- Baosteel raises HRC prices for Jan’26, Formosa lowers offers

- Winter weakness, construction slowdown to weigh on prices

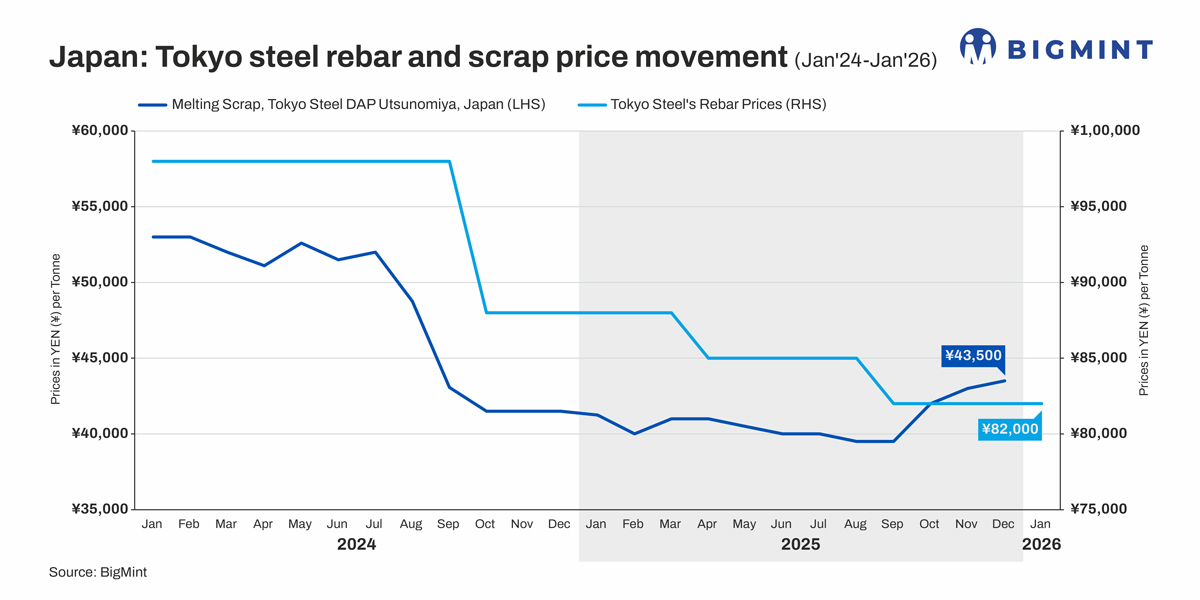

Tokyo Steel, Japan’s leading electric arc furnace (EAF) steel producer, has kept its HRC (1.7–22 mm) prices unchanged m-o-m for January 2026 sales. Rebar and H-beam prices have also been maintained at stable levels m-o-m.

The latest prices are as follows:

- HRC (1.7–22 mm): JPY 86,000/t ($555/t)

- Rebars (D13–25): JPY 82,000/t ($529/t)

- H-beams (100–300 mm): JPY 103,000/t ($664/t)

Factors influencing Tokyo Steel’s pricing:

1. Domestic demand remains subdued: Domestic steel demand in Japan remains sluggish, as winter seasonality and uneven construction activity across regions continue to weigh on shipments, keeping buying interest subdued despite low inventory levels. However, market sentiment remains cautiously optimistic, underpinned by expectations that demand conditions will gradually improve as construction activity picks up.

2. Leading global mills’ price trends: Baosteel, the world’s leading steel manufacturer, has raised its HRC prices by RMB 100/t ($14/t) m-o-m for January 2026 sales after keeping pices stable for three consecutive months. This rise in prices is attributed to a rise in SHFE HRC futures, which increased by RMB 36/t ($6/t) m-o-m to RMB 3,277/t ($464/t). In addition, prices of hot-dip galvanised (HDG) also increased by RMB 100/t ($14/t) m-o-m.

Meanwhile, Vietnamese steelmaker Formosa Ha Tinh (FHS) has reduced its hot-rolled coil (HRC) prices by around $14/t for January 2026 sales. After the adjustment, FHS’s HRC (SAE1006, skin-passed) is now priced at approximately $497/t CIF Ho Chi Minh City (HCMC), reflecting continued weakness in domestic steel demand following the severe damage caused by Typhoon Kalmaegi.

3. Kanto scrap export offers rise: Japan’s December 2025 Kanto scrap export tender recorded its fifth consecutive m-o-m increase of JPY 728/t ($5/t), with a 15,000-t H2 lot reportedly awarded via a trading firm to a Vietnam-based mill at JPY 45,688/t ($294/t) FAS Japan. However, in dollar terms, the increase was limited to just $1/t, as the weaker JPY, sliding from 153.8/$ on 11 November to 156.6/$ on 10 December, offset the yen-denominated gains and lifted export offer levels.

Outlook

Tokyo Steel’s prices are expected to remain largely stable in the near term, as winter seasonality and uneven construction activity continue to weigh on shipments. Market sentiment is expected to gradually improve toward Q1 2026 as construction activity recovers; however, any price upside is likely to remain capped until clearer signs of a sustained domestic demand recovery emerge.

Leave a Reply