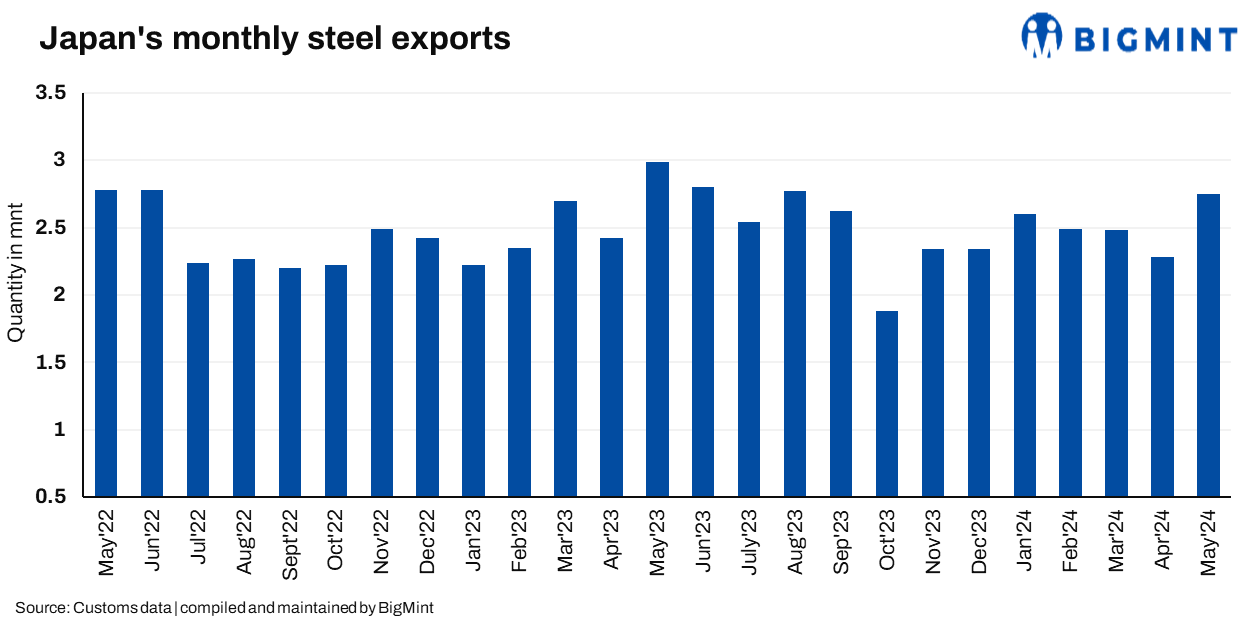

Steel exports dropped for the fourth month in a row in May, as per data released by Ministry of Finance on 19 June. Exports fell 8.3% y-o-y to 2.749 million tonnes (mnt). Steel exporters are navigating a complex and demanding negotiation environment.

Overseas markets are weak, with HRC prices in Asia stuck around $500/t. Domestic demand is also subdued due to volatile auto industry. However, the weak yen makes exporting more attractive, pushing steel producers to prioritise export contracts. May’s steel exports represent the highest monthly export figure this year.

ASEAN steel imports dipped for the first time in two months, dropping 10% to 817,000 tonnes (t). However, it remained above 800,000 t for the second month in a row. South Korea’s imports continued a downtrend, falling 18.7% to 405,000 t, marking the eighth consecutive month of decline amid trade concerns. However, China’s imports, which were low in the prior year, increased by 1.2% to 269,000 t, marking their first increase in two months.

Sales dropped significantly outside of Asia- the US saw 9.7% decline to 92,000 t, while the Middle East experienced a steeper fall of 26.4% to 83,000 t. Furthermore, the EU market was hit the hardest, with sales falling by 72.4% to 77,000 t. This decrease in the EU is attributed to difficulty navigating the Suez Canal due to heightened Houthis activity, the timing of quota renewals that avoid safeguard taxes, and a significant drop in shipment volume compared to the previous month.

Steel imports rose in May by 6.6% y-o-y, reaching 625,000 t. This marks the second consecutive month of increase. While, South Korea led the surge with imports rising 19.6% to 322,000 t, followed by ASEAN at 33% to 32,000 t. China also saw an increase of 2.7%, bringing its imports to 110,000 t.

Note: This article has been written in accordance with an article exchange agreement between Japan Metal daily and BigMint.