- Vietnamese, Bangladeshi buyers reduce bids amid caution

- Strengthening JPY, tariff uncertainties weigh on sentiment

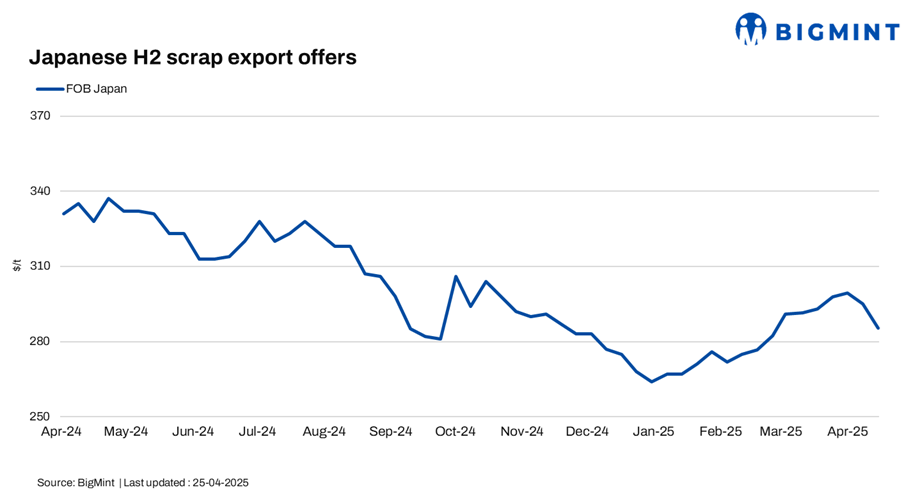

Japanese H2 scrap export offers extended their downtrend this week, pressured by weak demand and hesitant buyer sentiment, which was also reflected in Tokyo Steel’s latest scrap purchase price cuts. BigMint’s weekly assessment of the same stood at JPY 40,900/t ($285/t) FOB Tokyo Bay, down by JPY 1,100/t ($8/t) in comparison with JPY 42,000/t ($293/t) in the previous week.

The strengthening Japanese currency, now at around 143 against the USD, added to the decline, along with ongoing uncertainty surrounding tariff policies. As Turkiye’s deep-sea scrap demand waned, bids from Asian buyers such as Vietnam and Bangladesh also dropped, further widening the bid-offer gap. Sellers struggled to maintain offers amid firm resistance from buyers, which kept spot market activity muted.

Meanwhile, Tokyo Steel – Japan’s top EAF mill – intensified the downtrend by announcing its seventh scrap purchase price cut in April, effective 26 April. The mill reduced prices by JPY 500/t ($4/t) across all plants, bringing the total monthly reduction to JPY 4,500/t ($31/t). Revised prices are as follows:

- Tahara at JPY 41,500/t ($289/t),

- Okayama, Kansai, and Kyushu at JPY 41,000/t ($286/t),

- Nagoya and Utsunomiya at JPY 40,500/t ($283/t), and

- Takamatsu at JPY 39,000/t ($272/t),

According to the latest release from the Japan Iron and Steel Association, the average price of H2-grade scrap iron across three major regions in Japan stood at JPY 39,100/t ($273/t) in the third week of April, marking a JPY 100/t ($0.7/t) decline from the previous week. Region-wise, Kansai saw a slight dip of JPY 100/t ($0.7/t) w-o-w to JPY 38,800/t ($271/t), while prices in Kanto and Chubu remained steady at JPY 48,000/t ($335/t) and JPY 37,800/t ($364/t), respectively.

Other market updates

Vietnam: Vietnam’s imported scrap market saw moderate activity but remained under pressure, as prices slipped amid cautious buying. Japanese H2 scrap dropped slightly to $325-330/t CFR. Notably, a bulk deal of 10,000 t of HS and Shindachi was heard to have been concluded at $360-362/t CFR, while shredded traded lower around $345/t CFR.

Despite steady supplier interest, mills stayed cautious, reacting to falling billet prices and overall weak global sentiment.

On the domestic front, demand showed early signs of recovery with resumed construction activity, but buyers continued to tread carefully, monitoring international trends before committing to larger purchases.

South Korea: South Korea’s ferrous scrap inventory rose for the fifth consecutive week amid weak demand and uneven mill activity. Total inventory at eight major steelmakers increased by 2.7% w-o-w to 929,000 t, the highest level since December 2023.

The central region recorded a 5% w-o-w rise to 512,000 t, while the southern region remained steady at 417,000 t. Notably, the build-up was concentrated at select mills, reflecting company-specific strategies rather than a broad market trend. Major steelmakers announced a KRW 10,000/t ($7/t) cut in scrap procurement prices across key grades, adding further pressure to the domestic scrap market.

Rebar sales in Q1CY’25 declined by 13% y-o-y to 1.55 mnt. Despite lower prices prompting mills to secure material, warehousing is outpacing shipments, resulting in continued inventory accumulation.

Taiwan: Taiwan’s imported scrap market stayed soft, as global prices weakened, and domestic demand remained sluggish. US-origin HMS 80:20 declined by $5/t w-o-w to $303/t CFR Taiwan, while Japanese H2 dropped by $10/t w-o-w to $315/t CFR. The steady decline in Japan-origin offers reflects limited buying interest and increased caution among regional mills.

Feng Hsin Steel, Taiwan’s leading rebar producer, held its rebar list and local scrap procurement prices unchanged for 21-25 April, adopting a wait-and-see approach after reducing rebar and scrap prices by TWD 700/t ($22/t) and TWD 500/t ($16/t), respectively, since late March.

Rebar demand remained weak, as buyers stayed cautious amid global uncertainty. Mainland China’s rebar prices hovered low, further dampening Taiwan’s market sentiment.

Outlook

Japanese H2 scrap export offers are expected to stay weak amid sustained buyer resistance, limited spot activity, and currency-related headwinds. With domestic mills cutting prices and overseas bids softening, especially from key buyers such as Vietnam and Bangladesh, supply-side pressure is set to persist, keeping the market subdued in the short term.

Leave a Reply