- H1 exports down 13% on weak Asian demand

- India’s imports plunge 31% m-o-m in June

Indonesia’s non-coking coal exports witnessed a sharp downturn in June 2025, falling by 23.1% m-o-m to 24.62 million tonnes (mnt), compared to 32.04 mnt in May 2025.

On a y-o-y basis, exports were also significantly lower, declining by 24% from June 2024. This steep drop was primarily driven by weak buying interest from key Asian markets and a growing emphasis on domestic coal consumption within Indonesia.

Subdued demand from key Asian buyers

The decline in exports was largely shaped by reduced demand from Indonesia’s major non-coking coal customers in Asia. India, the largest importer of Indonesian coal, saw a 30.5% m-o-m drop in imports to 6.91 mnt in June.

Similarly, China’s imports fell by 15.7% to 4.25 mnt amid increased domestic coal production and tepid demand for Indonesian material. The Philippines also registered a 22% decline in imports to 2.61 mnt, while Malaysia’s imports dropped sharply by 34.7% to 1.59 mnt.

Contrasting this trend, South Korea and Japan offered some positive momentum. South Korea’s imports surged by 44.5% to 1.93 mnt, marking a strong return to the Indonesian market. Japan’s imports rose by 10% to 1.43 mnt, providing some degree of market support.

Exports decline in first-half

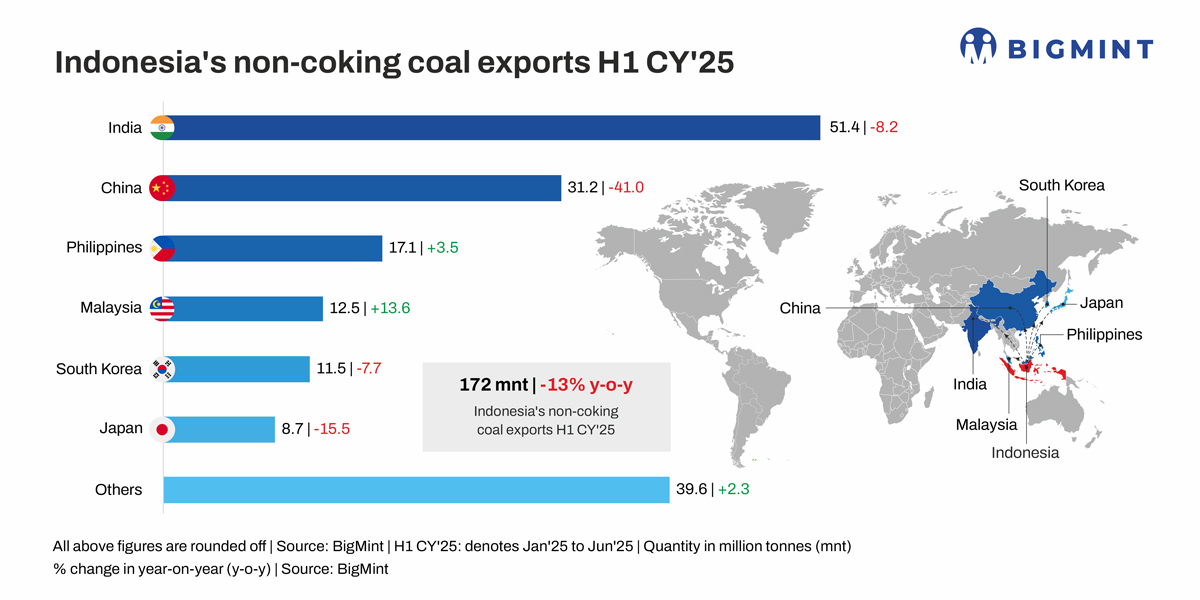

For the first half of calendar year 2025 (H1CY’25), Indonesia’s thermal coal exports totalled at 172 mnt, marking a 13.1% y-o-y decline from 198 mnt in H1CY’24. The most significant drop was in shipments to China, which fell by a steep 41% to 31.16 mnt due to rising domestic output and consumption.

Exports to India during the same period dropped by 8.3% to 51.4 mnt. This decrease was attributed to improved availability of domestic coal through auctions, aligning with India’s ongoing strategy to boost self-reliance in energy.

Japan also recorded a 15% decline in imports to 8.7 mnt. Overall, the downturn in H1 exports was largely the result of subdued global demand and increased domestic coal availability in Indonesia.

Regional export trends reflect overall decline

Coal-producing regions in Indonesia reported notable m-o-m reductions in export volumes in June. East Kalimantan remained the largest exporting region, though its shipments dropped by 25% to 11.52 mnt. South Kalimantan followed closely, with a 26.5% fall to 7.91 mnt. North Kalimantan experienced the sharpest decline of 43.5%, with exports falling to just 0.85 mnt.

Sumatra saw a marginal 0.05% drop in exports to 4.34 mnt, but faces potential short-term disruptions following the recent collapse of the Muara Lawai Bridge in South Sumatra. The incident, caused by overloading, has halted coal transport from key mining firms, prompting an official suspension and investigation.

Port activity slows in line with export trends

Major Indonesian coal ports mirrored the declining trend in exports. Taboneo Port recorded a 27.7% m-o-m fall in shipments to 4.97 mnt, while Muara Pantai saw the steepest reduction of 69.1%, down to 0.75 mnt. Exports from Balikpapan dropped by 17% to 2.14 mnt, and Samarinda handled 3.58 mnt, a 27.3% decrease.

Bunati Port also saw a modest decline, with exports falling by 3.3% to 2.42 mnt. Overall, port activity remained sluggish throughout the month, in line with falling international demand.

Coal prices under pressure amid mixed market signals

Indonesia’s benchmark thermal coal reference prices (Harga Batubara Acuan or HBA) for the second half of May 2025 reflected market softness across higher-grade coals. High-calorific value (CV) coal (6,322 kcal/kg) fell by 8.9% to $110.38/t compared to first half of May 2025, while mid-CV coal (5,300 kcal/kg) prices declined by 5.1% to $76.62/t.

In contrast, low-grade coal prices recorded marginal gains. Low-CV coal (4,100 kcal/kg) inched up by 0.3% to $50.58/t, and very low-CV coal (3,400 kcal/kg) rose by 2% to $35.42/t compared to the first half. These price movements underscore a shift in demand toward lower-grade, cost-effective fuels amid a broader market slowdown.

Outlook

Amid weak demand from key Asian markets, rising domestic coal supply, and logistical disruptions, Indonesia’s non coking coal export outlook remains subdued. Without a rebound in regional power demand or shifts in trade policies, further pressure on export volumes and prices is likely.

Leave a Reply