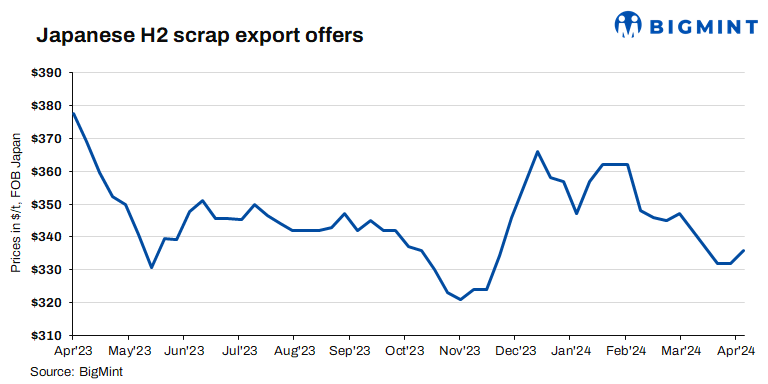

This week, export offers for Japan’s H2 scrap increased, propelled by optimistic forecasts for late April and May shipments. Increased interest from Vietnam and Taiwan, expecting further price hikes in line with global trends, also played a role. Additionally, improved realisations in the domestic market contributed to the price hike, prompting some Japanese suppliers to redirect their focus towards domestic sales.

According to the latest assessment by BigMint, export offers for Japanese H2 scrap stood at JPY 50,600/tonne (t) ($334/t) FOB Tokyo Bay, showing a rise of JPY 400/t ($4/t) compared to JPY 50,200/t ($332/t) FOB reported a week earlier.

Other market updates

Vietnam: Vietnamese mills have shifted their focus towards domestic scrap procurement over seaborne scraps due to bid-offer disparities, alongside higher inventories held by major steel mills, which were booked before the Lunar New Year holidays. Meanwhile, downstream steel demand remained soft, resulting in sluggish scrap consumption.

Prices for domestic type 1 (3-6mm) scrap were reported to be around VND 9,000-9,200/t in the northern region and VND 8,700-8,800/t in the southern region.

Japanese H2 scrap export offers to Vietnam hovered at approximately $375-385/t CFR. Last week, suppliers hiked prices in response to global trends, especially those influenced by Turkiye. Consequently, some buyers secured deals in anticipation of further increases. However, Vietnamese buyers are largely maintaining inventories, with only a few seeking to replenish stocks. Although demand for finished steel remained moderate, suppliers are considering further price hikes. However, uncertainty looms over the absorption of these hikes, given the existing stockpile held by mills.

Taiwan: Taiwan’s largest rebar producer, Feng Hsin Steel, headquartered in Taichung in central Taiwan, decided to raise its rebar list prices and procurement prices for local scrap for transactions over 1-3 April. The mini-mill is offering its 13mm dia rebar at TWD 19,500/t ($608/t) EXW, gaining TWD 300/t on week, and its buying price for local HMS 1 and 2 80:20 scrap reaches TWD 10,900/t after the on-week rise of TWD 200/t.

The price of US-sourced HMS 1 and 2 80:20 scrap was reported at $355/t CFR Taiwan, the same level from one week before, while the price of Japan-origin H2 scrap increased continuously by another $5/t on week to reach $370/t CFR Taiwan.

South Korea: South Korean steel mills have opted to prioritise domestic market purchases over seaborne options due to the availability of cost-effective scrap in the domestic market. Additionally, scrap inventories were reported to be higher this week.

South Korea’s primary steel manufacturers, including POSCO with its Gwangyang and Pohang mills, as well as Daehan and YK Steel, have decided to reduce scrap procurement prices by KRW 10,000/t ($7/t), starting on 4-5 April, 2024. Similarly, Dongkuk, Hyundai, and Welcome Steel have also announced plans to cut scrap purchase prices by KRW 10,000/t ($7/t), effective from 10-11 April, 2024.

Additionally, the combined steel scrap inventory held by the top eight South Korean steel producers amounted to 899,000 t this week, showing an increase of approximately 3% compared to 873,000 t in the previous week.

Outlook

Japanese export offers are expected to face continued pressure in the near term due to several factors. Vietnamese mills are currently maintaining substantial inventories, while Taiwanese buyers are observing holidays for the Qingming Festival and Children’s Day from 4-7 April. Additionally, South Korean buyers continued to prioritise bookings from the domestic market due to their cost-effectiveness.