- Selective Asian buying weighed on exports

- Competitive low-grade coal sustained demand

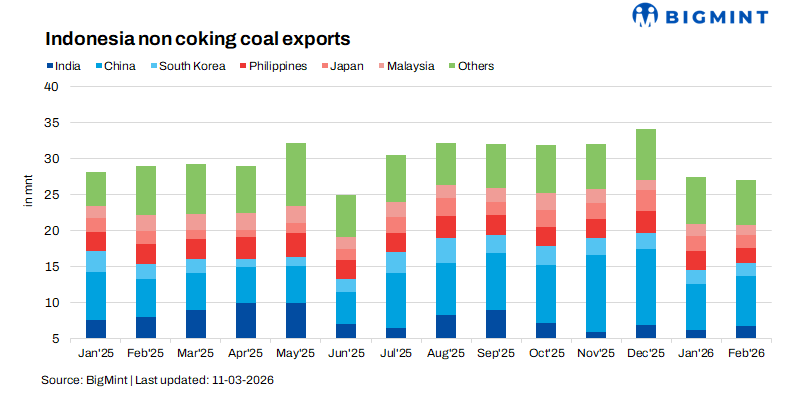

Indonesia’s non-coking coal exports recorded a marginal decline in February, slipping 1.8% month-on-month (m-o-m) to 26.95 million tonnes (mnt) from 27.45 mnt in January. Volumes have hit eight month’s low, as per data maintained with BigMint. The modest drop occurred despite relatively stable demand from several Asian markets and improved port activity following logistical disruptions earlier in the year.

On a year-on-year (y-o-y) basis, however, shipments were 7.1% lower, indicating a gradual moderation in global coal consumption. The decline reflects softer industrial activity in some importing economies, increasing adoption of renewable energy, and more cautious procurement strategies among utilities seeking to optimise fuel costs.

Global demand softens as energy transition gains momentum

February’s export performance highlights a moderation in global coal appetite, particularly across key Asian markets where utilities and industrial users have become increasingly cost-sensitive. Several importing countries have been adjusting procurement strategies amid comfortable inventory levels, improved domestic supply in some markets, and a gradual shift toward diversified energy sources.

Additionally, policy-driven decarbonisation efforts and greater renewable penetration are beginning to influence long-term coal consumption trends. In response, Indonesian miners have adopted a more cautious production approach, balancing output levels and pricing strategies to maintain competitiveness in a market characterised by fluctuating demand.

At the same time, short-term energy market volatility continues to influence coal sentiment. Financial coal benchmarks such as the Newcastle (NEWC) and API2 indices rallied sharply in early March before correcting, reflecting shifting expectations around gas supply disruptions and coal-fired power competitiveness in Europe. While these movements were driven largely by financial markets, they have contributed to cautious physical buying across Asia.

Asia’s import landscape shows diverging trends

Import patterns across major Asian buyers remained mixed and region-specific during February.

Exports to India declined 10.7% m-o-m to 6.82 mnt, primarily due to adequate domestic coal stockpiles and subdued industrial consumption. Many power utilities relied on existing inventories rather than increasing seaborne purchases.

India’s cautious buying behaviour has also been influenced by strong domestic coal supply. Coal India Ltd (CIL) has been ramping up output to meet its FY’26 production and dispatch targets, with pithead inventories expected to reach roughly 140-150 mnt by the end of March, compared with about 107 mnt a year earlier, reducing the immediate need for imported coal.

In contrast, exports to China rose 7.2% to 6.83 mnt, supported by stable electricity demand and inventory replenishment ahead of seasonal consumption requirements.

However, China’s domestic coal market remains relatively well supplied, which has limited stronger growth in seaborne imports despite international price volatility.

Elsewhere in Southeast Asia, shipments to Malaysia dropped 20.9% to 1.29 mnt, reflecting cautious buying behaviour amid competitive Indonesian offers and evolving industrial demand. In Northeast Asia, Japan’s imports fell 7.3% m-o-m to 1.9 mnt, largely due to seasonal stock adjustments and the gradual restart of nuclear power units.

Similarly, exports to South Korea declined 11.2% to 1.83 mnt, despite relatively stable electricity demand. The Philippines recorded a 21.9% decrease to 2.03 mnt, suggesting a temporary slowdown following earlier fluctuations in procurement.

Overall, coal purchasing across Asia remained highly price-sensitive, with buyers carefully balancing inventory levels, domestic supply, and evolving energy policies.

Regional supply trends reflect operational and demand variations

Coal shipment trends across Indonesia’s mining regions remained uneven, shaped by logistical conditions and varying demand for different coal grades.

East Kalimantan, Indonesia’s largest coal-producing region, saw exports fall 6.6% m-o-m to 12.51 mnt, largely due to temporary port congestion and limited vessel availability. South Kalimantan also experienced a modest decline of 1.2% to 9.88 mnt, reflecting softer buying interest from key import markets.

In contrast, North Kalimantan recorded a sharp 45.1% increase to 1.19 mnt, although the growth was partly constrained by weaker demand for premium-grade coal.

Meanwhile, Sumatra bucked the broader trend, with exports rising 4.6% to 3.38 mnt, supported by stronger demand for low-calorific-value coal from Southeast Asian buyers seeking more cost-effective fuel sources. This underscores the continued relevance of lower-grade coal in price-sensitive emerging power markets.

Lower-calorific coal from Indonesia continues to remain competitive in many Asian markets. For example, Indonesian 4,200 GAR coal has recently been assessed around $58/t FOB, remaining among the most economical seaborne fuels for power generation compared with higher-grade Australian or South African material.

Port operations show mixed performance

Shipment activity across Indonesia’s key export terminals displayed contrasting operational trends. Taboneo Port reported a 17.5% decline in shipments to 4.9 mnt, mainly due to logistical disruptions and vessel scheduling constraints. Balikpapan Port recorded a steeper 26.5% drop to 2 mnt, reflecting maintenance activities and shipment delays.

Meanwhile, Muara Pantai Port registered a marginal 1.7% decline to 1.77 mnt, while Samarinda Port saw shipments increase 4.5% to 3.5 mnt, benefiting from improved loading efficiency and smoother logistics.

The strongest performance came from Bunati Port, where shipments surged 35.8% to 3.68 mnt, supported by operational improvements and stronger handling of lower-grade coal cargoes.

Indonesian benchmark coal prices ease

Indonesia’s thermal coal benchmark prices (HBA) for the second half of Feb’26 softened moderately as export demand showed signs of stabilisation after earlier strength.

The 6,322 kcal/kg GAR benchmark declined 3% to $102.9/t, reflecting reduced buying interest in higher-calorific coal grades. Similarly, the 5,300 kcal/kg GAR (HBA-I) index fell 3% to $71.74/t, suggesting near-term demand saturation in some importing markets.

Lower-grade coal benchmarks registered steeper declines. The 4,100 kcal/kg GAR (HBA-II) index eased 1.8% to $47.3/t, while the 3,400 kcal/kg GAR (HBA-III) benchmark dropped 6% to $33.9/t, as buyers remained cautious and focused on securing competitively priced cargoes.

Overall, the price adjustment represents a short-term market recalibration following earlier price firmness, rather than a structural decline in demand.

Outlook

Indonesia’s coal exports are expected to inch down further, supported by steady Asian demand, though buying may stay selective due to ample inventories. Recent vessel-tracking data also indicates that Indonesian thermal coal shipments have been running below normal levels in early March, averaging roughly 0.79 mnt per day over the past week, compared with a longer-term average of about 1.3-1.35 mnt per day since 2024. This suggests export volumes may remain under pressure in the near term. Competitive low-CV coal is likely to sustain demand in emerging Asian markets.

Market participants are also closely watching developments in Indonesian production approvals, as only a limited number of miners have reportedly received confirmed RKAB quotas so far. Until greater clarity emerges, exporters and buyers may continue to adopt cautious positioning, potentially keeping Indonesian export volumes and seaborne trade flows volatile in the near term.

Leave a Reply