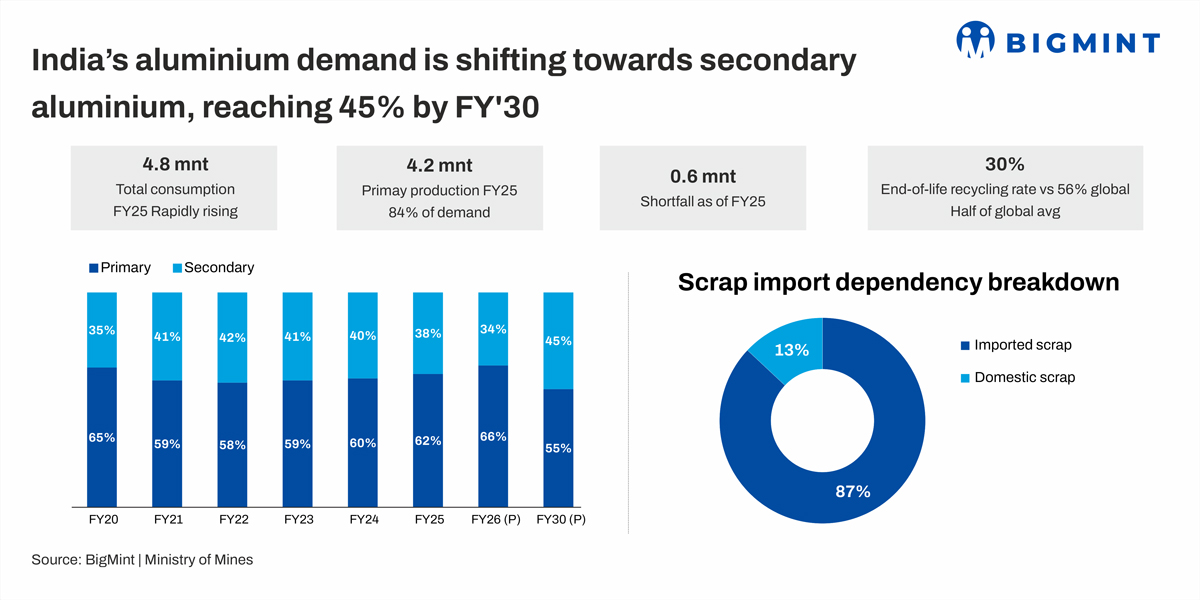

- Aluminium demand was 4.8 mnt, primary production 4.2 mnt, in FY25

- Projected supply shortfall to rise to 1.6 mnt by 2030

- Scrap dependence exposes domestic sector to global risks

India’s aluminium industry is growing rapidly, but its supply structure tells a more complex story. While the country is the world’s second largest producer of primary aluminium, its overall supply remains insufficient to meet domestic demand.

As of FY25, India’s aluminium consumption stood at around 4.8 mnt, while primary production was approximately 4.2 mnt. At first glance, this suggests near self-sufficiency. However, this does not capture the full picture, as a large portion of downstream demand is met through imports of scrap and value-added products.

The supply mix highlights this imbalance. Primary aluminium contributes about 62% of domestic consumption, while secondary aluminium accounts for the remaining 38%, with production at roughly 2 mnt. This growing share of secondary aluminium reflects both cost efficiency and sustainability benefits, but it also introduces new dependencies.

Secondary growth driven by economics but import-dependent

The expansion of secondary aluminium is structurally logical. Recycling aluminium requires up to 95% less energy than primary production, making it far more cost effective in an energy constrained environment. It also aligns with global decarbonisation trends, where recycled metal is increasingly preferred.

However, India’s secondary ecosystem is heavily dependent on imports. Nearly 85-90% of scrap requirements are sourced from international markets. This is primarily because domestic scrap generation remains low, a consequence of historically low per capita consumption of aluminium in India.

At around 3.5 kg per capita, India’s aluminium usage is significantly below the global average of 12 kg, which limits the availability of end-of-life scrap within the country. As a result, even as recycling capacity expands, the sector remains exposed to global supply disruptions and price volatility.

Supply not sufficient even today

Despite being a large producer, India is still not fully self-sufficient in aluminium. Imports account for an estimated 55-60% of total consumption when scrap and downstream products are included.

This gap is driven by two factors. First, domestic production is concentrated in primary metal, while demand is increasingly shifting toward alloys, flat rolled products, and recycled inputs. Second, the secondary sector’s reliance on imported scrap means that domestic production is indirectly dependent on global supply chains.

Supply gap expected to widen by 2030

Looking ahead, demand growth is expected to outpace supply expansion. By 2030, India’s aluminium demand is projected to reach around 8.5 mnt, nearly doubling from current levels.

Primary capacity is expected to increase from 4.2 mnt to around 7 mnt, driven by expansions from major producers. However, even with these additions, there remains a projected capacity shortfall of around 1.6 mnt.

This gap implies continued reliance on imports, particularly for scrap and downstream products. It also suggests that without faster capacity additions or improved recycling systems, supply constraints could tighten further.

Long-term demand creates structural pressure

The long-term outlook presents an even bigger challenge. By 2047, India’s aluminium demand is expected to reach approximately 28 mnt, driven by infrastructure, renewable energy, electric mobility, and industrial growth.

To support this level of demand, the country would require around 37 mnt of production capacity. Based on current trajectories, this leaves a potential supply gap of at least 7 mnt.

This is not just a capacity issue. It reflects deeper structural constraints across raw materials, energy, and recycling systems.

Raw material security remains key bottleneck

India has significant bauxite reserves, but only about 13% are classified as proven. This creates uncertainty around long term raw material availability.

To achieve full self-reliance in aluminium production, India aims to meet 100% of its bauxite and alumina requirements domestically by 2035. However, this will require faster development of mining assets and improved regulatory clarity.

Without secure access to bauxite, scaling primary aluminium production becomes difficult, regardless of installed smelting capacity.

Energy constraints could limit expansion

Energy is the single largest input in aluminium production. Smelting requires approximately 14,000 kWh per tonne, making it one of the most power intensive industrial processes.

To support future growth, the sector will need an additional 15 to 18 gigawatts of power capacity by 2030. The challenge is not just availability, but also the source of power. With global markets increasingly favouring low-carbon aluminium, reliance on coal-based energy could impact competitiveness.

This makes renewable energy integration a critical factor in both supply expansion and market positioning.

Recycling holds the key but needs scale

Improving domestic scrap availability is one of the most effective ways to bridge the supply gap. Currently, India’s end-of-life recycling rate is around 30%, well below the global average of 56%.

Increasing this rate would reduce import dependence, stabilise supply, and lower emissions. However, achieving this requires formalising the scrap collection ecosystem, improving segregation, and incentivising organised recycling.

Without these changes, the secondary sector will continue to grow, but with limited control over its raw material base.

Supply story still in transition

India’s aluminium sector stands at a critical inflection point. While primary production provides scale and secondary aluminium offers efficiency and sustainability, structural challenges across raw materials, energy, and recycling continue to constrain overall supply.

Demand growth remains strong, but the key question is whether supply systems can keep pace. Strengthening domestic scrap availability, securing raw material resources, and expanding energy capacity will be crucial in reducing import dependence.

How has India’s Non-ferrous Metal Scrap Recycling Framework envisaged developing a domestic ecosystem for strengthening scrap supply and reducing import dependence? How will EPR targets for non-ferrous metals, including aluminium, boost generation of scrap? To explore these issues in detail and understand the future of India’s aluminium market, join us at BigMint’s India Non-Ferrous Week in Mumbai on 9-10 June 2026.

Leave a Reply