- HBA coal prices rise across all CV segments amid firm demand

- Affordable lower-CV coal continues to attract strong buying interest

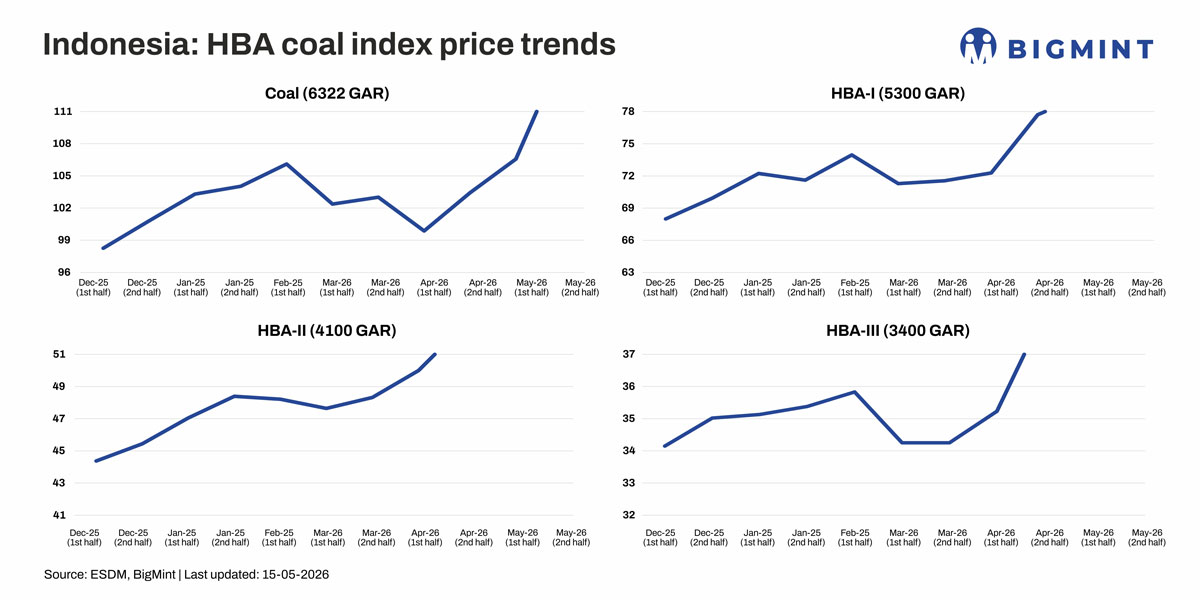

Indonesia’s Harga Batubara Acuan (HBA) thermal coal benchmarks registered broad-based gains across all calorific value (CV) segments for the second half of May 2026, reflecting tightening spot availability, sustained regional demand, and improving procurement activity from utilities and industrial consumers across Asia.

The upward movement highlights strengthening sentiment in the seaborne thermal coal market, particularly as buyers continue to secure cargoes ahead of peak summer power consumption and amid persistent fuel affordability concerns in emerging economies.

High-CV coal segment strengthens

The benchmark HBA price for 6,322 kcal/kg GAR coal increased sharply by nearly 9% to $116.32/t in H2 May’26 from the first half of the month, reaching its highest level in almost one year.

The strong recovery in the high-CV segment was primarily driven by renewed procurement from major power utilities across Asia, particularly in countries facing rising electricity demand during the summer season. Utilities showed increased preference for high-energy coal grades to improve combustion efficiency and optimise generation costs amid elevated power loads.

Mid-CV coal gains support from cost-conscious buyers

The HBA-I benchmark for 5,300 kcal/kg GAR coal rose by 1% to $80.34/t, returning to levels last seen in early May 2025.

The increase was largely supported by resilient buying interest from price-sensitive importing nations such as India and Vietnam, where mid-CV coal continues to provide an effective balance between calorific efficiency and procurement affordability.

Utilities and industrial consumers in these regions increasingly preferred mid-grade coal due to its comparatively lower landed cost versus premium grades, particularly at a time when energy buyers remain focused on controlling generation and production expenses.

Lower-CV coal segments outperform on affordability-driven demand

The lower-calorific coal categories recorded comparatively stronger gains during the period, reflecting sustained procurement from smaller utilities, cement manufacturers, and industrial consumers seeking economical fuel alternatives.

HBA-II (4,100 kcal/kg GAR) reaches record high: The HBA-II benchmark for 4,100 kcal/kg GAR coal surged by 3.5% to $57.61/t, marking the highest level since the benchmark was introduced.

The sharp increase was supported by strong buying interest from South and Southeast Asian consumers, where lower-CV coal remains an attractive option due to its competitive pricing and suitability for blended fuel consumption.

HBA-III (3,400 kcal/kg GAR) hits fresh all-time high: Meanwhile, the HBA-III benchmark for 3,400 kcal/kg GAR coal increased by 1.5% to $39.35/t, reaching a new all-time high.

Demand for ultra-low CV coal remained firm from highly price-sensitive markets that continue shifting toward lower-cost fuel sources amid broader economic and energy cost pressures. Industrial users and smaller power producers increasingly opted for cheaper coal alternatives to manage operational expenditures, thereby sustaining strong consumption levels in this category.

The market also benefited from stable downstream industrial demand and improving trade flows within the regional seaborne market.

Key market drivers behind the HBA rally

Several factors collectively supported the upward movement across Indonesia’s thermal coal benchmarks:

- Seasonal summer demand growth across Asia boosted electricity generation requirements and coal procurement activity.

- Limited spot cargo availability tightened supply conditions, particularly for prompt-loading shipments.

- Strong demand from emerging Asian and other Southeast Asian nations continued to support seaborne trade flows.

- Affordability-driven fuel switching encouraged buyers to increasingly procure lower-CV coal grades.

- Stable industrial activity across cement, metals, and manufacturing sectors sustained consumption of mid- and lower-grade coal.

- Improved market sentiment and firmer seller expectations contributed to higher offer levels across the Indonesian coal market.

Market outlook

Indonesia’s thermal coal market is expected to remain firm, supported by seasonal power demand, utility restocking, and tight spot supply. High-CV coal is likely to stay elevated amid strong utility procurement, while mid- and lower-CV grades may continue receiving support from cost-sensitive Asian buyers. However, cautious imports, softer freight rates, and rising renewable energy generation could limit further price gains.

Leave a Reply