- Tokyo Steel’s price hike fuels Japanese scrap market

- Vietnamese buyers resist high imported scrap prices

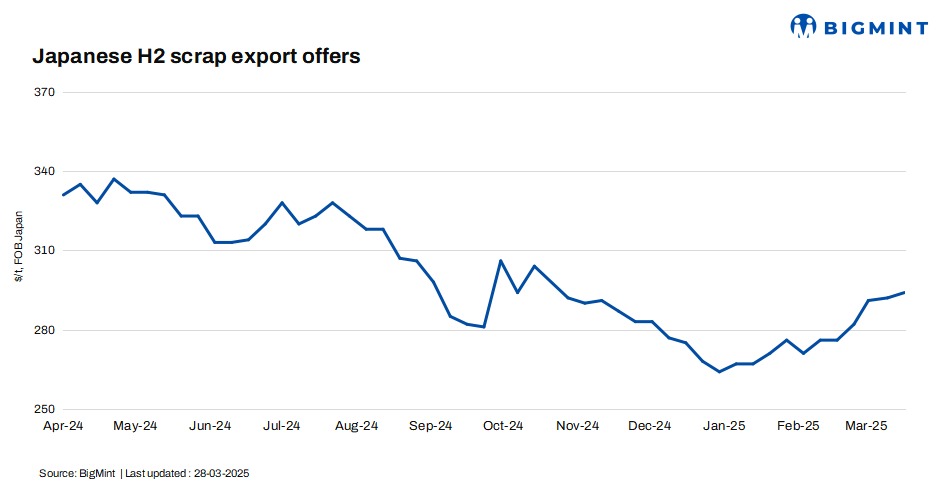

Japanese H2 scrap export offers climbed up this week, supported by stronger market sentiment following Tokyo Steel’s price hike. BigMint assessed Japanese H2 export offers at JPY 44,300/tonne (t) ($294/t) FOB Tokyo Bay, up JPY 800/t ($5/t) from the previous week.

In the past couple of days, Tokyo Steel adjusted its scrap procurement prices twice, raising Utsunomiya’s prices by JPY 1,000/t ($7/t) to JPY 41,000/t ($272/t), effective 26 March 2025, while other plants remained unchanged. Earlier, on 22 March 2025, the mill raised prices at Kyushu, Okayama, and Takamatsu by up to JPY 1,000/t ($7/t). Post-revision, scrap procurement prices at Kyushu stood at JPY 43,000/t ($285/t), Okayama at JPY 42,500/t ($282/t), and Takamatsu at JPY 40,500/t ($269/t).

The increase at Utsunomiya came in the wake of rising seaborne prices, aligning with Tokyo Bay exporters’ higher offers. A mill source noted that Utsunomiya’s prices had been low since maintenance, prompting the adjustment.

Despite a bullish domestic scrap market, suppliers remained cautious, awaiting clearer price direction.

Domestic FAS collection prices for H2 reached JPY 41,000-42,000/t ($272-279/t).

Other market updates

Vietnam: Vietnam’s imported scrap market remained largely stable this week, with moderate buying interest, as mills favoured domestic scrap due to competitive pricing. Japanese bulk H2 scrap offers stood at $335-345/t CFR Vietnam, unchanged w-o-w, but buyers remained firm at $325-330/t CFR. US-origin HMS 80:20 offers at $370/t CFR failed to attract interest amid exchange rate pressures and high import prices. In the domestic market, H1 scrap prices ranged within VND 8,300-9,100/t ($325-356/t) DDP. Meanwhile, rebar prices inched up by VND 100/t ($4/t) w-o-w to VND 13,450/t ($526/t) exw, though overall demand in the construction sector remained moderate.

South Korea: South Korea’s imported scrap market saw a slight rise in arrivals to 53,500 t by the end of March from 50,713 t in mid-March, driven by steady mill demand. Bar steel companies accounted for 49.5% of the total, while special steel sheet firms took 50.5%. Hyundai Steel led with 22,500 t, followed by SeAH Besteel with 21,000 t. Despite this, seaborne scrap demand remained weak due to low mill operation rates, sluggish rebar sales, and bearish construction sentiments. Meanwhile, rising domestic scrap inventory, fuelled by operational curtailments, added further pressure to the market.

Taiwan: Taiwan’s imported scrap market weakened, as US-origin containerised scrap prices dropped by $3-5/t w-o-w to a one-month low of $310-315/t CFR. Limited scrap availability kept offers at $318-325/t, but sluggish rebar sales pressured bids lower. Taiwanese mills preferred cheaper Russian billets, reducing scrap demand.

Feng Hsin Steel cut its rebar list prices and local scrap buying prices to boost sales, with 13 mm dia rebar now at TWD 18,300/t exw. Japanese scrap offers remained scarce, with H1:H2 (50:50) heard at $335/t CFR, but buyers sought $320-325/t. Weak rebar demand and cautious buying sentiment kept Taiwan’s scrap market under pressure.

Outlook

Japanese H2 scrap export offers are likely to remain firm in the short term, supported by Tokyo Steel’s price hikes and stronger domestic sentiment. However, overseas buyers, including Taiwan and Vietnam, may resist higher prices due to sluggish steel demand and preference for cheaper alternatives such as Russian billets.

In Taiwan, weak rebar sales and cautious buying could keep scrap bids subdued despite limited availability. Meanwhile, South Korea’s rising domestic scrap inventory and slow seaborne demand may add further uncertainty. Overall, while Japanese scrap prices could see near-term stability, global scrap market sentiment remains mixed, with demand trends dictating further movements.

Leave a Reply