- Weak demand from Vietnam pressures H2 tags

- Kanto tender sees $7/t price drop in Apr’25

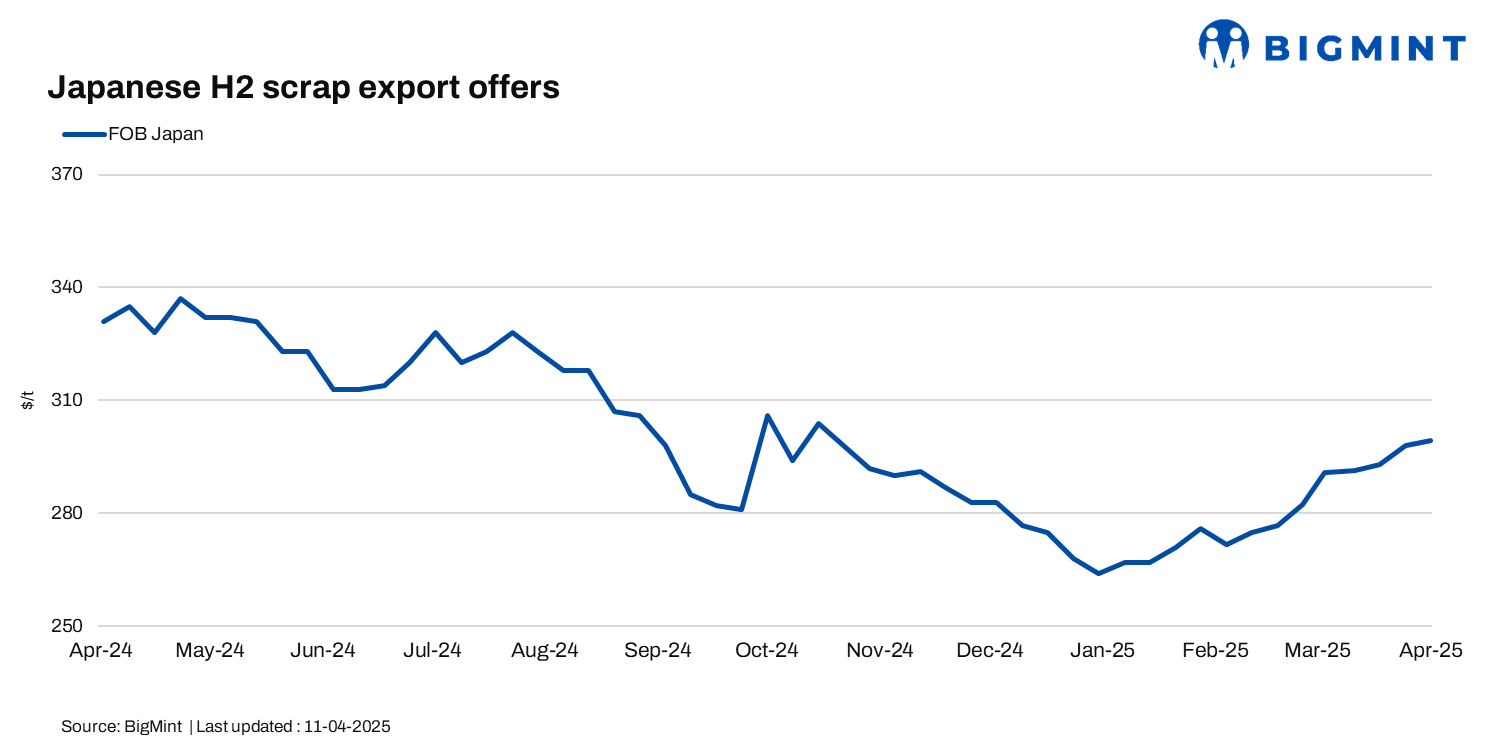

Japan’s H2 scrap export market saw a notable downturn in early April, driven by sluggish overseas demand, currency fluctuations, and growing caution among exporters. The April Kanto Tetsugen tender concluded at JPY 43,288/t ($303/t) FAS, down JPY 938/t ($7/t) from March, reflecting weak appetite from importers, particularly in Vietnam, where buyers continued to press prices down amid thin demand and macroeconomic headwinds.

As a result, BigMint’s latest assessment of Japanese H2 export offers declined by JPY 700/t ($5/t) to JPY 42,800/t ($299/t) FOB Tokyo Bay, down from JPY 43,500/t ($304/t) last week. However, due to the appreciating JPY, the dollar-denominated price remained nearly stable compared to $298/t a week ago.

This week, Tokyo Steel reduced purchase prices at its Kyushu plant by JPY 500/t ($3/t) to JPY 42,500/t ($297/t), citing high inventory levels, a move that further underscored softening domestic and export market sentiment.

Japanese exporters faced resistance in pushing H2 offers above $335/t CFR Vietnam, with tradable levels slipping to $327-330/t CFR. Amid ongoing trade uncertainties and volatile steel prices, many Japanese suppliers adopted a wait-and-watch approach, as JPY appreciation and weak global demand made future price direction increasingly uncertain.

Meanwhile, the average price of H2 across Japan’s three main regions rose to JPY 38,800/t ($271/t) in the first week of April, up JPY 500/t ($3/t) from the previous week. The Chubu (central) region recorded the largest increase, with prices climbing up by JPY 1,500/t ($10/t) to JPY 36,800/t ($257/t). In contrast, prices remained unchanged in the Kanto and Kansai regions, holding steady at JPY 48,000/t ($336/t) and JPY 38,900/t ($272/t), respectively.

Other market updates

Vietnam: Vietnam’s imported scrap market remained subdued during the week amid sluggish steel demand, weakening currency, and mounting uncertainty surrounding tariffs. Japanese H2 scrap prices fell modestly, while the Kanto tender, awarded at JPY 43,288/t ($303/t FAS), which translates to around $330-335/t CFR Vietnam, aligned with prevailing market expectations.

However, buyers remained cautious, pressing tradable levels further down to $327-330/t CFR. Bulk offers from the US hovered at $360-365/t CFR, though bids were below $350/t amid bearish sentiment. With mills largely sidelined and wary of volatile pricing and unclear policy direction, many refrained from booking cargoes, preferring to monitor market signals.

South Korea: South Korea’s imported scrap market continued to face pressure in early April, weighed down by growing inventories and lacklustre finished steel sales. Steelmakers such as Korea Iron and Steel, Daehan Steel, and YK Steel slashed scrap purchase prices by KRW 10/t ($7/t) from 9-11 April, with Hyundai Steel following suit from 12 April and SeAH Besteel initiating cuts from 10 April.

Scrap inventories at eight leading mills jumped 11.2% w-o-w to 853,000 t, underscoring a widening gap between supply and demand. The central region recorded a sharper rise in stockpiles, while the southern region saw a slight dip. Amid softening sentiment and looming price cuts, mills are treading cautiously, limiting scrap intake and maintaining a guarded procurement approach.

Outlook

Japanese H2 scrap export offers are likely to remain under pressure as Vietnamese buyers continue to show limited interest, pushing prices lower amid thin demand and economic uncertainties. The recent Kanto tender decline, combined with Tokyo Steel’s price cuts and high inventories, signals weak market sentiment.

Exporters are expected to stay cautious due to volatile steel prices, an appreciating JPY, and sluggish overseas demand. With mills in key destinations such as Vietnam largely sidelined, further softening in prices appears likely in the short term.

Leave a Reply