- Tokyo Steel cut scrap prices by up to JPY 1,000/t in June

- Vietnam’s scrap market stable; mills prefer cheaper Indonesian billets

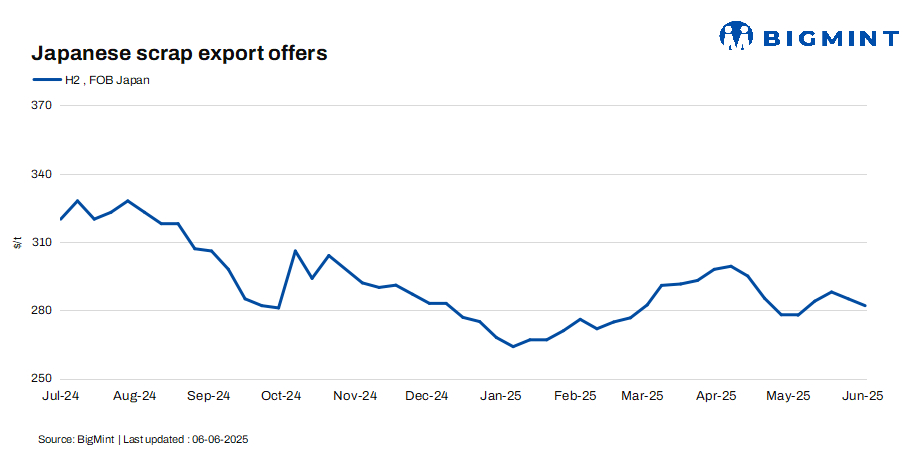

Japanese H2 scrap export prices moved sideways to lower amid continued weakness in downstream demand across major markets. Domestic supplier margins were squeezed as sluggish rebar demand prompted a major local scrap buyer to cut prices twice.

BigMint assessed H2 at JPY 40,600/tonne (t) ($282/t) FOB Tokyo Bay, down JPY 500/t ($3/t) from the previous week’s JPY 41,100/t ($285/t).

Japan’s steel scrap exports rebounded in April, exceeding 700,000 t for the first time in four months. Exports rose 57.3% y-o-y to 716,324 t and increased 14% m-o-m, driven by strong demand from emerging Asian markets. Bangladesh and India also stepped up purchases from Japan in April.

Tokyo Steel lowered its scrap procurement prices twice in early June, cutting rates by a total of JPY 1,000/t ($6/t) at its Kyushu and Kansai plants, and by JPY 500/t ($3/t) at Takamatsu and Okayama. Following the adjustments, H2 scrap prices stood at JPY 39,500/t ($276/t) at Kyushu, JPY 40,500/t ($284/t) at Kansai, and JPY 38,500/t ($270/t) at Takamatsu.

Other market updates

Vietnam: The imported scrap market remained mostly stable w-o-w, with limited buying interest as mills preferred cheaper Indonesian billets–about 80,000 t booked at ~$430/t FOB. While some EAF mills showed mild scrap demand, most held bids firm.

Japanese H2 rose slightly to $322/t CFR. Offers ranged $325-330/t CFR, with bids around $318/t. Fewer Japanese offers emerged amid yen volatility, keeping buyers cautious.

Sentiment remained mildly bearish, with some Southeast Asian scrap diverted to India on stronger demand. Vietnam imported 295,355 t of Japanese scrap in April, scrap imports nearly doubled y-o-y signalling strong buying interest.

South Korea: South Korea’s scrap inventory fell 4% w-o-w to 742,000 t in early June, marking a fifth straight weekly drop. The southern region saw an 8% decline, pressuring mills to run at half capacity due to low stocks, while the central region held more stable. Despite weak imports, prices remained firm, with buyers opting for selective purchases amid regional supply imbalances. A clearer market shift is expected once imports and inventories improve by mid-to-late June.

South Korea’s scrap imports from Japan declined in April 2025 as buyers stepped back amid ample inventories.

Taiwan: Taiwan’s scrap market stayed firm as mills kept domestic scrap prices steady despite weak rebar demand. Feng Hsin Steel cut rebar prices by TWD 200/t for June but held scrap prices at TWD 8,600/t due to high global scrap costs. With the US and Japan witnessing a rise in scrap prices, mini-mills maintained steady scrap bids, while weak demand from China weighed on Taiwan’s steel outlook.

Outlook

Japan’s steel scrap market faces downward pressure amid weak rebar demand and recent domestic price cuts. While April exports rebounded–driven by higher shipments to Vietnam, Bangladesh, and India–JPY volatility has curbed seller interest, and buyers remain cautious. The outlook stays soft, hinging on recovery in downstream demand and regional buying.

Leave a Reply