- Indonesian supply risks underpin price floor despite weak Asian demand

- Wide bid-offer gaps reflect policy uncertainty and firm producer stance

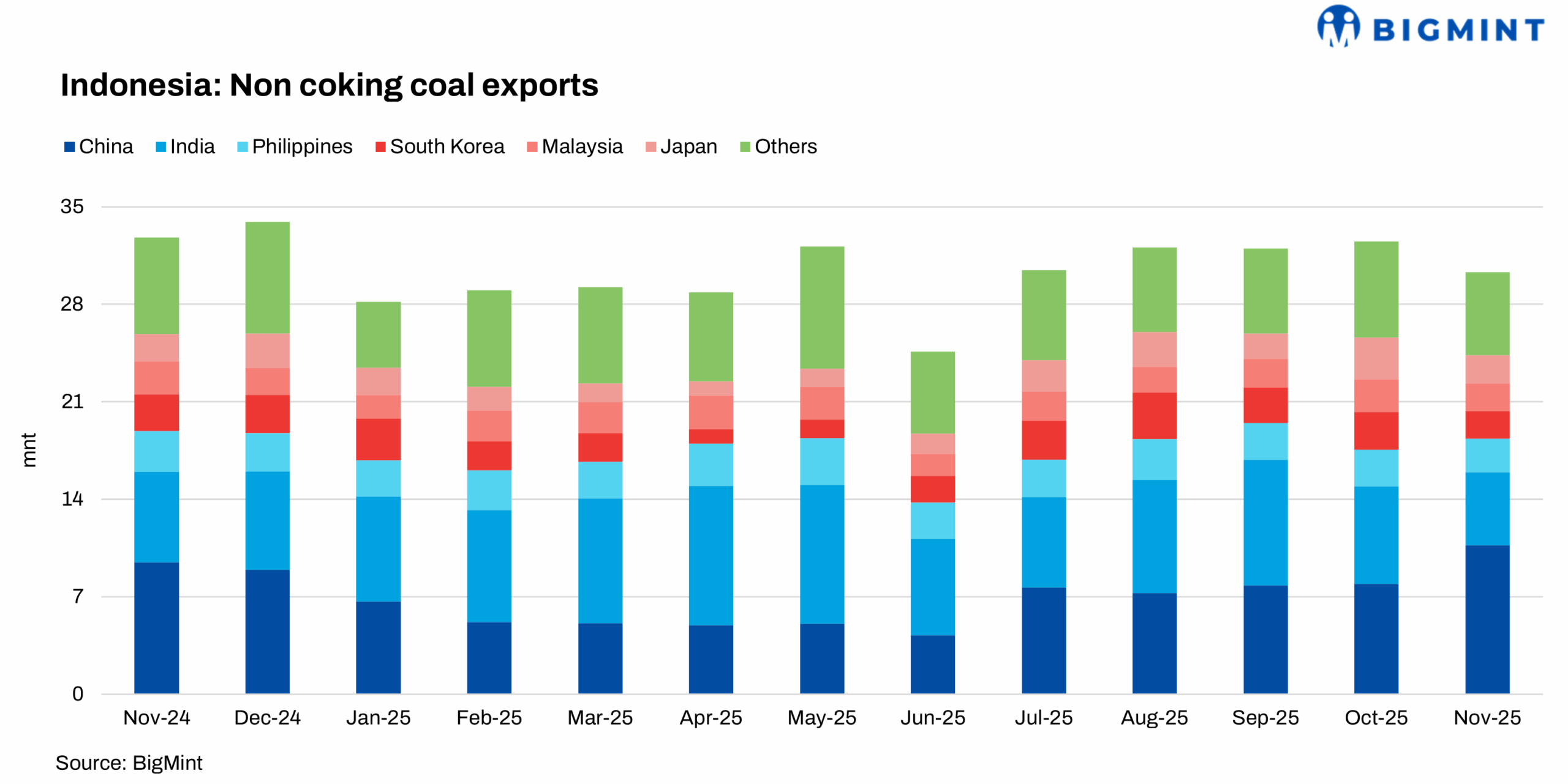

Indonesia, the world’s largest exporter of low- and mid-CV coal, has entered a period of unusual pricing firmness — even as buyers across China and India push aggressively for discounts.

The reason? A perfect storm of supply-side uncertainty heading into 2026.

Unapproved 2026 production quotas

Indonesia’s government has not yet finalised next year’s production quota. This vacuum — highly unusual for December — has made miners reluctant to sell aggressively into falling markets.

Some fear:

- Production caps

- Export curbs

- A potential export tax on thermal coal

- New domestic supply obligations

Wet-weather disruptions

The January-March monsoon threatens:

- Reduced mine productivity

- Haul-road damage

- Port congestion

- Lower-than-expected output

Producers know this well: January-March is historically their costliest and least predictable quarter.

Market response

Chinese buyers have retreated, leaving offers untouched:

- 3,800 GAR offers remain at $40-41/t FOB, with bids still stuck in the high $30s

- Ultra-low-rank bids at $38/t FOB find no counterparty

- Indonesian 4200 GAR remains India’s most competitive fuel, delivered at INR 1,350-1,390/Gcal

Impact on Asia

The bid-offer gap is now a core sign of stress:

- Soft demand

- Firm supply psychology

- Policy-dependent forward pricing

Indonesia has effectively set a floor for regional low-CV prices — even as global coal enters a deeply bearish winter.

Leave a Reply