- Suppliers hold back offers, wait for higher values

- Tokyo Steel hikes scrap buying tags by up to $10/t

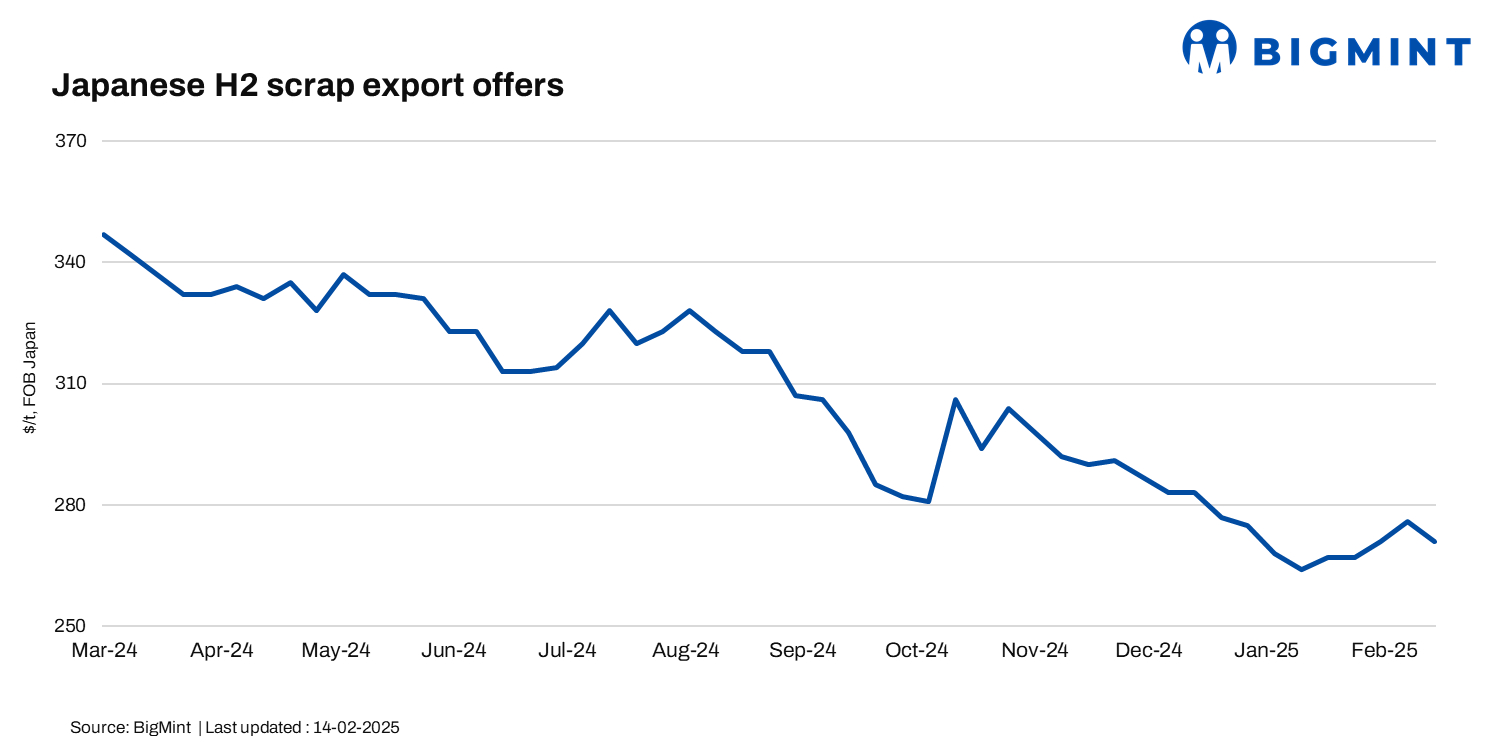

Japan’s H2 scrap export market softened, with prices dipping amid competitive offers and cautious buying. Buyers were hesitant after the recent decline in the Kanto tender price.

A market participant stated, “There are very few offers in the market, as suppliers have decided to wait for higher values.”

BigMint’s latest assessment showed a slight dip of JPY 200/t ($1.3/t), bringing Japanese H2 scrap export prices to JPY 41,400/t ($271/t) FOB Tokyo Bay from JPY 41,600/t ($273/t) last week.

February’s Kanto Iron and Steel Cooperative tender saw bids fall by $10/t (JPY 1,610/t) m-o-m, with a 15,000-t H2 lot awarded to a Bangladeshi mill at JPY 43,200/t ($281/t) FAS.

Despite the decline in export tags, as well as the Kanto tender prices, Tokyo Steel – the largest EAF steel mill in Japan decided to increase its domestic scrap procurement offers for the first time this month, effective 14 February 2025. The adjustments include an increase of JPY 1,000/t ($7/t) at the Okayama plant, JPY 500/t ($3/t) at Kansai, and JPY 1,500/t ($10/t) at Kyushu. Following the revision, H2 scrap prices stood at JPY 42,000/t ($273/t) at Okayama and Kyushu, JPY 41,000/t ($266/t) at Kansai, JPY 40,500/t ($263/t) at Tahara, JPY 40,000/t ($260/t) at Utsunomiya, JPY 39,500/t ($257/t) at Takamatsu, and JPY 39,000/t ($253/t) at Nagoya.

Domestic FAS collection prices for H2 were heard to have remained range-bound w-o-w at JPY 38,500-39,500/t ($252-259/t).

Other market updates

Vietnam: Vietnam’s imported scrap market remained quiet amid a persistent bid-offer gap and sluggish demand. The February Kanto had little impact on Vietnam’s market, as mills found the price uncompetitive. H2 offers ranged within $315-320/t CFR Vietnam, while bids stood at $310/t CFR.

Domestic scrap prices rose due to tight supply and VAT invoice concerns, prompting some mills to increase purchase tags.

Deep-sea scrap prices edged higher, with US-origin offers at $360/t CFR and Australian-origin at $355/t CFR, though liquidity remained thin. Market players largely stayed on the sidelines, monitoring price trends rather than actively procuring scrap.

South Korea: South Korea’s steel scrap market saw price hikes as major steelmakers, including Hwanyang Steel, Daehan Steel, and SeAH Besteel, raised purchase prices by KRW 10,000-15,000/t ($7-$10/t) from 11 February. This move came amid tightening supply, with the combined scrap inventory at eight major mills falling for the seventh consecutive week to 617,000 t. While inventories in the central region dropped 6%, the south saw a 5% rise.

Despite weak demand, mills raised scrap prices to secure supply, but further increases may depend on easing expectations or signs of a price decline, as most brokerage stocks have already entered the market.

Taiwan: Taiwan’s scrap market gained momentum as mini-mills raised procurement prices in response to rising global scrap costs. Feng Hsin Steel, the island’s largest rebar producer, increased its HMS (80:20) purchase prices by TWD 300/t w-o-w to TWD 9,200/t but maintained rebar tags at TWD 18,000/t ($548/t) exw due to weak demand.

US-origin HMS 1&2 (80:20) climbed up by $5/t w-o-w to $310/t CFR Taiwan, while Japan-origin H2 jumped $10/t w-o-w to $315/t CFR. Despite firm scrap prices, sluggish rebar sales and slow post-holiday demand recovery kept mills cautious.

Japanese H1/H2 (50:50) scrap offers were at $325/t CFR, with deals at $315/t CFR.

Outlook

In the near term, Japan’s scrap export market may remain under pressure as buyers adopt a wait-and-watch approach following the Kanto tender decline, though domestic demand could provide some support as Tokyo Steel raises procurement prices. Vietnam’s scrap market is expected to stay subdued amid the ongoing bid-offer mismatch, while tight domestic supply may keep local prices firm. South Korea’s rising scrap prices may continue in the short term due to sustained inventory declines, but weak steel demand could limit further hikes. Taiwan’s scrap market may see stable to firm pricing, though sluggish rebar demand could temper buying activity.

Leave a Reply