- Lower freights boost competitiveness of US export offers

- Japanese sellers continue to face weak demand in Vietnam

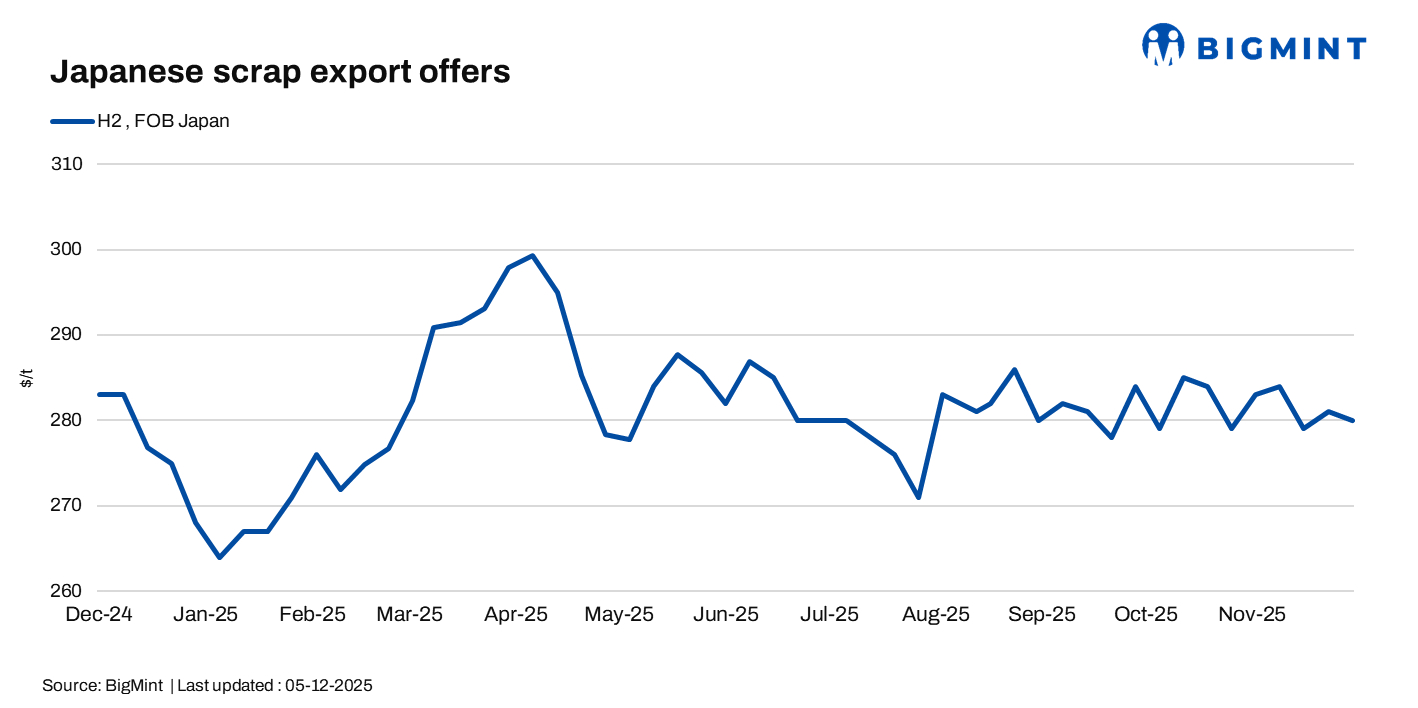

Japan’s H2 scrap prices eased w-o-w on 5 December 2025 due to a stronger JPY, while US scrap export offers rose on strong Turkish buying and rebar demand.

Japan’s ferrous scrap export prices soften

BigMint assessed Japan’s H2 scrap at JPY 43,700/t ($283/t) FOB Tokyo Bay, down JPY 250/t ($2/t, 1%) from last week, as the JPY strengthened against the US dollar.

H2 scrap offers in Vietnam held at $325-330/t CFR, with tradable levels at $322-323/t, while bids were near $320/t. US-origin HMS 80:20 softened to $350-355/t, while indicative bids stayed at $340-342/t CFR.

Market participants attributed weak demand in Vietnam to weather disruptions and a sluggish downstream steel market. A mill-side participant noted that although Typhoon Koto did not make landfall in Vietnam, overall market conditions remain soft.

US export scrap prices climb on strong Turkish buying

US export scrap prices increased by $6/t (2%) w-o-w to their highest level since March 2025, extending weeks of upward momentum.

Falling freight rates to $42/t (from $47/t) improved exporter margins, while higher CFR prices pushed US dock prices upward amid tight supply and winter-affected flows.

Narrowing billet-scrap spreads also signalled strengthening scrap fundamentals, as Turkish mills continued with steady restocking.

FOB assessments (US East Coast, bulk)

HMS 80:20 – $338/t, up by 2% ($6/t) w-o-w.

Shredded – $358/t, up by 2% ($6/t) w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

Turkiye – up by 2% ($6/t) w-o-w at $369/t.

Vietnam –down by 0.3% ($1/t) w-o-w at $345/t.

Bangladesh –up by 1% ($2/t) w-o-w at $355/t.

Turkiye’s strong long steel demand sustained deep-sea scrap purchases despite the lira hitting a record of above 42 per dollar. Weak US labour data pushed the Dollar Index below 99, boosting the competitiveness of US export cargoes. Turkish mills have already secured five deep-sea cargoes in December, with most of them being of US-origin.

Outlook

Japan’s scrap market may remain subdued amid a stronger yen and the pending Kanto-Tetsugen tender, while Vietnamese demand could stay weak due to adverse weather and slow downstream activity. US export offers are likely to remain firm, supported by strong Turkish buying and competitive freights.

Leave a Reply