- Demand recovery expected amid rising inquiries, low inventories

- Baosteel keeps HRC prices firm for Dec’25, FHS cuts Jan’26 tags

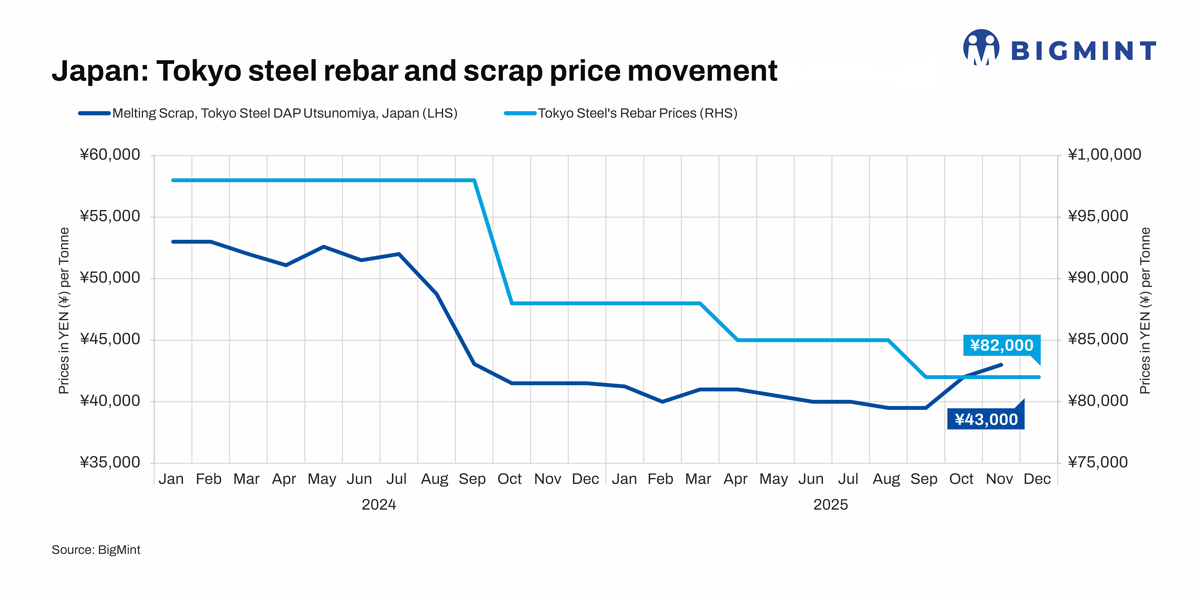

Tokyo Steel, Japan’s leading electric arc furnace (EAF) steel manufacturer, has kept prices of hot-rolled coils (HRCs) (1.7-22 mm) stable for December 2025 shipments compared to the previous month. Additionally, the company has rolled over its prices of rebars. However, H-beam prices increased by JPY 3,000/t ($19/t) for the same period.

Revised prices are as follows:

- HRCs (1.7-22 mm): JPY 86,000/t ($556/t)

- Rebars (D13~25): JPY 82,000/t ($530/t)

- H-beams (100-300 mm): JPY 103,000/t ($666/t)

Factors influencing Tokyo Steel’s pricing

1. Domestic market remains subdued: Domestic demand in Japan remains uneven, with rising inquiries for civil engineering materials but sluggish cargo movement. Redevelopment and large facility projects are gradually boosting quotations, and low inventories suggest prices have bottomed out, supporting expectations of a near-term market recovery.

2. Key global mills’ pricing trends: Baosteel, the world’s leading steel manufacturer, has kept HRC prices stable for December 2025 sales. This marks the third consecutive month of unchanged pricing, driven by subdued domestic demand. Hot-dip galvanised prices also remained flat m-o-m.

Vietnamese steel giant Formosa Ha Tinh (FHS) has reduced its hot-rolled coil (HRC) prices by approximately $16/t for January 2026 sales against November 2025 sales. Following this adjustment, FHS’s HRC prices (SAE1006, skin-passed) stood at around $511/t CIF Ho Chi Minh City (HCMC).

3. Kanto scrap export offers rise: Japan’s November 2025 Kanto scrap export tender witnessed a moderate m-o-m uptick of JPY 644/t ($4/t), with a 20,000-t H2 lot reportedly awarded via a Japanese trading firm to a Vietnam-based mill at JPY 44,960/t ($291/t) FAS Japan. As per market insiders, in dollar terms, the increase was limited to $1/t, supported mainly by a weaker JPY (from JPY 151/$1/t on 9 October to 154.5/$ on 11 November), which increased export offers.

Outlook

In the short term, global steel markets remain subdued due to high US tariffs, weak Chinese demand, and rising protectionism. In Japan, low inventories and improving project inquiries hint at a modest price recovery, though elevated production costs may limit momentum.

Leave a Reply