- Holiday slowdown weighs on iron ore freights

- Spot rates under pressure across major routes

Iron ore freight sentiment weakened this week as year-end and New Year holidays curtailed fixture activity, leaving charterers largely absent and spot rates under pressure. Ample tonnage availability, particularly in the Pacific, combined with a lack of fresh cargo enquiries intensified competition among owners, driving freights lower across major routes. Weak Chinese steel output indicators further dampened near-term sentiment, reinforcing a cautious, wait-and-see approach despite steady underlying trade flows.

Spot cargo demand was subdued as steel mills and traders delayed procurement decisions during the year-end and early-January holiday period. This led to thin fixing volumes across major routes, limiting chartering activity.

At the same time, ample vessel availability, particularly in the Pacific basin, increased competition among shipowners. The accumulation of open tonnage meant that available cargoes were insufficient to absorb supply, forcing owners to accept lower rates.

Freight sentiment also remained weak even as iron ore futures strengthened, as higher prices were largely driven by restocking expectations rather than immediate consumption. Market participants viewed recent import volumes as inventory-led, reducing urgency to secure vessels.

Capesize routes faced the most pressure, with slower fixing momentum on Australia-China, Brazil-China, and South Africa-China trades. This weakness spilled over into the Supramax segment, where softer demand from India’s east coast and Southeast Asia, combined with comfortable vessel supply, kept freight rates biased lower.

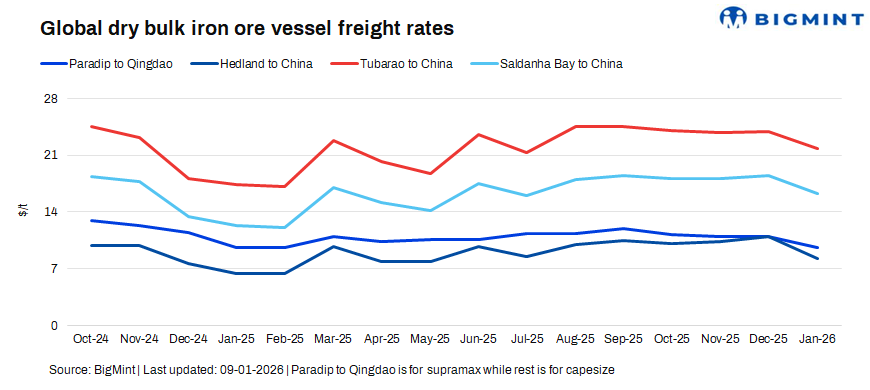

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China fell by $0.1/dry metric tonne (dmt) w-o-w to $9.5/dmt on 9 January.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China declined by $0.5/dmt w-o-w to $8/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments dropped by $0.5/dmt w-o-w to $21.5/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao down by $0.4/dmt w-o-w to $16/dmt.

Market highlights

- Baltic dry index falls w-o-w: The Baltic dry index fell by 8.7% (164 points) w-o-w to 1,718 on 8 January. The index has weakened recently, slipping to its lowest level in over two months as Capesize and Supramax rates soften despite some Panamax support. This reflects weaker cargo enquiry and ample vessel supply in early January.

- Brent crude futures rise w-o-w: Brent crude oil futures rose by around $1.38/bbl w-o-w to $62.63/bbl for the March 2026 contract on 9 January, supported by improved risk sentiment, expectations of firmer demand post-holidays, and supply discipline from major producers, which offset concerns around ample global inventories.

- DCE iron ore futures increase w-o-w: Iron ore futures on the Dalian Commodity Exchange rose by RMB 27.5/t w-o-w to RMB 817/t ($117/t) on 9 January, driven by restocking ahead of the Lunar New Year, relatively firm steel margins at Chinese mills, and expectations of tighter near-term supply due to weather-related disruptions at key export regions.

Outlook

Iron ore freight sentiment is expected to improve gradually after the holiday period, as chartering activity resumes and deferred cargo programmes re-enter the market. Restocking ahead of the Lunar New Year and firmer iron ore prices should support near-term demand, helping lift fixture volumes and vessel utilization.

However, ample vessel availability, especially in the Pacific, may cap the upside, limiting the pace and extent of rate recovery. Capesize rates are likely to stabilise first, with modest gains on major routes, while Supramax and Panamax markets may see a slower, more uneven recovery.

Overall, the market is likely to transition from bearish to neutral-to-firm in the coming weeks, with gradual rate improvement contingent on sustained cargo flow momentum and clearer signals of steel demand recovery from China.

Leave a Reply