- 20,000 t of H2 reportedly sold to Vietnamese mill

- JPY depreciation supports Japan’s H2 export offers

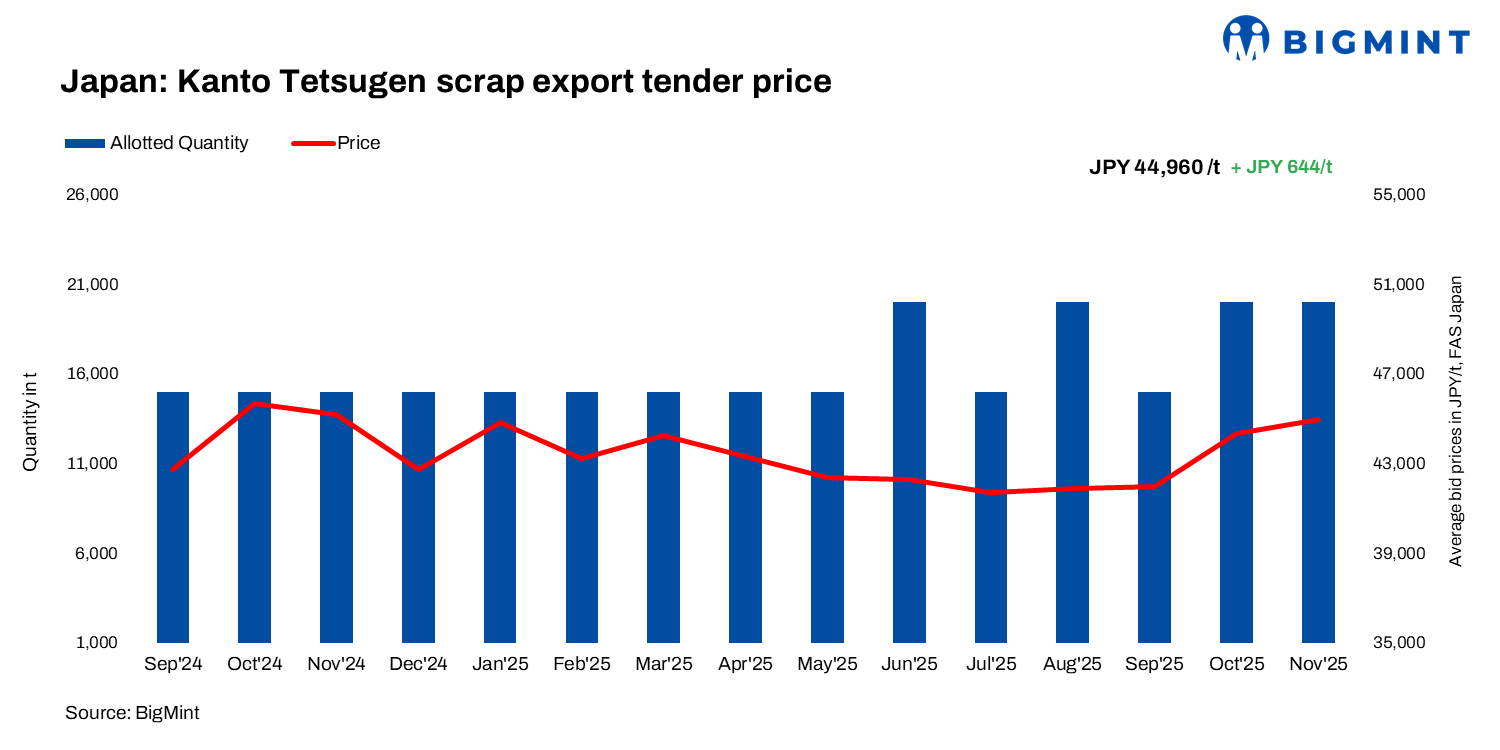

Japan’s November 2025 Kanto scrap export tender witnessed a moderate m-o-m uptick of JPY 644/tonne (t) ($4/t), with a 20,000-t H2 lot reportedly awarded via a Japanese trading firm to a Vietnam-based mill at JPY 44,960/t ($291/t) FAS Japan.

For comparison, this is a slight increase from the October tender’s JPY 44,316/t ($290/t). This marks the fourth consecutive monthly price rise and the highest since January’s JPY 44,810/t.

As per market insiders, in dollar terms, the increase was limited to $1/t, supported mainly by a weaker JPY (from JPY 151/$1/t on 9 October to 154.5/$ on 11 November), which increased export offers.

Due to weak domestic demand, the shipment volume was capped at 20,000 tonnes per vessel for the second straight month.

All 15 trading companies participated, submitting a total of 15 bids with no withdrawals. The cumulative bid volume reached 121,100 tonnes–down by 25,000 t from the previous month — but still above the 100,000 t mark for the 11th consecutive month.

Tokyo Steel raises scrap purchase prices post-Kanto tender

Tokyo Steel announced its second scrap price hike for November, effective 12 November 2025, increasing rates by JPY 500/t ($3/t) across all plants. Post-revision, H2 scrap stood at JPY 44,000/t ($285/t) at Tahara, Okayama, Kyushu, and Tokyo Bay; JPY 43,500/t ($282/t) at Nagoya and Kansai; JPY 43,000/t ($279/t) at Utsunomiya; and JPY 39,000/t ($253/t) at Takamatsu.

Japan’s domestic, export scrap market

Last week, H2 scrap deals were estimated at JPY 43,400-44,000/t FOB ($282-286/t) amid tight supply and a weaker yen.

Current Kanto region domestic scrap prices were at JPY 42,000-43,000/t ($272-279/t), and it is anticipated that domestic prices may rise following the higher bids.

As per market insiders, Vietnamese mills bid $320-324/t for H2 scrap, while Japanese suppliers held firm with offers around $330-335/t, leading to a modest gap in price expectations.

As per market insiders, Vietnamese mills bid $320-324/t for H2 scrap, while Japanese suppliers held firm with offers around $330-335/t, leading to a modest gap in price expectations.

Outlook

The weaker JPY continues to support higher export offers, with buyers from Bangladesh and South Korea closing deals at these levels. Domestic demand remains subdued amid fiscal uncertainty under Takaichi’s leadership. Activity is expected to stay selective, guided by currency trends and tight supply, the next shipment of 20,000 t is scheduled for loading between 13-29 December, with the next bid set for 10 December.

Leave a Reply