- Kanto tender sees 15,000 t of H2 sold to Bangladesh

- Japanese market to remain range-bound in near term

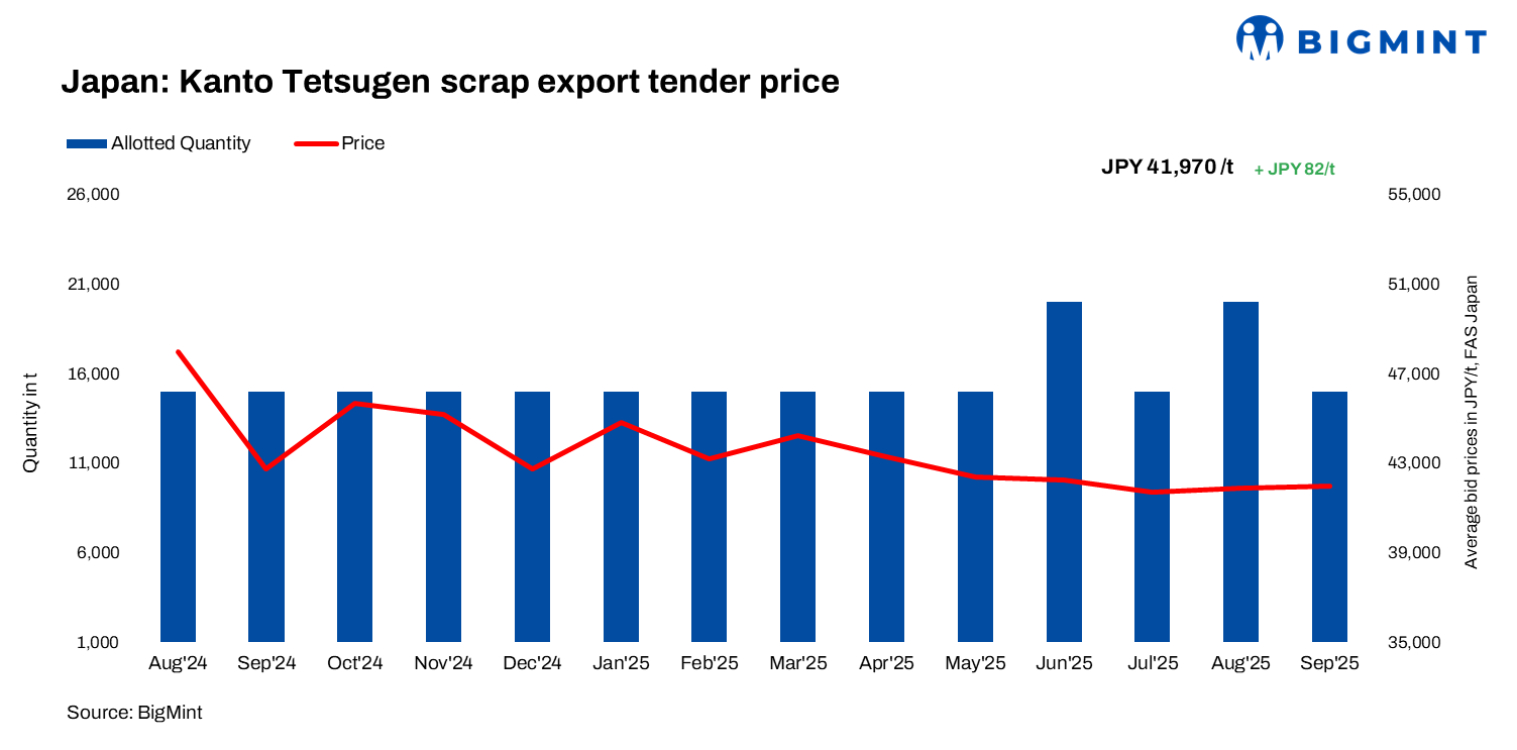

Japan’s September 2025 Kanto scrap export tender witnessed an m-o-m uptick of JPY 82/tonne (t) ($1/t), with a 15,000-t H2 lot reportedly awarded via a Japanese trading firm to a Chattogram-based mill at JPY 41,970/t ($285/t) FAS Japan. In comparison, the Kanto tender was concluded at JPY 41,888/t ($285/t) in August.

As per sources, a total of 15 bids were submitted by 14 of the 15 trading companies. No trading companies withdrew, but one company submitted a late bid. The total volume of the 15 bids was 145,900 t, an increase of 4,800 t from the previous month. This was the ninth consecutive month of over 100,000 t.

According to a supplier, “The aim is to ship the cargo by 31st October. The price equates to approximately $295/t FOB Japan, with an estimated freight of $50-55/t, bringing the CFR Chattogram cost to around $345-350/t for the buyer.”

The JPY-USD exchange rate remained largely stable (147.4/$ on 10 September vs. 147.6/$ on 9 August), which led to the dollar value rising by less than $0.3-0.4/t.

Notably, the latest Kanto tender witnessed the participation of a key Chattogram-based mill, which returned to the market after a month.

Japan’s scrap export market

Last Friday, BigMint’s weekly assessment placed H2 at JPY 41,500/t ($280/t) FOB Tokyo Bay, down by JPY 500/t ($3/t) w-o-w.

A Japanese trader noted that while prices dropped slightly, several Kansai-region mills were still under maintenance, and local demand showed little recovery.

As of 10 September, H2 scrap prices from electric furnace mills in the Kanto region were quoted at 39,000-40,500 JPY/t, while Gulf Coast H2 was at 39,500-40,500 JPY/t. The latest winning bid exceeded these spot levels.

Shipping of the 15,000 t under the July contract is expected to conclude by 18 September, while the schedule for the 20,000 t under the August contract remains undecided.

Updates on importing markets

Bangladesh: Bangladesh’s imported Japanese H2 prices rose $5/t w-o-w to $345-348/t CFR after the September Kanto tender. Liquidity challenges persisted as letter of credit (LC) openings remained slow, with offers at $345-350/t against bids of around $340/t.

Mills, however, have shown renewed activity, securing bulk cargoes from the US and Japan.

Vietnam: Imported ferrous scrap prices in Vietnam slipped $2-3/t w-o-w, as post-holiday trading remained sluggish amid regional softness. Demand for Japanese H2 eased late last week, with buyers shifting towards higher-grade scrap. Japanese H2 scrap was at $322/t CFR, down by $2/t w-o-w.

Across Asia, bearish billet markets weighed on sentiment, as Chinese mills faced high inventories and weak margins. Uncertainty over US tariffs further curbed Vietnamese deep-sea inquiries.

Taiwan: Imported scrap prices slipped, with US HMS 80:20 at $305/t CFR Taiwan and Japanese H2 at $310/t, both down $3/t w-o-w. Weak mainland China rebar demand and weather disruptions further pressured Taiwan’s market.

Taiwan’s Feng Hsin Steel reduced its rebar and local scrap purchase prices for 8-12 September amid sluggish demand and falling global scrap. The mill’s revised offers for 13-mm rebar stood at TWD 16,700/t ($550/t) exw, down TWD 300/t w-o-w, while HMS 1&2 80:20 was at TWD 7,800/t after successive cuts.

Outlook

Japan’s scrap export market is likely to stay range-bound in the near term, with H2 supported only marginally by Kanto tender trades. Bangladesh may show some buying interest, though LC constraints could restrict volumes. Taiwan’s demand outlook remains weak, weighed down by sluggish steel consumption and softer billet and rebar prices. The next Kanto tender, slated for 9 October, will be a key indicator for market direction. Without stronger Chinese demand or firmer US-origin offers, Asian scrap prices are expected to hover within a narrow band through September.