- Vietnam remain the active buyer for second consecutive month

- Tokyo Steel raises scrap purchase prices by $6/t following strong Kanto tender results

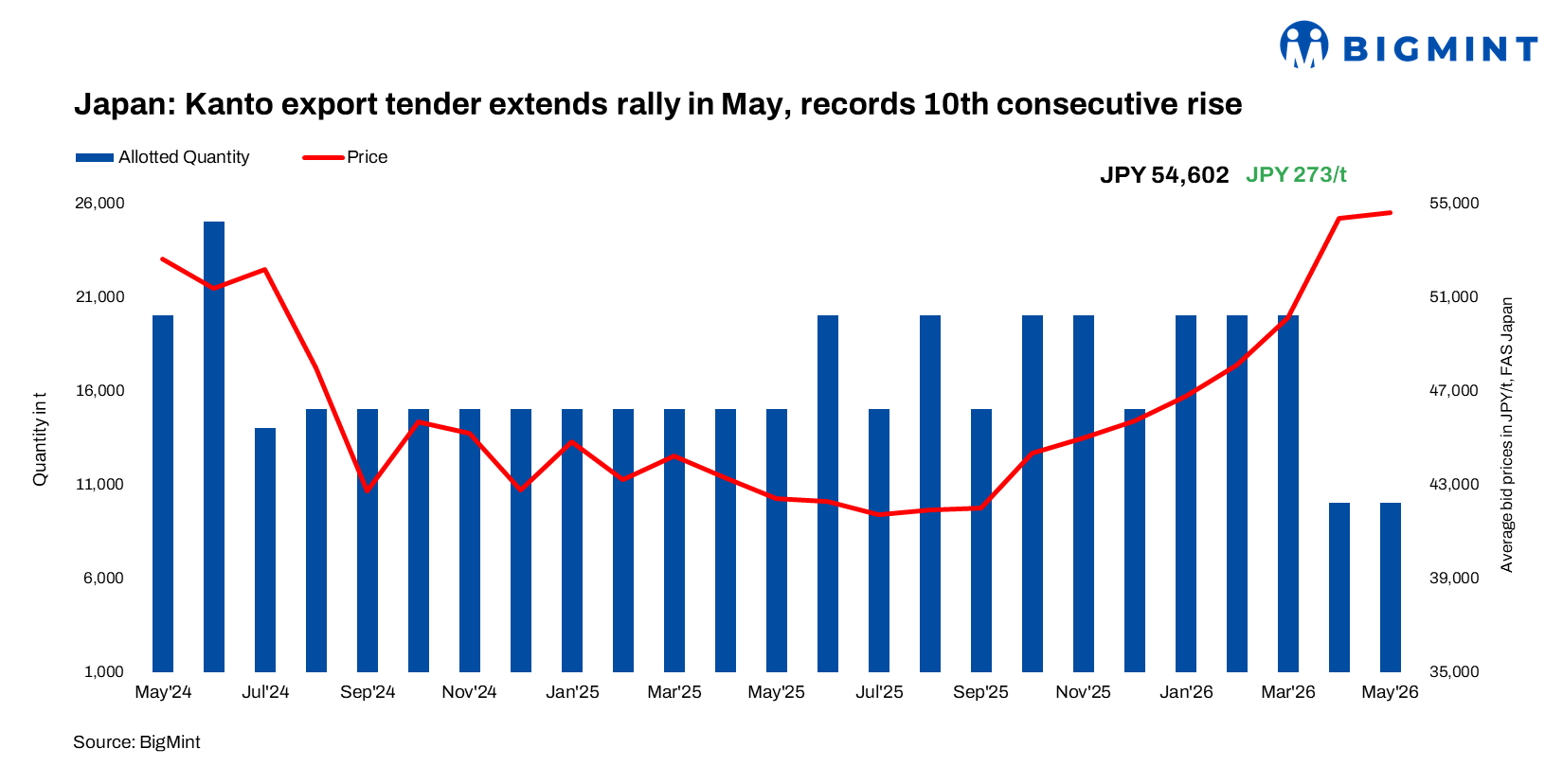

Japan’s Kanto Tetsugen export tender extended its bullish momentum in May 2026, marking the tenth consecutive monthly increase amid firm domestic scrap fundamentals and limited export availability with the winning bid reaching its highest level in more than three years since March 2023. The latest tender concluded with 10,000 t of H2 scrap booked at JPY 54,602/t ($346/t) FAS, up by JPY 273/t ($2/t) m-o-m. The awarded level translates to around JPY 55,500/t ($352/t) FOB Japan.

As per market insiders, out of 15 participating trading companies, 14 submitted a total of 15 bids, while one company abstained. Total bid volume reached 170,000 t, up by 50,000 t m-o-m, marking the 17th consecutive month with bids exceeding 100,000 t and the highest bidding volume since February 2021.

The cargo is understood to have been awarded to a Japanese trading company, with Vietnam likely to be the destination, according to market participants. Notably, the April Kanto tender cargo was also reportedly shipped to Vietnam, indicating continued Vietnamese demand for Japanese-origin scrap.

Meanwhile, the Japanese yen has strengthened modestly against the US dollar over the past month, appreciating from around JPY 159.3/$ on 12 April to nearly JPY 157.6/$ currently. The firmer currency has also contributed to higher export offer levels from Japanese suppliers by lifting dollar-denominated replacement costs.

The cargo is scheduled for export from the Kanto region under May contracts (first bid), with final vessel loading expected by 30 June, market participants informed BigMint. Although the second and third bids were reportedly close in price, concerns over completing shipments within June reportedly led directors to approve only the first cargo.

Market comments

Chairman Minami reportedly stated that tight H2 scrap availability and ongoing collection difficulties continued to support domestic prices, while the final awarded level remained within realistic market expectations. The continued uptrend did not surprise the seaborne market, as Japanese domestic scrap prices have remained firm and spot export availability continued to stay limited.

A regional scrap trader commented: “Japanese export prices continue to remain well supported by firm domestic market conditions and limited spot scrap availability. Exporters are under little pressure to aggressively lower offers, particularly as local mill buying sentiment remains strong.”

Most market participants indicated that Bangladeshi buying interest remained weak, with no major trades heard during the week. Buyers continued to stay away from fresh bookings amid weak finished steel demand, liquidity pressure, and persistent financial constraints.

A Bangladesh-based importer said: “High freight costs, payment delays, and LC-related complications continue to affect import activity. Buyers are cautious and only booking material when absolutely necessary.”

Market participants noted that several exporters have increasingly shifted focus toward Southeast Asian destinations such as Vietnam, Indonesia, and Taiwan, where payment visibility and deal execution remain relatively smoother compared with Bangladesh.

A regional market participant said: “Vietnamese buyers may still be workable around $395/t CFR for H2 scrap, but most Japanese export offers are now heard above $400/t CFR, making fresh transactions difficult at current levels.”

Despite the firm tender outcome, some domestic participants viewed the final awarded price as slightly below earlier expectations, as stronger dollar-denominated export indications to Vietnam had initially fuelled expectations of bids closer to JPY 56,000/t ($355/t). Meanwhile, the 10,000 t cargo booked under the April tender is scheduled for shipment between 15-21 May, with most April-contracted cargoes currently lined up for vessel loading.

Domestic market support and price alignment

In the domestic market, H2 scrap prices were heard at around JPY 53,000-53,500/t ($335-339/t), while dockside collection prices stood at JPY 52,000-52,500/t ($329-332/t) FAS.

Tokyo Steel raised scrap purchase prices by JPY 1,000/t ($6/t) across all plants effective 12 May 2026, taking H2 purchase levels to around JPY 54,000/t ($343/t), while price announcements for the Takamatsu plant remained suspended. The latest upward revision reflects firm domestic scrap fundamentals in Japan, supported by active mill buying, limited scrap generation, and steady export demand following the recent Kanto tender strength.

Outlook

Japanese export scrap prices are expected to remain firm, supported by steady domestic mill buying and tight scrap availability. However, higher Japanese offer levels may continue to face resistance from overseas buyers, especially across East Asia. Market participants are expected to closely track domestic mill price movements and upcoming export negotiations for clearer market direction ahead of the next Kanto export tender, scheduled for 10 June.

Leave a Reply