- Indonesia’s coal exports stay steady on mixed Asian demand

- Shipments rise from East and North Kalimantan, decline from South Kalimantan, Sumatra

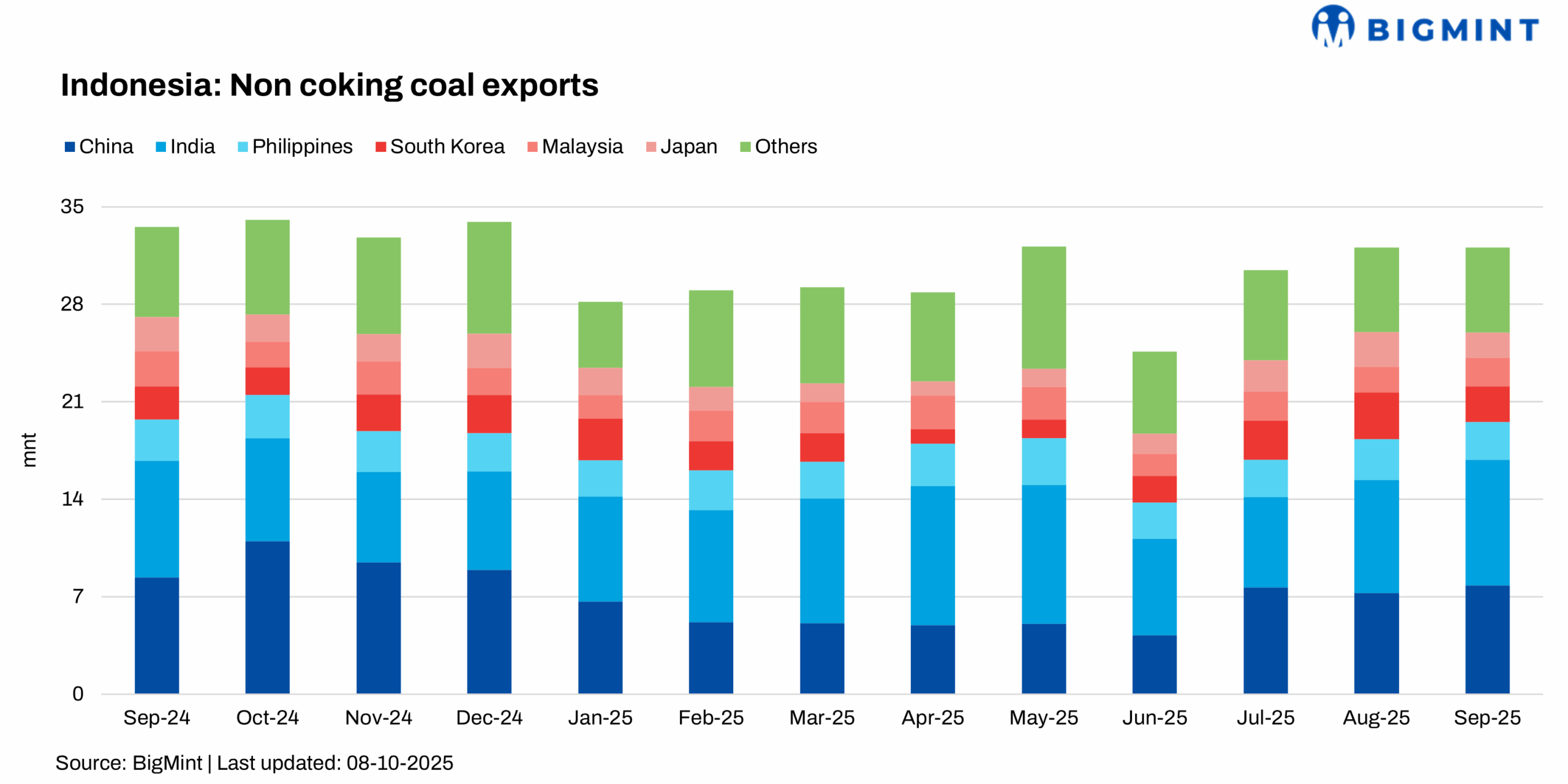

Indonesia’s non-coking coal exports remained largely stable in September 2025, recording a marginal 0.1% month-on-month (m-o-m) decline to 32.06 million tonnes (mnt) from 32.1 mnt in August. However, exports fell sharply by 4.38% year-on-year (y-o-y) compared to September 2024, signaling slightly weaker international demand.

Mixed trends in Asian demand

Asian buyers exhibited mixed import activity during the month. India, one of Indonesia’s top importers, increased purchases by 11% m-o-m to 9.03 mnt, while China’s imports rose 7.68% to 7.82 mnt, supported by steady power sector demand. Malaysia also saw an 11.85% rise in imports to 2.05 mnt, reflecting sustained industrial activity.

Conversely, several key markets reduced intake. Japan’s imports fell sharply by 28% m-o-m to 1.79 mnt, while South Korea recorded a 23.8% decline to 2.57 mnt. The Philippines also witnessed a 7.6% drop to 2.71 mnt, indicating weaker energy demand in parts of Southeast Asia.

Regional supply shows mixed momentum

Export performance across Indonesia’s mining hubs also varied. East Kalimantan, the country’s largest coal-producing region, increased shipments by 6.6% m-o-m to 16 mnt, supported by smoother port operations. North Kalimantan reported a strong 23.5% jump to 1.26 mnt, owing to better logistics.

On the other hand, South Kalimantan saw a 4.9% decline to 10.56 mnt, while Sumatra recorded a steeper 14.35% fall to 4.24 mnt, suggesting moderate supply-side softening.

Port-level activity reflects varied movement

Port-wise data indicated uneven performance. Taboneo Port saw shipments drop 13.5% m-o-m to 5.86 mnt, while Balikpapan reported a 2.6% dip to 2.71 mnt. In contrast, Bunati Port recorded a 7.4% increase to 4.44 mnt, and Samarinda rose 5% to 4.74 mnt. Muara Pantai posted the highest surge m-o-m, up 40.6% to 1.71 mnt.

Benchmark coal prices show mixed sentiment

Indonesia’s Harga Batubara Acuan (HBA) for mid-August 2025 showed diverging price trends. High-CV (6,322 kcal/kg) coal fell $1.53/t to $100.69/t, while Mid-CV (5,300 kcal/kg) eased $0.13/t to $67.2/t. Lower grades followed suit, with 4,100 kcal/kg coal down $2.04/t to $43.7/t, and 3,400 kcal/kg sliding $1.38/t to $33.48/t.

Outlook

Indonesia’s non-coking coal exports are expected to stay stable in the coming months, supported by firm Indian and Chinese demand. However, weaker buying from Japan and South Korea, coupled with volatile prices and logistical constraints, may limit any sharp export growth in the near term.

Leave a Reply