- Capesize rates fall on soft Chinese demand, improved vessel supply

- Smaller vessel rates remain firm on steady minor bulk movements

Iron ore freight sentiment weakened this week, as Capesize rates across major routes drifted lower amid softer Chinese demand and improving vessel availability. Although winter restocking continued, the pace of chartering slowed, pulling down long-haul freights and weighing on overall market tone.

A decline in fixtures was witnessed this week, with the market remaining dull. Export activity was uncertain, and high-grade iron ore supply tightened, but demand was not strong enough to lift freight levels.

Capesize market faces pressure as demand eases: Capesize freights on key iron ore routes — Australia-China, Brazil-China, and South Africa-China — declined w-o-w as chartering activity moderated. Improving weather conditions and easing congestion in Brazil and Australia increased vessel availability, adding downward pressure on rates.

Supramax segment steady despite broader weakness: Supramax rates on the India-China route remained stable, supported by balanced supply-demand conditions in the Indian Ocean. While Capesize softness influenced overall sentiment, regional Supramax fundamentals held firm due to steady minor bulk movements.

FFAs reflect uptrend: Forward Freight Agreements (FFAs) for Capesize contracts were up slightly, indicating expectations of stabilisation ahead of peak winter demand. Supramax FFAs remained largely unchanged, in line with muted physical market activity.

Bunker prices add mild cost pressure: Bunker fuel prices edged higher this week, adding slight upward pressure on voyage costs. Demand remained firm in major bunkering hubs such as Singapore and Fujairah, supported by stable crude oil prices.

Route-wise updates

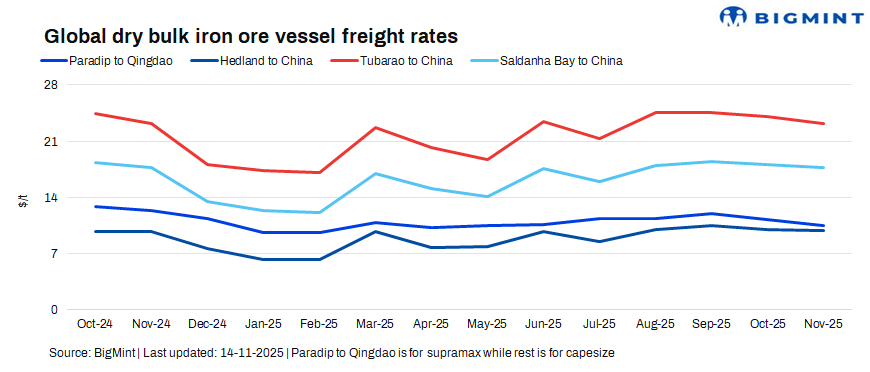

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China remained stable w-o-w at $10.50/dry metric tonne (dmt) on 14 November.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China dropped by $0.3/dmt w-o-w to $9.8/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments were lower by $0.22/dmt w-o-w at $22.98/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao declined by $0.13/dmt w-o-w to $17.67/dmt.

Market highlights:

- Baltic index slips w-o-w following Capesize fall: The Baltic Exchange’s main dry bulk index slipped this week, falling 27 points w-o-w to 2,077 as of 14 November. The Capesize segment saw the sharpest correction, down 208 points to 3,133, driven by softer iron ore demand and easing congestion in key exporting regions. However, the smaller vessel segments strengthened on improved coal movements and steady grain demand.

- Brent crude oil futures drop w-o-w: Brent crude oil futures inched down slightly w-o-w by about $0.2/barrel (bbl) to $63.8/bbl on 14 November 2025 against $64/bbl on 7 November. Brent crude edged down w-o-w as weak demand sentiment and lingering oversupply concerns outweighed any support from geopolitical risks, keeping prices slightly softer.

- DCE iron ore futures decline w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract closed at RMB 772.5/t ($109/t) on 14 November, down RMB 12/t ($1.6/t) w-o-w.

Outlook:

Iron ore freights are expected to remain under mild pressure in the near term as vessel availability improves and Chinese buying remains cautious. However, winter restocking and steady export flows from Australia and Brazil may offer limited support, keeping the market range-bound with a slightly soft bias.

Leave a Reply