- Bangladeshi mill returns to the Kanto tender after a two-month pause

- Rising energy costs, policy uncertainty pressure Bangladeshi mills

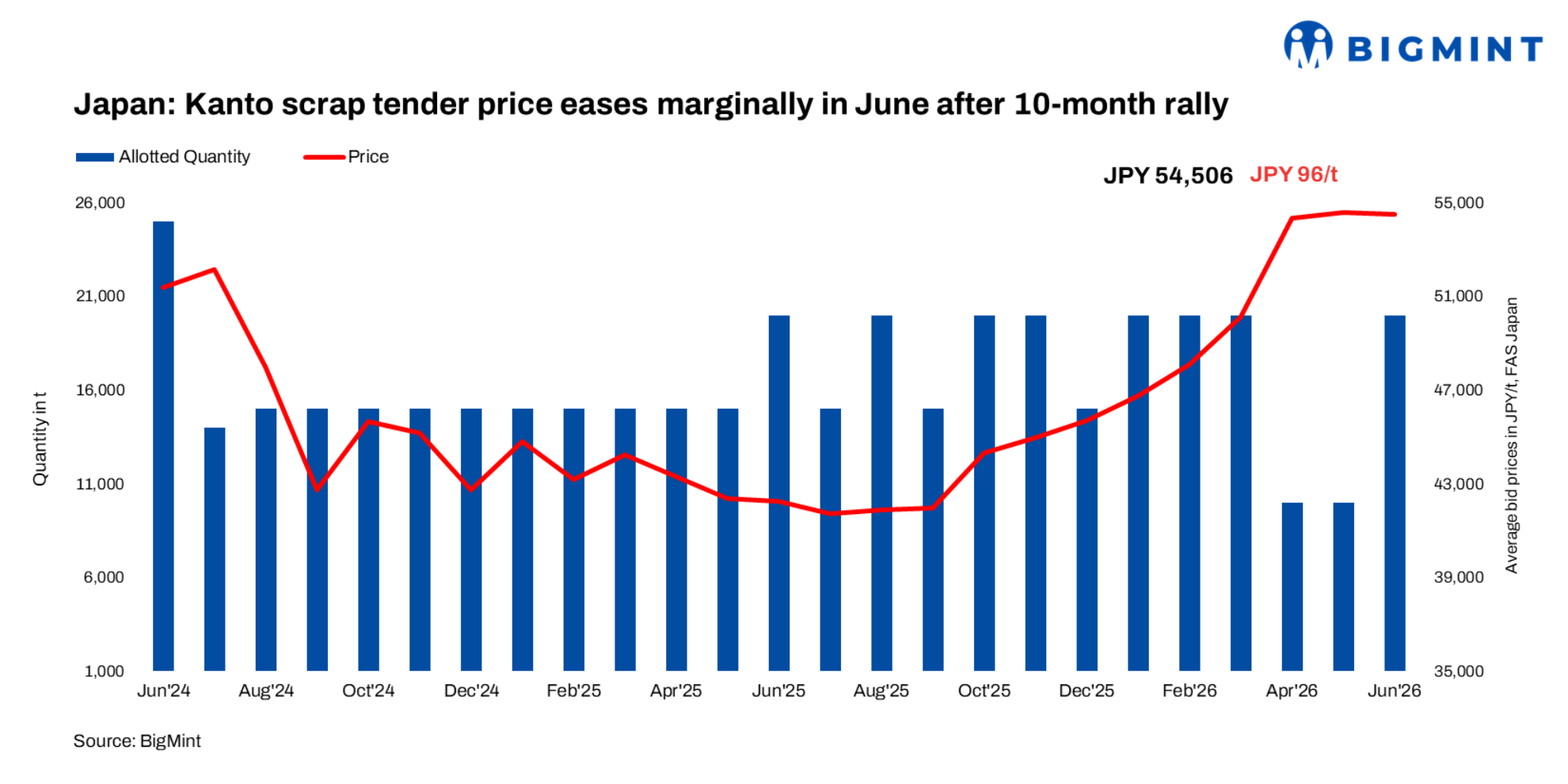

Japan’s June Kanto H2 export scrap tender recorded its first correction after ten consecutive monthly increases, with the settlement easing by JPY 96/t ($1/t) m-o-m to JPY 54,506/t ($340/t) FAS for a 20,000-t cargo. Although the decline marked the first drop in 11 months, the correction was largely nominal, with prices remaining in the JPY 54,000/t ($337/t) range for a third consecutive month.

The latest settlement also remained close to the highest level since the March 2023 tender, when a 20,000-t cargo was awarded at JPY 55,438/t ($345/t) FAS. In dollar terms, however, the June tender value declined by around $6/t m-o-m from approximately $346/t in May.

The latest tender level translates to around $347-348/t FOB Japan and below $400/t CFR Chattogram, with shipment scheduled by 31 July 2026. The softer dollar-denominated price was primarily driven by the depreciation of the Japanese yen, which weakened by around JPY 3/$ from approximately JPY 157.1/$ during the May tender to JPY 160.4/$ in June. The weaker currency helped support export pricing despite softer buying interest across key overseas markets, particularly Vietnam.

The cargo was awarded to a Japanese trading company for shipment to a Chattogram-based mill in Bangladesh, marking the country’s return to the Kanto tender after a two-month absence. The auction received 14 bids totalling 120,400 t against an offered volume of 20,000 t, although the total bid volume was around 50,000 t lower than the previous month.

Despite the decline, bidding volume remained above 100,000 t for the 18th consecutive month.

Domestic Japanese scrap firms up despite export weakness

The decline in the Kanto export tender contrasted with firmer conditions in Japan’s domestic scrap market. Domestic Kanto H2 prices increased by around JPY 1,000/t ($6/t) m-o-m to approximately JPY 54,000/t ($337/t), supported by steady mill demand and relatively tight scrap availability. The tender settlement remained broadly in line with domestic mill purchase prices and slightly above prevailing Tokyo Bay export levels, suggesting limited impact on the domestic market.

Market participants attributed the softer dollar-denominated tender outcome primarily to currency movements. Market sources noted that the offered volume was increased to 20,000 t ahead of seasonal summer production cuts at Japanese electric-arc furnace (EAF) mills, allowing larger export cargoes to be offered.

Bangladesh mills await budget clarity

Bangladesh mills await budget clarity

Despite Bangladesh’s apparent return to the Kanto market, imported scrap buying sentiment remained subdued ahead of the government’s FY’27 budget presentation on 11 June. Market participants expressed concerns that higher electricity surcharges and additional industrial levies could further increase steelmaking costs at a time when margins remain under pressure.

BigMint weekly assessments, CFR Chattogram

- European-origin containerised HMS (80:20): $382/t, down $2/t w-o-w

- European-origin containerised shredded scrap: $418/t, up $5/t w-o-w

- Japanese-origin bulk H2: $403/t, down $12/t w-o-w

- US-origin bulk HMS (80:20): $410/t, down $2/t w-o-w

Indicative offers remained mixed, with Philippines-origin GI bundles heard at $345-350/t CFR Chattogram and UK-origin HMS (80:20) at around $360/t CFR Chattogram. Shredded scrap offers from Australia and the UK were reported at $420-430/t CFR Chattogram, while bids for Australian-origin shredded were heard near $410/t CFR Chattogram — a persistent bid-offer gap and cautious buying sentiment.

Weak construction activity, sluggish real estate investment, and tight liquidity conditions continue to limit steel consumption, keeping buyers cautious. Industry observers believe that measures aimed at improving consumer purchasing power, easing financing costs, and supporting domestic manufacturing could help revive demand and improve sentiment across the steel sector.

Local scrap gains preference

Domestic scrap prices in Bangladesh increased to BDT 55,000-56,000/t ($448-456/t), up from around BDT 50,000/t ($407/t) a week earlier. The sharp rise in local prices has reinforced mills’ preference for domestic procurement despite the recent softening in international scrap markets. Market participants noted that buyers remain focused on preserving liquidity and limiting exposure to policy uncertainty ahead of the FY’27 budget announcement.

A Dhaka-based mill source indicated that a proposed 20-25% increase in power-related charges could significantly impact production economics. Combined with elevated borrowing costs, higher energy prices, and currency depreciation, many mills continue to operate under strained margins amid weak steel demand.

Another Chattogram-based steel mill source noted that recent increases in electricity tariffs have already added around BDT 2,000-4,000/t ($16-33/t) to production costs. Any further hikes, along with higher gas prices and dollar-linked import expenses, are expected to weigh further on profitability.

Local scrap remains the preferred choice for most Bangladeshi mills due to easier availability and quicker deliveries. Weak construction activity and slow steel demand continue to keep buyers cautious, with most mills purchasing only for immediate requirements. Unless imported scrap prices become more competitive or domestic supplies tighten, import activity is likely to remain limited in the near term.

Outlook

BigMint expects Bangladesh’s imported scrap market to remain cautious as mills continue to prioritise liquidity amid weak steel demand, high borrowing costs, and rising energy expenses. While the softer JPY has improved the competitiveness of Japanese scrap, buying activity is likely to remain need-based until there is greater clarity on production costs and policy measures under the FY’27 budget. Market participants will also closely monitor the next Kanto export tender, scheduled for 9 July, for indications on export pricing direction and overseas demand trends.

Leave a Reply