- Tokyo Steel trims prices by $3/t post-Kanto result at 2 sites

- EAF output cuts, monsoon weigh on consumption outlook

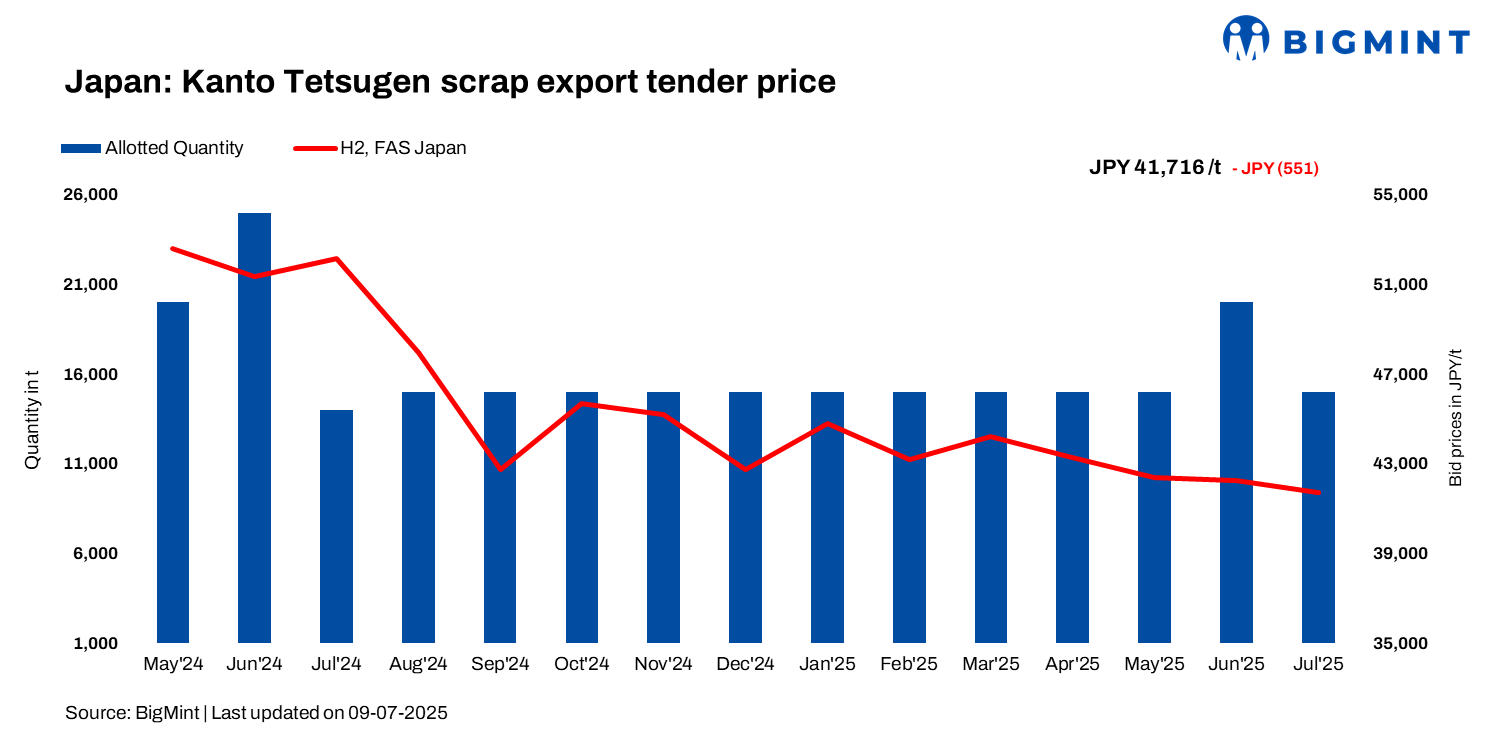

Japan’s July 2025 Kanto scrap export tender witnessed an m-o-m drop of JPY 551/t ($4/t), with a 15,000-t H2 lot awarded to a Chattogram-based mill via a trader at JPY 41,716/t ($284/t) compared to JPY 42,267/t ($291/t) FAS Japan– marking the fourth straight monthly drop.

Similarly, the dollar-denominated price also slipped by $7/t m-o-m from $291/t in June. A weaker JPY (147.1/$ on 9 July versus 145.08/$ on 11 June) softened the fall in JPY terms.

As per market feedback, buying interest from key overseas regions remained weak, keeping bids under pressure. A weak export market also pressured domestic prices. This round of bidding saw participation from all 15 trading companies, with total bids amounting to 116,500 t–down nearly 47,000 t from the previous month, though still above 100,000 t for the seventh month in a row.

Chairman Minami remarked that while expectations were slightly higher, the result was reasonable under the current market conditions.

Despite weak buying interest from key importers like Vietnam, the bid exceeded domestic mill and bay prices (JPY 40,000-41,500/t), and was viewed as solid.

The FOB level for this shipment is estimated at $293/t, translating to approximately $345-347/t CFR Chattogram and $352-354/t CFR Kandla. Freight differentials between Bangladesh and India could be at least $7-10/t. The shipping deadline is set for 31 August, aligning with traders’ schedules before the summer holiday period in mid-August.

Japan scrap market update

Chubu: Scrap prices fell by another JPY 500/t ($3/t), marking the second cut this month as EAF mills scaled back output for July power-saving curbs. Tokyo Steel’s Tahara plant initiated the drop, followed by Totetsu and Daido Steel. Sentiment remained cautious, with room for further downside.

Western Japan: Totetsu held prices steady, but an Osaka-based mill’s JPY 500/t cut prompted similar adjustments ahead of summer maintenance.

Kanto: Prices stayed stable for two months, with H2 scrap trading at JPY 40,000-41,000/t ($273-280/t).

Tokyo Steel: Following the Kanto tender, Tokyo Steel cut purchase prices by JPY 500/t ($3/t) at Utsunomiya and Tokyo Bay satellite yards, effective 10 July. Other locations remain unchanged.

- Utsunomiya: JPY 40,000/t ($273/t)

- Tokyo Bay Satellite: JPY 40,500/t ($276/t)

Japanese H2 export prices dropped slightly amid limited buying interest, with Asian mills opting for conservative procurement due to the monsoon steel demand lull and summer maintenance.

BigMint assessed the weekly H2 scrap export price at JPY 40,400/t ($276/t) down by JPY 100/t ($0.7/t) w-o-w FOB Tokyo Bay.

Importer’s market updates

Vietnam: Vietnam’s imported scrap market remained sluggish, with buyers maintaining a cautious stance amid currency fluctuations and subdued steel demand. Japanese H2 offers ranged between $315-320/t CFR, but bids stayed lower at $310-315/t, signalling weak buying appetite. Traders pointed to the ongoing rainy season and a weakening VND as key factors dampening sentiment.

Bulk HMS 80:20 offers from the US held steady at $340-342/t CFR, while bids hovered at $335/t CFR. Australian-origin offers were also heard at $335/t CFR and above, though no firm bids emerged. Buyers reportedly preferred smaller lots to hedge against market volatility.

Bangladesh: The imported scrap market remained sluggish, as mills showed limited interest in fresh bulk bookings, aside from routine Kanto tender purchases aimed at securing lower prices. The market continued to be weighed down by monsoon disruptions and weak construction demand.

Bulk HMS 80:20 offers stood at $350-355/t CFR, while Japanese H2 was quoted at $345-350/t. Inquiries from Singapore were higher at $380-385/t. However, buyer interest remained muted, with bids hovering closer to $345/t for HMS and $375/t for PNS.

Outlook

Japan’s scrap market started July on a weaker note amid reduced EAF operations, low steel demand, and limited export interest. Extreme heat disrupted urban scrap collection, causing localised tightness that may slow further price drops. With furnace maintenance ongoing and the next Kanto auction on 8 August, the market remains in wait-and-watch mode.

Leave a Reply