- Australia-China route witnesses fixtures at higher levels

- Baltic dry index remains volatile ahead of China holiday

Dry bulk iron ore freight rates showed mixed movements during the week, as softer cargo demand and rising vessel availability continued to weigh on sentiment, particularly in the Capesize segment.

Capesize freight markets remained under pressure as iron ore shipment volumes from key exporting regions – Australia and Brazil – slowed. Miners displayed limited urgency to fix vessels amid stable inventories and muted price signals. Although the West Australia-China route saw marginal improvement, broader fundamentals remained weak due to cautious Chinese buying and seasonal disruptions around the Lunar New Year.

Chinese steel mills maintained a conservative procurement strategy, supported by comfortable port inventories and narrowing steel margins. The lack of aggressive restocking reduced spot fixtures on major long-haul routes such as Brazil-China and South Africa-China, further limiting rate upside.

On the supply side, increased ballasting and ample prompt tonnage in both the Pacific and Atlantic basins intensified competition among shipowners. The oversupply of vessels exerted downward pressure on voyage rates and time charter equivalents, especially for long-haul Brazil trades where fresh cargo volumes were insufficient to absorb available capacity.

Weaker iron ore futures and softness across the broader commodities complex also dampened charterers’ appetite to commit at higher freight levels. While cargoes provided temporary support, they were insufficient to offset the broader imbalance between demand and vessel supply.

In contrast, the Supramax segment displayed relative resilience earlier in the week, supported by diversified minor bulk flows and shorter-haul trades. However, even this segment faced some rate corrections amid evolving regional dynamics.

Route-wise updates:

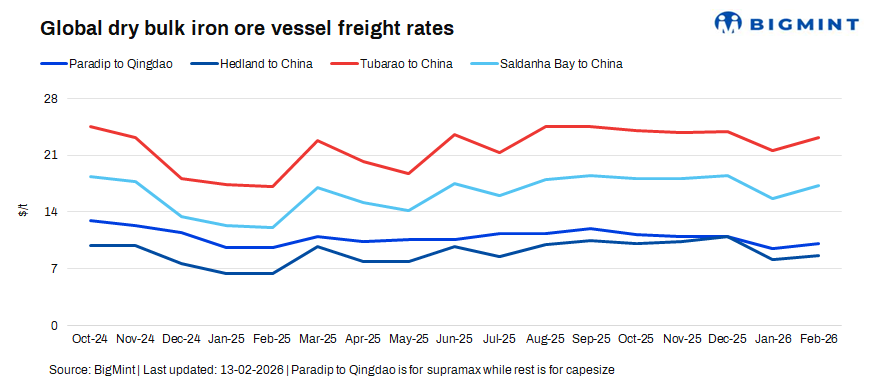

- India (Paradip)–China (Qingdao), Supramax: Freight rates declined by $0.9/dmt w-o-w to $9.6/dmt on 13 February, reflecting easing momentum despite steady regional demand.

- Australia (Port Hedland)–China (Qingdao), Capesize: Rates edged up by $0.2/dmt w-o-w to $8.5/dmt, supported by intermittent cargo flows from Western Australia.

- Brazil (Tubarao)–China (Qingdao), Capesize: Freight rates fell by $0.5/dmt w-o-w to $23/dmt, pressured by limited fresh cargoes and abundant vessel supply on long-haul routes.

- South Africa (Saldanha Bay)–China (Qingdao), Capesize: Rates eased by $0.4/dmt w-o-w to $17/dmt, amid subdued cargo demand and competitive tonnage availability.

Market highlights:

- Brent crude oil futures drop marginally w-o-w: Brent crude oil futures eased around $0.07/bbl w-o-w to $66.91/bbl for May 2026 contract on 12 February. Crude oil futures edged lower w-o-w mainly due to concerns over softer global oil demand outlook and ample supply availability in the market. Cautious sentiment was also influenced by mixed economic signals from major consuming regions and expectations of stable-to-higher output from key oil-producing countries, which together limited upward price momentum.

- DCE iron ore futures drop w-o-w: Iron ore futures on the Dalian Commodity Exchange declined by RMB 14.5/t ($2.1/t) w-o-w to RMB 746/t ($108.1) on 13 February, amid cautious steel demand prospects and elevated port inventories in China.

- Baltic index surges w-o-w: The Baltic Dry Index rose by 159 points w-o-w to 2,095 on 12 February, supported by stronger Capesize charter rates and improved cargo volumes, particularly for iron ore and coal shipments, which tightened vessel availability.

Outlook

The near-term outlook for dry bulk freight for Capesize are likely to remain under pressure due to ample vessel availability in both the Pacific and Atlantic basins, coupled with measured iron ore procurement by Chinese mills. Seasonal factors post-Lunar New Year and comfortable port inventories in China may continue to cap aggressive restocking. However, any pickup in iron ore shipments from Brazil or weather-related disruptions in Australia could trigger short-lived rate spikes given the sensitivity of long-haul tonne-mile demand. Supramax and Panamax segments may show comparatively better resilience, supported by diversified minor bulk flows (coal, fertilizers, grains) and shorter-haul regional trades, which provide some buffer against iron ore volatility.

Leave a Reply