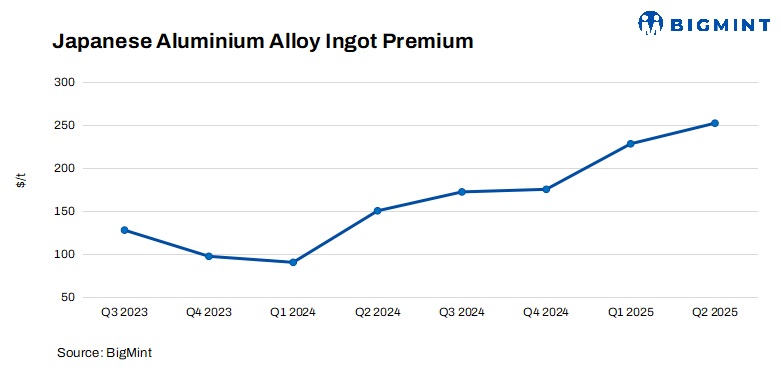

Japan Metal Daily: A global aluminium producer has proposed a $260/tonne (t) premium for Japan’s primary metal shipments in Q2CY’25 (April-June 2025), citing supply concerns following US tariffs, as per Japan Metal Daily.

For the January-March quarter, Japanese buyers agreed to pay a premium of $228/t, the highest in nearly a decade and up 30% from the prior quarter.

Japan is a major Asian importer of aluminium, and the premiums for primary metal shipments it agrees to pay each quarter over the London Metal Exchange cash price set the benchmark for the region.

For Q2, producers have been proposing a premium of $245-260/t, marking a 7.5-14% increase from the previous quarter. If consumers agree to these terms, it will be the first time that the premium falls within the $200/t range for the fifth consecutive quarter.

The increase in the proposed premium reflected concerns that fresh US tariffs on Canadian aluminium could divert supply from the Middle East, Australia, or other regions that typically serve Asia to North America, tightening availability in Asia.

Negotiations for the new quarter began late last week between Japanese buyers and global suppliers, including Rio Tinto and South32, and are expected to continue into the coming weeks.

The US gets most of its aluminium from Canada, and with additional tariffs, the North American aluminium premium is expected to rise. While spot premiums in Asia and Europe have been weak recently, producers are hopeful for a rebound as premiums in North America increase.

Additionally, future US tariffs may cause aluminium shipments intended for other regions to be redirected to North America, which could push premiums higher in other areas depending on supply and demand. If Canadian tariffs are higher than other countries, producers from other nations might send their aluminium to North America, where the premium is higher.

The April-June period tends to see easier settlement of aluminium premiums because many consumers reduce their inventory of raw materials before the fiscal year ends and want to ensure a stable supply after April.

However, some believe prices could drop compared to the previous quarter due to the weak premiums in the spot market, and reaching an agreement could be difficult due to differences between producers and consumers. In the January-March period, some negotiations took longer than expected because of these differing views.

Note: This article has been written in accordance with a content exchange agreement between Japan Metal Daily and BigMint.

Leave a Reply