerge in January and reinforce upward price momentum as mills return to the market.

Outlook

Japan may see sellers lift offers gradually after the tender, while Vietnamese mills are likely to keep bids stable. In the US, continued Turkish demand and tight domestic supply are expected to support prices, with January mill procurement expected to provide further support.

Leave a Reply