- Weak demand, port congestion lower Japanese H2 prices

- South Korea’s scrap imports rise as inventories shrink

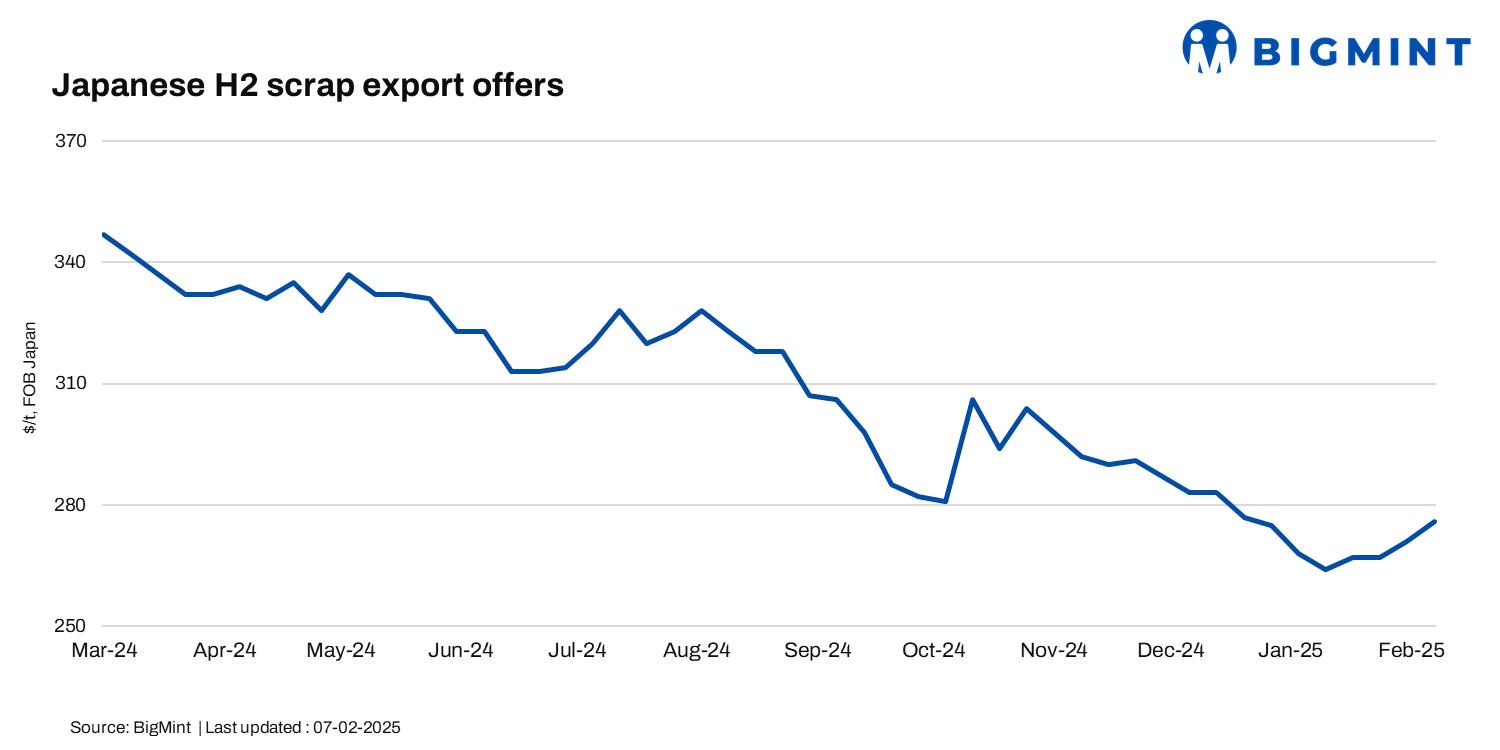

The Japanese H2 scrap export market saw a slight drop in the week, with limited activity as buyers gradually returned from holidays. Seaborne demand, especially from Vietnam, remained thin, as buyers awaited price signals from China’s post-holiday market trends.

Additionally, port congestion in Japan continued to delay shipments, pushing some February orders into March. Meanwhile, BigMint’s latest assessment showed a slight dip of JPY 400/t ($3/t), bringing Japanese H2 scrap export prices to JPY 41,600/t ($274/t) FOB Tokyo Bay, down from JPY 42,000/t ($277/t) last week.

According to the Japan Iron and Steel Association, the average H2 scrap price across Japan’s three key regions in the first week of February stood at JPY 37,300/t ($246/t), down JPY 300/t ($2/t) from the prior week. Regionally, prices declined by JPY 500/t ($3/t) to JPY 35,100/t ($231/t) in the central region, by JPY 200 ($1/t) to JPY 36,800 ($243/t) in Kansai, while in Kanto they remained at JPY 42,000/t ($277/t).

Updates of other markets

Vietnam: Vietnam’s imported scrap market remained cautious after the Tet holidays, with buyers closely monitoring China’s post-holiday movements before setting bid levels. While some mills had sufficient inventories due to pre-holiday restocking, others expected demand to recover as January shipments were lower and procurement had been minimal.

Japanese H2 scrap offers were heard at $315-$320/t CFR Vietnam, with moderate demand in the market. However, port congestion in Japan continued to delay shipments, pushing some February cargoes into March.

No deep-sea scrap offers toward Vietnam were reported, reflecting the generally subdued sentiment in the broader Asian scrap market.

South Korea: South Korea’s imported scrap market saw a surge in arrivals, reaching 109,750 t this week, a sharp rebound from January’s 7,000 t. Around 72% of imports were driven by plate and special steelmakers, while shaped steel manufacturers remained subdued due to weak construction demand.

Major buyers included Hyundai Steel, POSCO, and SeAH Besteel. Meanwhile, domestic scrap inventories at major mills fell 11% w-o-w, with sharper declines in the central region, raising concerns over supply shortages.

Hyundai Steel and others have responded by increasing scrap purchase prices by KRW 10,000/t ($7/t) from 4 February, with POSCO implementing hikes at Gwangyang and Pohang. If inventory shortages persist, further price increases are expected.

Taiwan: Taiwan’s imported and domestic scrap market saw an upswing as global scrap prices strengthened. Feng Hsin Steel, the island’s largest rebar producer, raised both its rebar list price and local scrap procurement price by TWD 300/t for 4-7 February. Imported scrap prices also climbed, with US HMS 80:20 rising by $10/t to $305/t CFR and Japanese H2 by $5/t to the same level.

Stronger Chinese steel prices and lower-than-expected inventory accumulation post-holiday fuelled positive sentiments. The market outlook remains firm as mills adjust pricing to cover higher production costs.

Leave a Reply