- Policy shifts, heavy rains, Ramadan slowdown tighten supply

- Widening bid-offer gaps signal buyers’ resistance to higher prices

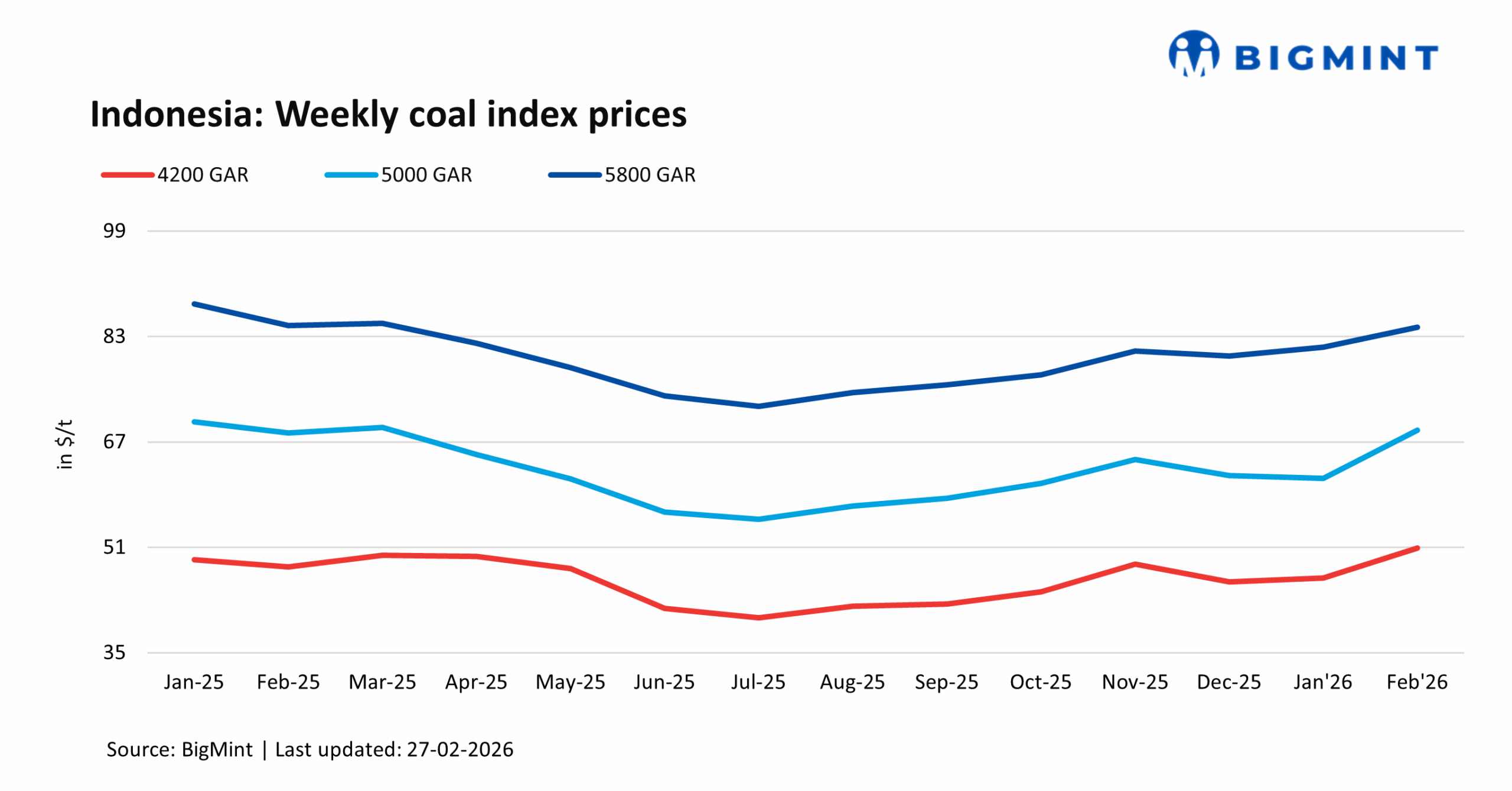

Indonesian thermal coal prices rose strongly in February, but gains were uneven across grades. Low- and mid-grade coal saw the biggest increases. Higher grades were more stable and, in one case, slightly weaker.

Details of price movements

The 4,200 GAR grade was the strongest performer. Prices climbed to $53.65/tonne (t) by 27 February, up $2.50/t in one week. Prices were at around $46.57/t in January.

The 3,800 GAR grade rose to $45.47/t, up $1.76/t on the week. The 3,400 GAR grade increased more slowly, reaching $34.80/t.

Forward prices also moved higher. March and April 2026 contracts for 4,200 GAR were both around $53-54/t. Even contracts for 2027 increased, showing that traders expect supply tightness to continue.

In contrast, the 5,000 GAR grade slipped slightly to $70.31/t, even though some offers were heard at $72-73/t. Buyers were less willing to accept higher prices at this level. The 5,800 and 6,300 GAR grades rose only modestly.

In the physical market, sellers asked $57.50-62.00/t for 4,200 GAR coal for March loading, while buyers bid $55.50-57/t. For 5,000 GAR coal, offers were near $72-73/t, with bids closer to $71/t. The gap between bids and offers widened as prices rose, showing buyer caution.

Freight trends also shifted. Prices of larger Panamax vessels rose, but not as much as prices for smaller geared vessels. The price difference between them narrowed. This suggests buyers preferred smaller ships, possibly for more flexible port access or tighter stock control.

Why prices rose

Supply tightness in Indonesia: The main reason for the rally was supply pressure. Many miners faced delays in getting approval for their annual production plans. Some received lower production quotas than expected. Others were still waiting and could not sell forward cargoes.

Heavy rains in Kalimantan disrupted mining and port loading. In South Sumatra, road transport limits slowed coal deliveries. With Ramadan approaching, mining activity also slowed. These factors reduced the supply of spot cargoes, especially in the 3,800-4,200 GAR range, which is Indonesia’s core export segment.

Strong Chinese buying: After the Lunar New Year, Chinese buyers returned to the market. Tender activity increased, and delivered prices into China rose sharply during the month. Low- and mid-grade coal was in strong demand because it blends well with domestic coal and offers good value. This supported Indonesian prices.

Cautious Indian demand: Indian buyers were more price-sensitive, especially for 4,600-5,000 GAR coal used in sponge iron production. As prices rose, resistance increased. This explains why the 5,000 GAR grade did not rise as strongly as lower grades.

Outlook

Tight market, but buyers are careful: Prices enter March with strong momentum. Forward prices suggest that traders expect supply to remain tight in the near term. However, the widening gap between bids and offers shows that buyers are becoming cautious at higher price levels. Chinese utilities hold comfortable stock levels at ports, giving them time to buy selectively. Indian buyers are also resisting peak prices.

Supply likely tight until April: Production approvals in Indonesia are still being finalised. Until this is resolved, supply is likely to stay tight. Even after approvals, it will take time for output to increase. Ramadan will also slow mining and logistics through mid-March. This means meaningful supply relief is unlikely before April.

Middle East conflict and energy prices: The conflict in the Middle East adds another layer of uncertainty. Tensions in the region have pushed up oil prices and increased volatility across energy markets.

Higher oil prices can raise bunker fuel costs for ships, which increases freight rates. That pushes up the delivered price of coal into Asia. If shipping costs rise further, buyers may slow purchases or seek closer supply sources.

Rising oil and gas prices can also make coal more attractive for power generation in some countries. In that case, coal demand could strengthen. On the other hand, if energy prices become too high and hurt economic growth, overall fuel demand could weaken.

In short, events in the Middle East can affect coal through freight costs, competing fuel prices, and general market sentiment.

The bigger picture

February showed how quickly prices can rise when supply is tight and demand is steady. Low- and mid-grade coal benefited the most.

The key question now is whether this is a short-term spike or the start of a longer period of tight supply. If production limits continue, prices may stay firm. If output normalises, some correction is possible.

For now, the market remains tight, but buyers are clearly more cautious at higher price levels.

Leave a Reply