- Market sentiment turns bearish on falling FFAs, thin Pacific inquiries

- Weaker Atlantic fixtures, rising vessel availability pressure rates

Iron ore freight rates declined across key routes in the week ended 12 December, weighed down by softer Chinese demand, reduced chartering activity, and improving vessel availability. Market sentiment turned cautious in both the Atlantic and Pacific basins as winter restocking momentum eased, and forward demand visibility weakened. Lower cargo inquiries and slower fixture flow contributed to an overall softening in freight levels.

Indian Ocean Supramax market cools

The Supramax market in the Indian Ocean softened, with freight on the India (Paradip)-China route losing momentum. A dip in minor bulk volumes, coupled with improving vessel availability, kept rates under pressure despite pockets of steady demand.

Sharp fall in FFA rates

A significant decline in Capesize freight derivatives (FFA) pressured spot sentiment, prompting charterers to reduce bids and owners to accept lower levels.

Limited fresh cargo demand in Pacific

Despite healthy interest from major Australian iron ore miners, overall Pacific cargo inquiries remained thin, leading to multiple fixtures concluded at progressively lower numbers.

Ample vessel availability across basins

A steady replenishment of open tonnage-especially after earlier fixtures-added supply pressure, preventing rate recovery even as fresh orders emerged.

Atlantic weak despite cargo flow

Although a burst of Brazil and West Africa fixtures occurred, rates were fixed below last done, reflecting softening sentiment and lower bids from charterers. Clear-out of South Atlantic requirements did little to support rates as fresh cargoes entered at weaker indications.

Subdued activity out of South Africa

Low trading activity from Saldanha Bay kept regional rates under pressure, contributing to broader weakness.

Route-wise updates

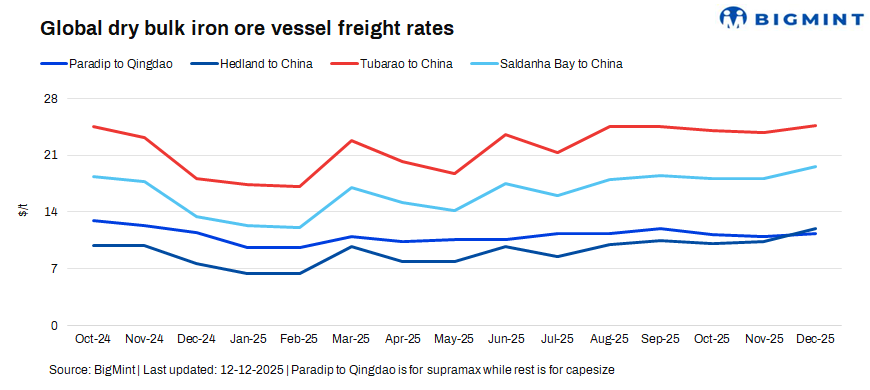

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China rose by $0.6/t w-o-w to $11/dry metric tonne (dmt) on 12 December.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China inched down by $1.52/dmt w-o-w to $11/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments fell by $2.82/dmt w-o-w at $23/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao decreased by $2.65/dmt w-o-w to $18/dmt.

Market highlights

- Baltic index trends down w-o-w: The Baltic Exchange’s dry bulk index (BDI) significant drop of 521 points this week to 2,294 as of 11 December. The drop is driven by weaker iron ore demand, ample vessel supply, and falling FFAs-combined with muted Panamax and Supramax activity to weigh heavily on overall dry bulk market sentiment.

- Brent crude futures drop w-o-w: Brent crude oil futures slipped lowered by around $1.47/barrel (bbl) w-o-w to $61.68/bbl on 12 December 2025 from $63.15/bbl on 04 December. Brent crude futures eased w-o-w as softer global demand sentiment, rising US crude inventories, and a stronger dollar weighed on market outlook, while steady supply from major producers kept prices under pressure.

- DCE iron ore futures decline w-o-w: Iron ore futures on the Dalian Commodity Exchange (Jan’26 contract) closed at RMB 760/t ($108/t) on 12 December, marking a w-o-w dip of RMB 25/t ($3.5/t). DCE iron ore futures dipped w-o-w as weaker Chinese mill demand, rising port inventories, softer steel prices, and cautious sentiment ahead of winter output controls weighed on market sentiment.

Outlook

Iron ore freight rates are expected to stay under pressure as weak FFA sentiment, thin Pacific cargo volumes, and abundant vessel supply overshadow any seasonal restocking support. Minor stabilisation is possible, but a sustained rebound appears unlikely without stronger Chinese demand.

Leave a Reply