- Fixture activity remains muted amid holiday season slowdown

- Brazil-China rates rise on long-haul cargoes, tighter vessel supply

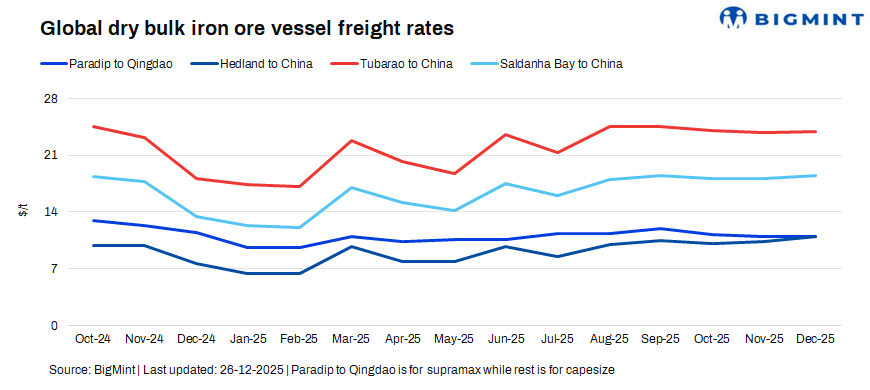

Dry bulk freights across key iron ore routes showed mixed trends w-o-w on 26 December, reflecting uneven cargo demand, ample tonnage availability, and limited fixture activity due to the holiday season, as charterers largely stayed on the sidelines towards the year-end.

Activity softened across most segments, with slower trading and fewer fresh fixtures amid Christmas and year-end holidays, leading to muted vessel demand. While some concluded forward freight agreements (FFAs) continued to signal optimism for early 2026, near-term fundamentals remained weak, constrained by fleet growth, subdued cargo volumes, and seasonal slowdown.

Supramax freights eased due to slower iron ore and minor bulk enquiries from India’s east coast, coupled with comfortable vessel availability in the Indian Ocean. The decline in Paradip-China rates came amid a wait-and-watch approach by charterers during the holiday period, with softer Chinese steel demand limiting fresh fixtures.

Capesize freight sentiment remained cautious overall. Pacific rates weakened, with Australia-China freights falling, as steady but unaggressive iron ore shipments met improving tonnage availability and thin holiday fixing. In contrast, Brazil-China rates edged higher, supported by long-haul cargoes and relatively tighter vessel supply, while South Africa-China rates slipped on softer demand and sufficient tonnage.

China’s steel output slumped in November to multi-year lows even as iron ore imports surged to potentially record levels, reinforcing the view that stockpiling and restocking — rather than immediate steel demand growth — are driving flows.

Notably, some commercial disputes continued to affect iron ore shipping, with a few vessels delayed at Chinese ports due to paperwork and timing issues. While these disruptions may temporarily affect port turnaround times and regional vessel supply, their impact on rates remained limited amid overall weak seasonal fixing activity.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China fell by $0.1/dry metric tonne (dmt) w-o-w to $10.5/dmt on 26 December.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China inched down by $1.5/dmt w-o-w to $9/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments increased by $0.51/dmt w-o-w to $23.61/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao decreased by $0.63/dmt w-o-w to $17.09/dmt.

Market highlights

- Baltic index falls w-o-w: The Baltic Exchange’s dry bulk index (BDI) declined by 223 points w-o-w to 2,071 as of 18 December, pressured by softer year-end cargo demand, slower iron ore and coal fixing, and rising vessel availability, particularly in the Atlantic. The Capesize segment slipped 305 points to 3,319 amid muted iron ore bookings, while Panamax and Supramax rates eased on weaker coal and grain inquiries and cautious chartering activity.

- Brent crude futures fall w-o-w: Brent crude oil futures fell by around $2.13/bbl w-o-w to $62.33/bbl for the February 2026 contract on 26 December, driven by concerns over sluggish global demand, ample supply outlook, and easing geopolitical risk premium, alongside a stronger dollar weighing on prices.

- DCE iron ore futures decline w-o-w: Iron ore futures on the Dalian Commodity Exchange closed at RMB 783/t ($111.4/t) on 26 December, down RMB 1/t w-o-w, as steel demand remained weak amid the seasonal slowdown, cautious restocking by mills, and stable port inventories, limiting near-term price support.

Outlook

Iron ore freights may soften modestly next week, with the possibility of selective support on long-haul iron ore routes if cargo programmes pick up post-holidays. Overall, the market is likely to stay cautious, with movements limited to a narrow range, until chartering activity ramps up in early January.

Leave a Reply