- Japan’s Kanto tender sees bids climb to 4-year highs

- Taiwan, Vietnam stay cautious amid cheap billet, rainy season

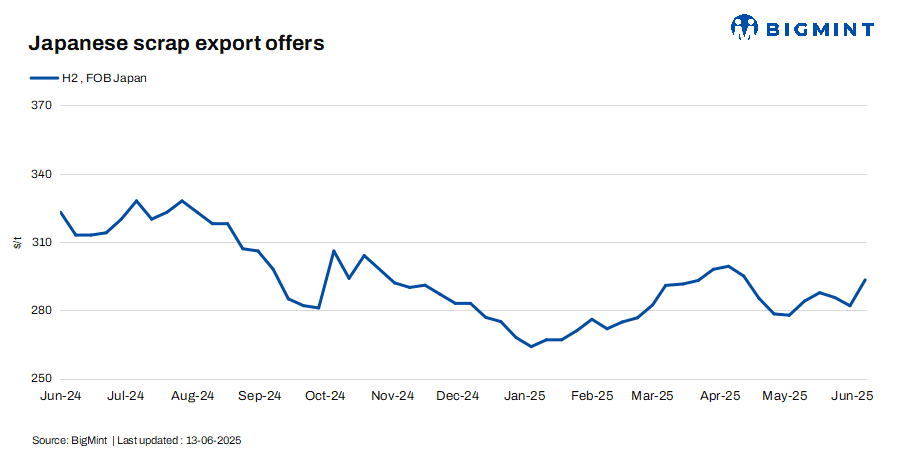

Japan’s H2 scrap export market saw a slight uptick this week, supported by a weaker JPY and active participation in the June Kanto tender, even as global demand remained muted.

The tender awarded a record 20,000 t cargo at JPY 42,267/t ($294/t) FAS — down just JPY 122/t ($0.8/t) from May — likely destined for Bangladesh, with freight rates estimated at $50-55/t. The Kanto Tetsugen association raised the per-vessel cap from 15,000 t to 20,000 t to better serve distant markets amid sluggish domestic demand and lower EAF production. Seventeen bids totaling 163,400 t marked the highest interest in over four years.

BigMint’s weekly Japanese H2 scrap export offers rose by JPY 735/t ($5/t) to JPY 41,335/t ($288/t) FOB Tokyo Bay in comparison with JPY 40,600/t ($283/t) in the previous week.

However, Vietnamese buyers remained cautious due to weak regional demand and the availability of competitively priced Chinese billets. Export bids and offers narrowed across key scrap grades, indicating limited buying appetite. While currency movements lent some price support, overall sentiment stayed subdued amid seasonal slowdowns and broader steel market uncertainty.

Tokyo Steel has announced scrap procurement prices for the third time this month, effective 13 Jun’25. Notably, it has introduced prices for its newly launched Tokyo Bay satellite yard for the first time, offering JPY 41,000/t ($285/t) for special grade scrap. The new yard aims to collect 20,000 t per month, enhancing procurement capacity in the Kanto region and promoting domestic scrap recycling.

The average price of H2 grade scrap iron across Japan’s three major regions fell by JPY 100/t ($0.7/t) in the second week of June, according to data from the Japan Iron and Steel Association. The nationwide average stood at JPY 38,000/t ($264/t). Regionally, Kansai saw the largest drop, with prices down JPY 500/t ($3/t) to JPY 37,400/t ($260/t). Prices in the Kanto and Chubu regions remained unchanged at JPY 42,000/t ($292/t) and JPY 36,300/t ($253/t), respectively.

Other market updates

Vietnam: Vietnam’s imported scrap market stayed quiet this week, with buyers remaining cautious amid regional oversupply and soft demand. Japanese H2 scrap offers were heard at $320-330/t CFR Vietnam, while tradable levels and bids centered around $320/t CFR.

Market participants largely stayed on the sidelines, deterred by ongoing global trade tensions and competitive billet prices from China. Although some mills may make limited purchases to meet production needs, overall sentiment remained bearish. The start of the rainy season in the south and the approach of Ghost Month — when construction and industrial activity typically slows due to cultural beliefs — further weighed on buying appetite. Despite currency fluctuations, market momentum remained weak.

South Korea: South Korea’s imported scrap market remained subdued this week amid weak construction demand and low mill utilization rates. Despite a notable inflow of around 35,000 t of scrap across key ports like Incheon and Gwangyang — mostly H2 and Shredded grades from Japan — the market struggled to gain traction.

Domestic steelmakers leaned on imports due to limited local availability, yet buyers stayed cautious given soft billet prices, tariff uncertainties post-US import duty hike, and volatile exchange rates.

Additionally, local scrap generation dropped 21% m-o-m in May, deepening supply issues. Offers remained stagnant, with no fresh deepsea bookings reported, highlighting continued buyer hesitation.

Taiwan: Taiwan’s imported scrap market remained under pressure this week amid weak local steel demand and falling global scrap prices. Feng Hsin Steel, the island’s largest rebar producer, slashed both its rebar and domestic scrap purchase prices again, citing reduced production costs due to cheaper imported scrap, especially from the US and Japan.

Japanese H2 scrap offers hovered around $318/t CFR Taiwan, but buying interest remained limited due to sluggish construction activity, aggravated by seasonal rains. The overall sentiment remained bearish, with mini-mills cautious amid soft rebar demand and no major rebound in sight for steel or raw material prices in the near term.

Outlook

Japanese H2 scrap export offers may stay supported in the short term due to a weaker JPY and active interest in the latest Kanto tender. However, regional demand remains tepid, with Vietnam, Taiwan, and South Korea showing limited buying appetite amid soft steel markets, cheaper Chinese billets, and seasonal slowdowns. While interest from Bangladesh offers some relief, overall sentiment is likely to stay cautious, suggesting a stable-to-soft outlook unless regional steel demand picks up.

Leave a Reply