- Total steel demand to decline 4% y-o-y in Apr-Jun’25

- Export outlook bleak amid weak demand, trade tensions

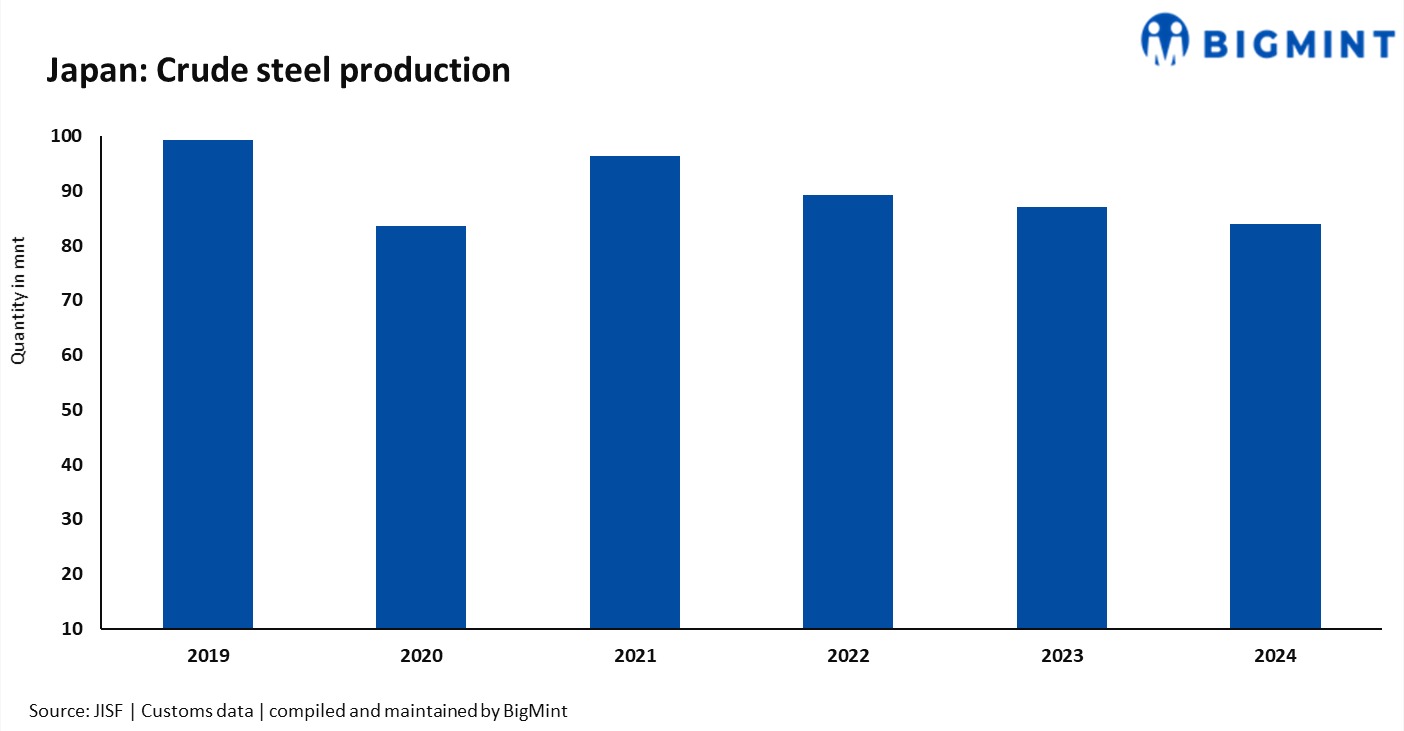

Japan Metal Daily: Japan’s Ministry of Economy, Trade, and Industry (METI) has released its steel demand forecast for the April-June period, projecting a crude steel production equivalent of 20.2 million tonnes (mnt). This figure indicates a continued downtrend, approximately 2% lower than the previous quarter’s forecast and about 5% lower y-o-y. Notably, this marks the sixth consecutive quarter with a y-o-y decline, signalling a clear and persistent slowdown in steel product demand.

Additionally, the overall demand for steel products is projected to be 18.04 mnt in the April-June period, comprising 14.38 mnt of ordinary steel and 3.66 mnt of special steel. This represents a 4% y-o-y decrease for total steel demand and a 3% y-o-y drop for ordinary steel demand.

Domestic consumption to decline across sectors

Within Japan’s domestic market, several key sectors are experiencing reduced steel consumption. Construction and civil engineering are projected to see a 2.4% decrease, while the automotive sector is expected to decline by 0.1%. The industrial machinery sector faces a more significant drop of 10.7%. Despite automakers’ production systems recovering, automobile sales are expected to remain at the same level as the previous year’s significantly reduced figures.

Export market to face significant hurdles

The export market also faces significant challenges. Demand from key markets such as China and ASEAN for automobiles and other steel-intensive products remains sluggish. Moreover, trade measures targeting Japanese steel are proliferating, exacerbating the already difficult export environment. These factors collectively indicate that the export outlook is likely to worsen.

Outlook

The steel industry faces continued downward pressure, with demand projected to remain low. At a press conference, Manabu Nabeshima, director of METI’s Metals Division, acknowledged the downtrend in demand and emphasised the need for vigilance against future risks, particularly those arising from US tariff measures, which were not factored into the current forecast.

The future outlook hinges on global economic stability, particularly in China and ASEAN, and the impact of increasing trade barriers. The industry must navigate sluggish domestic construction and automotive sectors while adapting to a challenging export environment.

Note: This article has been written in accordance with a content exchange agreement between Japan Metal Daily and BigMint.

Leave a Reply