- Exports under pressure amid cautious Asian demand

- Stronger preference for lower-CV coal due to cost advantage

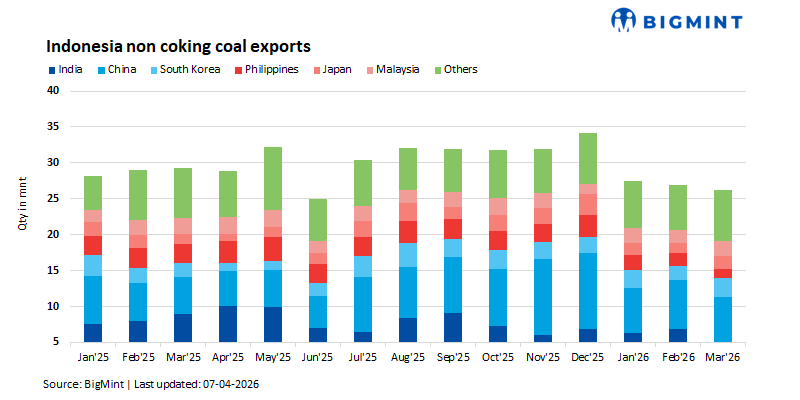

Indonesia’s non-coking coal exports recorded a marginal decline in Mar’26, slipping 2.6% m-o-m to 26.26 million tonnes (mnt) from 26.95 mnt in February, marking relatively subdued shipment levels, as per BigMint data. The dip came despite stable demand across key Asian markets and improved port activity.

On a y-o-y basis, exports were down 10%, indicating continued moderation in global coal demand amid softer industrial activity and increasing energy transition trends.

On a quarter-on-quarter basis, Indonesia’s non-coking coal exports declined 6.6% to 80.66 mnt in Q1 2026 from 86.37 mnt in Q1 2025, reflecting subdued regional demand and cautious buying trends.

Mixed demand trends in Asia

Indonesia’s coal shipments to major Asian destinations showed divergent trends in March, reflecting varying power demand patterns and procurement strategies across the region. Exports to South Korea declined sharply by 36% m-o-m to 1.18 mnt, likely due to comfortable inventories and reduced spot buying.

In contrast, shipments to Malaysia increased by 48% m-o-m to 1.91 mnt, while exports to the Philippines rose 29% to 2.62 mnt, supported by steady power generation demand and replenishment of utility stocks. Similarly, exports to India increased by 6.5% m-o-m to 7.26 mnt, driven by ongoing demand from the power and sponge iron sectors.

However, exports to China recorded a sharp decline of 39.8% m-o-m to 4.11 mnt, reflecting stronger domestic coal supply and cautious import procurement. Meanwhile, shipments to Japan increased moderately by 7.4% to 2.04 mnt, supported by stable utility demand and long-term supply contracts.

Regional supply trends reflect operational and demand variations

Coal shipment patterns across Indonesia remained uneven in March, reflecting both demand variations and logistical factors. East Kalimantan, the largest producing region, saw exports decline 7.2% m-o-m to 11.61 mnt amid softer buying and operational constraints, while South Kalimantan fell 2% to 9.68 mnt.

North Kalimantan also dropped 10.9% to 1.06 mnt, indicating weaker demand for higher-grade coal. In contrast, Sumatra recorded a strong 15.7% rise to 3.91 mnt, supported by steady demand for low-calorific coal from price-sensitive Southeast Asian markets.

Port operations show mixed performance

Port operations in March displayed a mixed trend across key Indonesian loading hubs. Shipments from Taboneo increased by 23.9% m-o-m to 6.07 mnt, supported by improved barge availability and stronger cargo movement. In contrast, loadings from Samarinda declined by 9.4% to 3.17 mnt, likely due to logistical constraints and uneven mine dispatches.

Bunati recorded a sharp drop of 38.3% to 2.27 mnt, primarily reflecting lower production and shipment scheduling. Meanwhile, volumes from Muara Pantai and Balikpapan decreased by 6.2% and 10.5% to 1.66 mnt and 1.79 mnt, respectively, amid softer demand and intermittent operational adjustments.

Shifting demand patterns affect coal benchmarks

Indonesia’s coal benchmark prices (HBA) released by the Ministry of Energy and Mineral Resources (ESDM) for the first half of April 2026 reflected mixed movements across different calorific value (CV) segments, highlighting evolving demand dynamics in the seaborne market.

Higher-calorific value coal registered a mild correction amid cautious procurement by buyers and relatively comfortable supply levels. In contrast, lower-CV grades continued to strengthen, supported by firmer demand from cost-conscious Asian utilities seeking more economical fuel options.

The trend indicates a gradual shift in purchasing preferences, with several importers favouring lower-CV Indonesian coal due to its competitive pricing and suitability for blending, while higher-CV material faced relatively weaker buying interest.

Outlook

Indonesia’s non-coking coal exports are expected to remain relatively stable in the near term, though growth may stay limited amid cautious buying and ample inventories with key Asian buyers. Demand is likely to remain stronger for lower-CV coal, supported by cost-conscious utilities in Southeast Asia. Meanwhile, higher-CV coal may continue to face pressure unless industrial activity and power demand improve across major importing countries.

Leave a Reply