- Indonesian exports surge on regional demand

- India’s imports dip, HBA trends signal shifting preferences

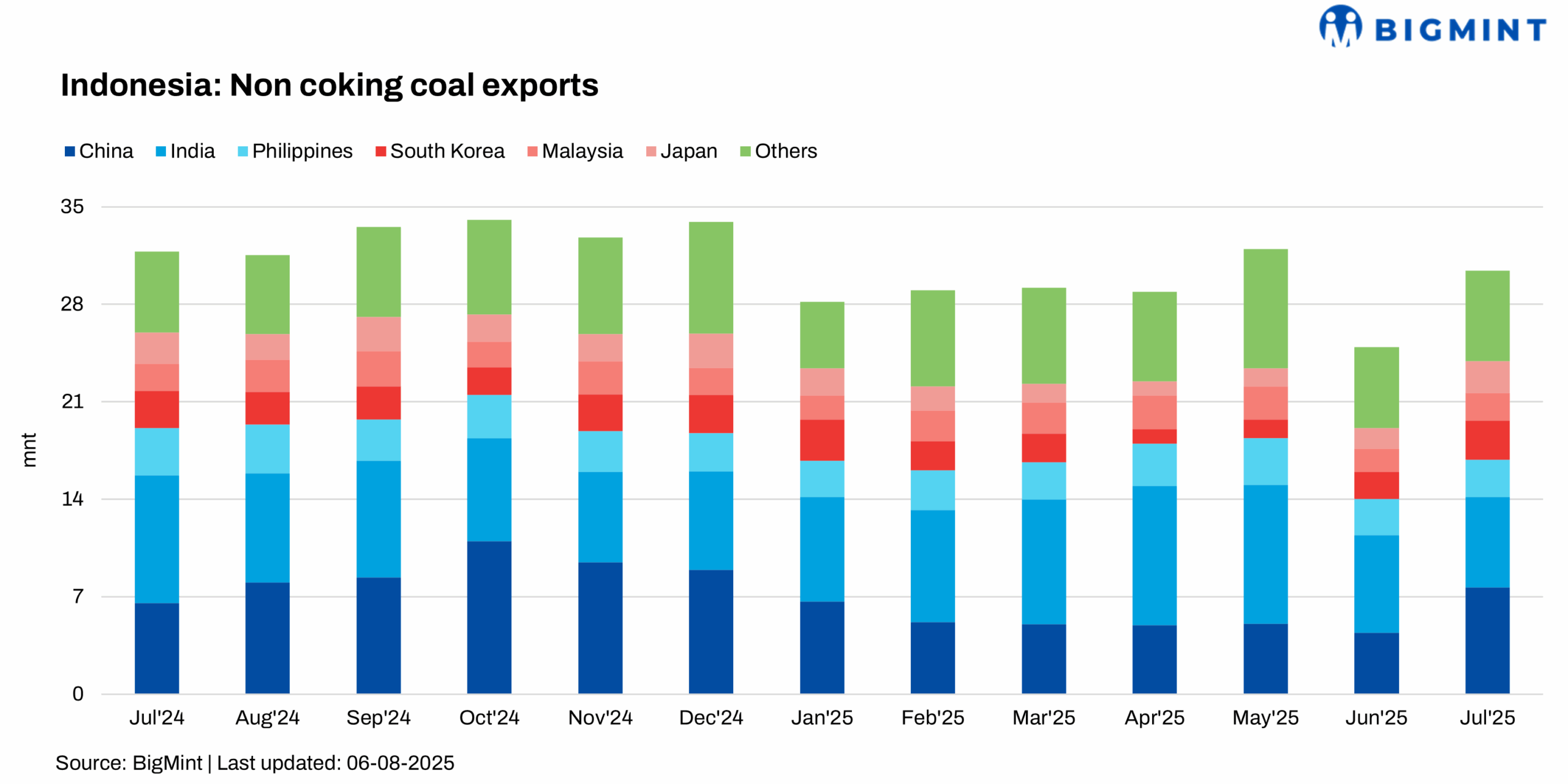

Indonesia’s thermal coal exports witnessed a strong recovery in July 2025, registering a month-on-month (m-o-m) increase of 22% to 30.43 million tonnes (mnt), up from 24.93 mnt in Jun’25. However, on a year-on-year (y-o-y) basis, exports declined by 4% compared to July, reflecting the broader structural shifts in regional energy markets and ongoing policy transitions.

Surge in Asian demand supports export recovery

The robust monthly rise in Indonesian exports was primarily driven by renewed demand from major Asian importers, despite growing caution around coal use due to clean energy transitions in several countries.

China’s imports of Indonesian thermal coal surged significantly by 73% m-o-m to 7.66 mnt, largely driven by restocking requirements amid high summer power demand and favourable price differentials compared to alternate sources. Similarly, South Korea and Japan posted notable increases, with imports rising by 45% to 2.81 mnt and 52% to 2.27 mnt, respectively, indicating renewed procurement interest from Northeast Asia after a subdued second quarter.

Southeast Asian buyers also contributed to the upswing. The Philippines recorded a modest 2% growth in imports to 2.67 mnt, while Malaysia’s imports rose sharply by 18% to 1.98 mnt, likely due to increased coal-based power generation needs and competitive Indonesian supply.

However, India, traditionally one of Indonesia’s largest thermal coal markets, reported a 7% m-o-m decline in imports to 6.51 mnt. The reduction stemmed from improved domestic coal availability and elevated stock levels at power plants, which reduced import dependence during the month.

Kalimantan drives export growth

Export growth was strongly supported by increased shipments from Indonesia’s major coal-producing regions, particularly Kalimantan. East Kalimantan, the largest contributor, saw exports rise 32% m-o-m to 15.43 mnt, reflecting smoother operational performance and port handling.

South Kalimantan followed with a 23% increase to 9.7 mnt, and North Kalimantan posted a 16% rise to 1.2 mnt, signaling recovery in regional production and logistics.

Sumatra diverged from the overall export trend, recording a 5% decline to 4.1 mnt, likely impacted by the recent collapse of the Muara Lawai Bridge in South Sumatra. Palembang has banned coal trucks from the Muara Lawai bridge after its partial collapse on 29 Jun’25. Also, the overloading-induced incident has disrupted coal transport from major miners.

Port-level activity reflects upbeat momentum

Port-level performance aligned with the broader uptick in export volumes. Taboneo Port led with a 22% rise to 6.06 mnt, followed closely by Samarinda at 4.56 mnt, up 23% m-o-m. Bunati Port recorded a strong 41% increase to 3.4 mnt, while Muara Pantai stood out with the sharpest gain of 224% to 2.43 mnt, likely due to resumption of operations or clearing of previous backlogs.

In contrast, Balikpapan port registered a 2% decline in throughput to 2.1 mnt, making it the only major facility to report a drop, potentially due to vessel congestion or scheduling disruptions.

Benchmark coal prices reflect mixed sentiment

Indonesia’s benchmark coal price index (Harga Batubara Acuan or HBA), released for mid-June 2025, highlighted varying trends across coal grades. FOB prices for high-calorific value (6,322 kcal/kg) coal fell by $2.36/t to $98.61/t, reflecting subdued interest in premium-grade coal amid cost-conscious procurement strategies.

Similarly, mid-CV (5,300 kcal/kg) coal prices declined by $1.95/t to $77.59/t, driven by easing international prices and oversupply concerns. On the other hand, lower-grade coal segments recorded marginal gains, with 4,100 kcal/kg coal prices rising by $0.17/t to $50.25/t and 3,400 kcal/kg coal increasing by $0.67/t to $36.14/t.

Outlook

Indonesia’s coal exports may stay strong in the short term on high power demand and competitive pricing, but face medium-term risks from green policies, renewables growth, and weather-related disruptions. Demand may tilt toward low-CV coals amid widening price spreads.

Leave a Reply