- Supply tightness supports prices

- High-/low-CV firm; mid-CV weak

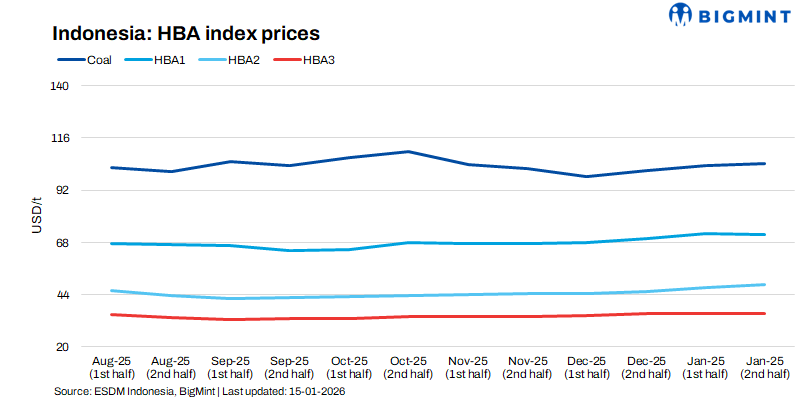

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) has revised its thermal coal benchmark prices (HBA) for the second half of January 2026, indicating a broadly firm price environment across most calorific value (CV) segments.

The revision reflects improving regional demand – particularly from key Asian buyers – alongside more disciplined supply behaviour by Indonesian miners, who remain cautious in ramping up output amid policy uncertainty and domestic priorities.

Benchmark movements across CV segments

Price trends during the period were mixed across CV categories. High-calorific value coal recorded a clear uptick, with the 6,322 kcal/kg GAR benchmark rising by 0.7% from the first half of January to USD 104.03/t, supported by steady demand from utilities seeking higher efficiency fuels.

In contrast, mid-calorific value coal softened marginally, as the 5,300 kcal/kg GAR (HBA-I) index declined by 0.87% to USD 71.61/t, reflecting near-term demand saturation and inventory comfort in certain importing markets. Lower-grade coal outperformed, with HBA-II (4,100 kcal/kg GAR) climbing sharply by 2.8% to USD 48.39/t, driven by cost-sensitive buyers and stronger pull from price-elastic markets in South and Southeast Asia.

Production curtailment signals structural tightness

On the supply side, Indonesia has signalled a significant shift in its coal production strategy. Energy and Mineral Resources Minister Bahlil Lahadalia stated that coal output is planned to be reduced to around 600 million tonnes (mnt) in 2026. This compares with an estimated 790 mnt in 2025 – above the official target of 735 mnt but below the record 836 mnt produced in 2024. The planned cut underscores the government’s intent to rein in oversupply, improve price stability, and align production more closely with long-term energy transition objectives.

Domestic market obligation remains paramount

Domestic demand will continue to take precedence over exports. The ESDM reiterated that the Domestic Market Obligation (DMO) allocation will be adjusted as required to ensure local demand is fully met before permitting overseas shipments. This policy stance is likely to constrain export availability during periods of strong domestic consumption, reinforcing Indonesia’s role as a more supply-managed exporter rather than a volume-driven supplier.

Market outlook

Indonesia’s thermal coal prices are expected to stay supported by production cuts, strict DMO enforcement, and steady Asian demand, with strength in high-CV and lower-grade coal, while mid-CV may remain under pressure.

Leave a Reply