- Rise in Kanto tender bids boosts Japanese H2 scrap export offers

- Vietnamese buyers resist higher offers amid limited interest

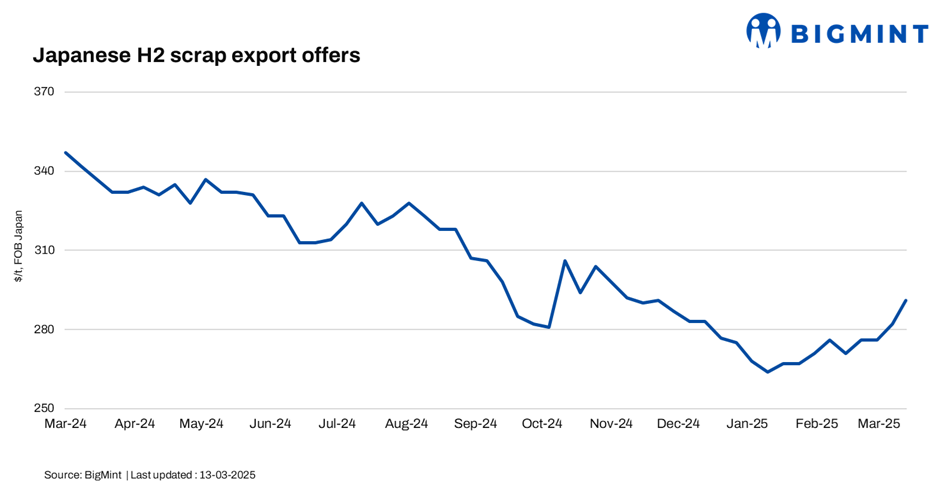

Japanese H2 scrap export offers climbed w-o-w, driven by stronger sentiment following March’s Kanto tender results. The winning bid for H2-grade scrap rose by JPY 1,026/t ($7/t) m-o-m, with a 15,000 t cargo destined for Bangladesh for the fourth consecutive month.

Limited availability further supported prices as suppliers held back, seeking greater clarity. However, traders noted that the tender price could be challenging for Vietnamese mills to match.

Domestic FAS collection prices for H2 scrap remained steady at around JPY 40,300/t ($272/t). Meanwhile, BigMint’s weekly assessment saw Japanese H2 scrap rise by JPY 1,400/t ($9/t) to JPY 43,100/t ($291/t) FOB Tokyo Bay from JPY 41,700/t ($281/t) the previous week.

Japan’s domestic scrap prices remained stable in the second week of March, with the average H2 scrap price across three regions at JPY 38,000/t ($256/t), unchanged from the previous week. Regional trends showed a slight increase in the Kansai region, where prices rose by JPY 200/t ($1.3/t) to JPY 38,800/t ($262/t). Meanwhile, the Chubu region saw prices hold steady at JPY 35,300/t ($238/t), and the Kanto region maintained its level at JPY 40,000/t ($270/t). Despite firm export demand following the March Kanto tender, domestic prices showed limited movement, reflecting a balanced supply-demand scenario in Japan’s scrap market.

Other market updates

Vietnam: Vietnam’s imported scrap market remained sluggish as buyers resisted higher offers after the March Kanto tender. Japanese H2 scrap offers climbed to $340/t CFR Vietnam from $330-335/t CFR in the previous week, but mills showed limited interest, anticipating price adjustments within one to two weeks. Market sentiment received slight support from rising finished steel prices and expectations of increased construction demand in 2025.

However, deepsea scrap remained costly, with US-origin cargoes at $360-365/t CFR, making HS-grade scrap a preferred choice due to its superior quality and flexible lot sizes. With weak demand and elevated costs, some suppliers shifted focus to alternative destinations such as Bangladesh, India, and Turkiye.

South Korea: South Korea’s scrap market remained stable despite a decline in steelmakers’ scrap inventory for the first time in two weeks. Total scrap inventory stood at 609,000 t, down 26,000 t from the previous week, with the central region seeing a sharper drop of 8.2%, particularly at Hyundai Steel’s Dangjin (-12.5%) and Dongkuk Steel (-8%).

The southern region remained nearly unchanged, with POSCO down 1.3% and Hyundai Steel Pohang up 2.3%.

Despite lower inventories, demand remained sluggish due to weak construction activity, leading mills to maintain optimal production levels rather than aggressively restocking scrap. The market held steady, with no major signs of inventory shortages or price volatility.

Taiwan: Taiwan’s imported scrap market remained subdued as mini-mills resisted higher global scrap prices amid weak demand. Feng Hsin Steel, Taiwan’s largest rebar producer, rolled over its rebar and domestic scrap buying prices for 10-14 March, keeping rebar at TWD 18,500/t ($561/t) exw and local HMS 80:20 scrap at TWD 9,500/t.

Despite global scrap prices rising, with US-origin HMS 80:20 climbing up by $5/t to $320/t CFR and Japanese H2 scrap hitting $325/t CFR, buyers showed caution.

Construction steel users avoided stockpiling due to market uncertainties, while weakening Chinese rebar prices further dampened sentiment. Some suppliers sought alternative markets as Taiwan’s sluggish steel demand persisted.

Outlook

Japanese H2 scrap export offers are likely to remain firm in the near term, supported by strong sentiment post Kanto tender and limited supply. However, Vietnamese mills may resist current price levels, delaying trade activity. In South Korea, weak construction demand will keep scrap procurement cautious, despite declining inventories. Taiwan’s market is expected to stay muted as mills hold back on purchases amid sluggish steel demand. Deepsea scrap prices may face resistance in Asia, with buyers favouring alternative grades for cost efficiency.

Leave a Reply