- Global primary nickel output may hit 3.735 mnt in 2025

- Indonesia to lift NPI output despite market uncertainty

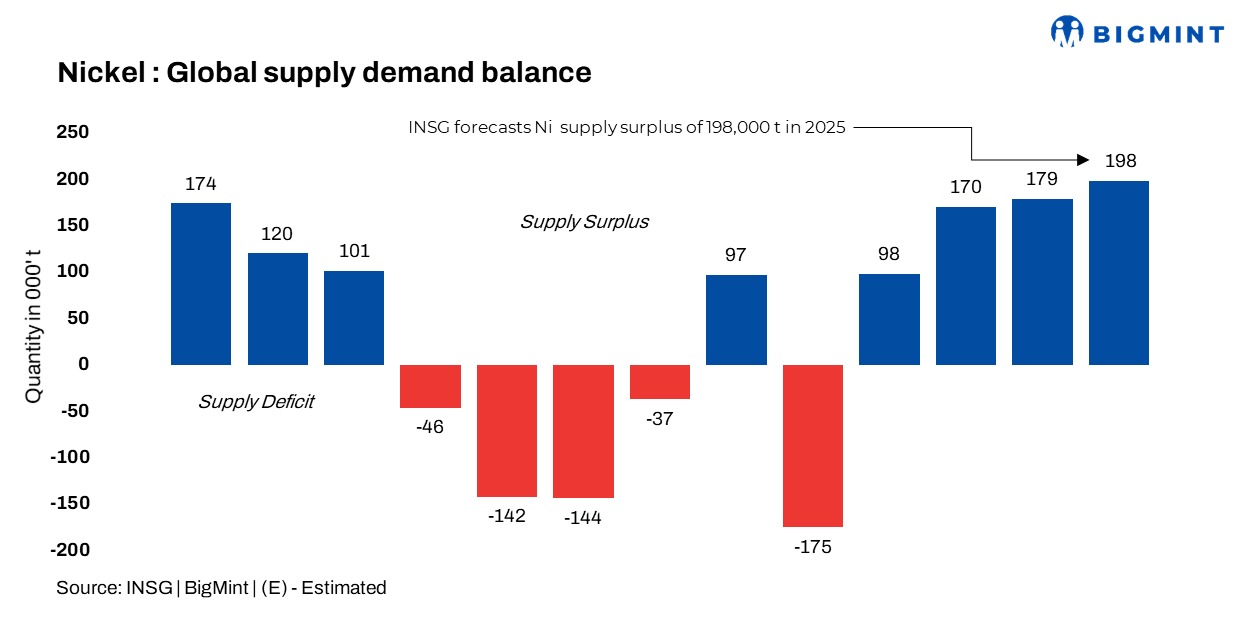

The International Nickel Study Group (INSG) convened on 22-23 April 2025, with participation from governments, industry stakeholders, and global organisations to review key nickel market developments.

At the platform, INSG revealed its forecast for global primary nickel production in 2025 at 3.735 million tonnes (mnt) and usage at 3.537 mnt, resulting in a projected surplus of 198,000 tonnes (t), following surpluses of 170,000 t in 2023 and 179,000 t in 2024.

Amid shifting global trade policies, market uncertainty has risen across the raw materials sector. In Indonesia, delays in mining permit approvals (RKABs) have tightened nickel ore supply, while the full impact of newly introduced royalties remains under assessment. Nevertheless, the country is expected to boost production of nickel pig iron (NPI), mixed hydroxide precipitate (MHP), matte, cathode, and sulphate in 2025.

China is also projected to increase primary nickel output, led by growth in cathode and sulphate production, although its NPI production is expected to decline. Globally, several producers are scaling back or suspending operations due to profitability concerns.

While stainless steel demand is set to grow, the expansion of nickel use in batteries has been slower than anticipated, driven by the rising adoption of lithium iron phosphate (LFP) batteries and plug-in hybrids. However, new precursor cathode active material (pCAM) projects globally may support future demand.

Leave a Reply