- Freight momentum improving despite mixed route performance

- Improved demand in winter season have kept BDI firm

Iron ore freight rates strengthened across major Capesize and Supramax routes w-o-w, supported by steady Chinese demand, stabilising chartering activity, and gradually tightening vessel availability. Market activity picked up across both the Atlantic and Pacific basins, with more cargo inquiries and improving export visibility as mills continued winter restocking and forward demand became clearer.

Capesize segment steadies with mixed route movements

Capesize rates displayed a firmer tone overall as charterers returned with fresh requirements and weather disruptions eased. On the key Australia-China route, freights edged up, reflecting improved activity in Western Australia. Rates on the South Africa-China route also strengthened, supported by tightening tonnage and healthier fixture momentum. However, the Brazil-China route saw a marginal decline, amid slightly softer inquiry levels for long-haul cargoes despite stable fundamentals.

Supramax segment remains firm on robust minor bulk demand

Supramax freight on the India (Paradip)-China route continued to strengthen, driven by steady minor bulk flows, balanced supply-demand conditions, and consistent activity in the Indian Ocean.

Forward curves reinforce bullish sentiment

Forward Freight Agreements (FFAs) for both Capesize and Supramax contracts trended higher, indicating market expectations of tightening fundamentals and stronger cargo demand through late November and into December.

Higher bunker costs add pressure

Bunker prices have inched higher in recent sessions, adding fresh cost pressure for shipowners across major trading regions. The uptick tracks firmer crude oil sentiment, with Brent crude futures rising w-o-w by about $0.94/bbl to $63.17/bbl on 28 November, lifting marine fuel benchmarks alongside. Tightness in certain bunker hubs also contributed to the increase, raising operating expenses – particularly for longer-haul voyages. The rise in bunker costs has added another layer of pressure to freight economics, weighing on sentiment in an already cautious market.

Route-wise updates

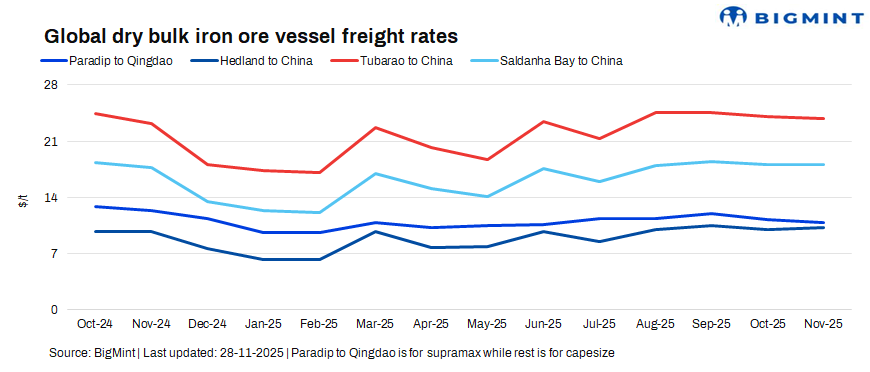

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China rose by $0.12/t w-o-w to $11.3/dry metric tonne (dmt) on 28 November.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China inched up by $0.2/dmt w-o-w to $10.98/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments down by $0.08/dmt w-o-w at $24.63/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao increased by $0.11/dmt w-o-w to $18.71/dmt.

Market highlights

- Baltic index continues its upward momentum w-o-w: The Baltic Exchange’s dry bulk index (BDI) rose 210 points this week to 2,480 as of 28 November. The Capesize segment drove the gains, jumping 589 points to 3,647, while the Panamax index added 50 points to 1,962 and the Supramax index inched up 2 points to 1,435. The rise was largely supported by stronger iron ore chartering, improved Atlantic activity, and tighter vessel availability in the Capesize segment, alongside steady demand in the mid-size sectors.

- DCE iron ore futures surge w-o-w: Iron ore futures on the Dalian Commodity Exchange (Jan’26 contract) closed at RMB 794/t ($112/t) on 28 November, marking a w-o-w increase of RMB 8.5/t ($1.2/t).

Outlook

Iron ore freight rates are expected to stay firm with slight upside in the near term, supported by steady Chinese demand, tightening vessel supply and improving chartering activity. Capesize sentiment remains mildly bullish on winter restocking and stable inquiries from Australia and South Africa, while Brazil-China rates may stay rangebound. Supramax levels in the Indian Ocean are likely to remain strong on consistent minor bulk flows and balanced tonnage.

Leave a Reply