- Vietnam shows restocking interest but no bulk deals closed

- Taiwanese buyers stay cautious due to sluggish rebar sales

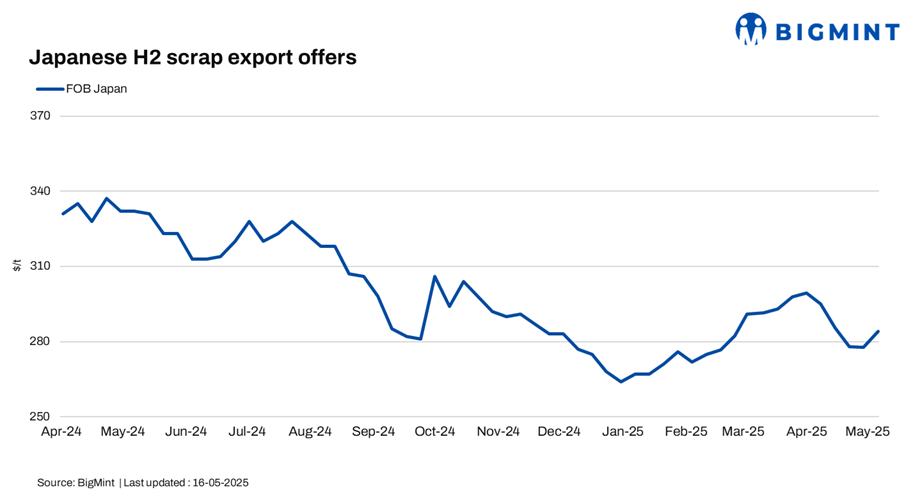

The Japanese H2 scrap export market saw a slight price rise during the week, supported by improved sentiment, a weaker JPY, and firmer billet prices. BigMint assessed Japanese H2 at JPY 41,300/t ($284/t) FOB Tokyo Bay, up JPY 900/t ($6/t) from JPY 40,400/t ($278/t) FOB in the previous week.

The May Kanto tender winning bid at JPY 42,389/t ($292/t) lifted market expectations, signalling a slight recovery in demand. However, trading activity remained subdued due to a persistent bid-offer gap and cautious buying amid US-China tariff concerns and exchange rate volatility.

Vietnamese buyers showed interest in restocking, but no bulk deals were observed. Overall, spot market liquidity was limited, as buyers monitored the market.

In the domestic market, the average H2 scrap price across three major regions in Japan stood at JPY 38,200/t ($263/t) during the first two weeks of May, marking a slight drop of JPY 100/t ($0.68/t) from the previous week. Region-wise, Kansai recorded a decline of JPY 300/t ($2/t) to JPY 38,000/t ($262/t), while prices in Kanto and Chubu remained unchanged at JPY 43,000/t ($296/t) and JPY 36,300/t ($250/t), respectively.

Other market updates

Vietnam: Vietnam’s imported scrap market remained cautious, with buyers largely on the sidelines amid a persistent bid-offer gap and market uncertainty. Offers for Japanese H2 rose to $325-327/t CFR, while bids improved slightly to around $320/t, but no deals were concluded.

There was interest in restocking due to low inventories, yet sentiment was clouded by US-China tariff concerns and currency fluctuations. Bulk HMS 80:20 offers from the US and Australia stood at $350/t and $345/t CFR Vietnam, respectively, with bids holding at $330/t. A blast furnace issue at a local mill may further pressure short-term demand.

Taiwan: Taiwan’s imported scrap market remained cautious and range-bound during the week. Deals for US-origin containerised HMS 80:20 were heard at $285-288/t CFR, with offers nudging up to $290-295/t as suppliers eyed stronger prices. However, sluggish rebar sales and weak domestic demand kept buyers on the sidelines.

The start of electricity rationing further slowed scrap buying, as EAF mills limited daytime production to avoid high power costs. Although a stronger Taiwan dollar made imports more affordable, mills showed little interest in higher-priced Japanese scrap, offered at $310-315/t CFR. Overall, trading stayed thin amid muted sentiment.

South Korea: South Korea’s imported scrap market saw rising tensions in early to mid-May due to tightening supply and falling inventories. Major steelmakers reported a 13% drop in scrap inventories to 809,000 t since late April, triggered by April’s price cuts and reduced logistics activity during holidays. In response, mills such as Hyundai Steel and Dongkuk Steel initiated special purchases and raised prices by KRW 10,000-20,000/t ($7-14/t) to secure volumes.

Despite these hikes, suppliers struggled with structural profitability issues, as higher costs and intense competition eroded margins. While price sentiment improved slightly, the market remained cautious, with steelmakers slowing additional hikes and adjusting volumes amid fragile profitability in the supply chain.

Outlook

Japanese H2 scrap export offers are expected to remain firm amid a weaker JPY, strong billet prices, and restocking interest from Vietnam. However, trading may stay limited due to a persistent bid-offer gap, cautious sentiment over US-China tariff tensions, and exchange rate fluctuations. In Taiwan and Vietnam, despite low inventories, weak downstream demand and high offers may keep buyers on the sidelines, limiting short-term market activity.

Leave a Reply