- High inventories, weaker industrial activity dampen demand

- China emerges as only Asian nation to lift Indonesian coal intake

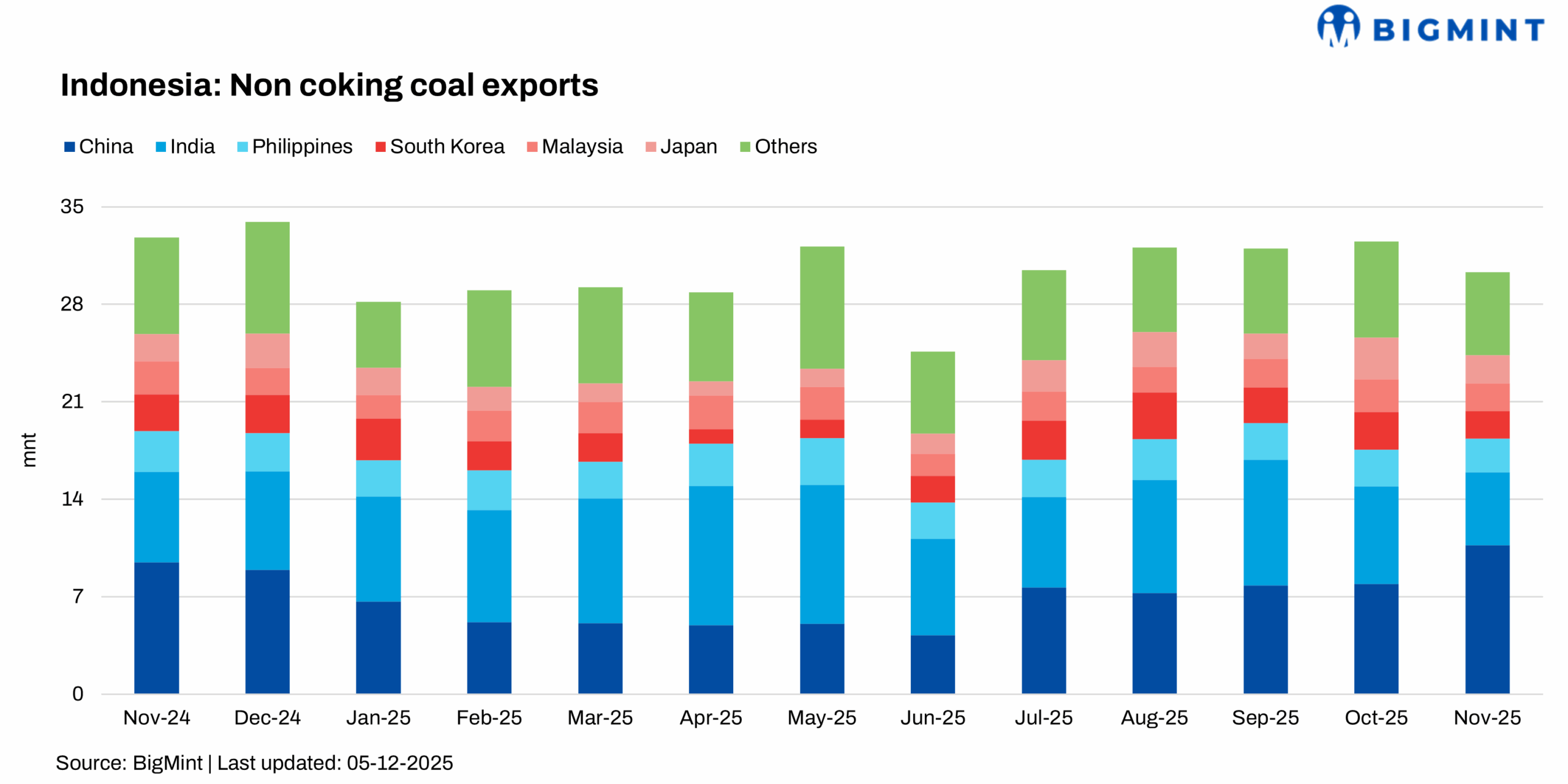

Indonesia’s non-coking coal exports declined in November 2025, signalling a gradual cooling in global consumption. Shipments fell 6.8% m-o-m to 30.29 million tonnes (mnt), from 32.51 mnt in October. On a y-o-y basis, exports slipped 7.6%, reflecting subdued demand across major Asian markets.

Asian imports lose momentum, except China

Most Asian importers reduced procurement amid high inventories, weaker industrial activity, and cautious restocking.

India, typically a key buyer, slashed imports by 25% m-o-m to 5.24 mnt as utilities leaned on domestic coal stocks. Southeast Asia followed a similar pattern — Malaysia cut intake by 15.2% to 1.99 mnt, while the Philippines recorded an 8.8% decline to 2.41 mnt.

Northeast Asian demand also softened. Japan’s imports plunged 33.6% to 1.99 mnt, and South Korea’s volumes dropped 26.2% to 2 mnt.

China, however, bucked the regional trend. Its imports surged 35.1% m-o-m to 10.69 mnt on the back of steady power consumption and strategic winter stocking.

Region-wise export performance remains mixed

Indonesia’s coal-producing regions showed contrasting output trends due to logistics and grade-specific demand.

East Kalimantan, the country’s largest producing zone, saw shipments fall 19% to 11.86 mnt amid limited vessel availability. Sumatra also posted a 13.7% decline to 4.38 mnt.

In contrast, North Kalimantan saw a sharp 33.9% jump to 1.36 mnt, while South Kalimantan recorded a 7.8% rise to 12.7 mnt.

Ports reflect uneven throughput

Port performance reinforced the uneven supply trends. Taboneo shipments dropped 16.8% to 5.96 mnt, while Samarinda fell 5.2% to 3.67 mnt and Muara Pantai plunged 17% to 2.35 mnt.

Meanwhile, Balikpapan posted a 10.3% rise to 2.02 mnt, and Bunati saw a 16.7% jump to 5.09 mnt.

Price trends show divergence across grades

Indonesia’s benchmark prices (HBA) for early December showed mixed movement. High-CV (6,322 GAR) fell 3.7% to $98.26/t amid muted spot buying. Mid-CV (5,300 GAR) gained 1% to $67.99/t on steady trade, while low-CV grades continued to edge higher, supported by cost-sensitive demand.

Outlook

Indonesia’s thermal coal market is likely to remain subdued in the near term as Asian buyers rely on inventories and mild weather caps power burn. However, prices are expected to remain stable, supported by the affordability of low-CV grades and steady Chinese demand. Logistics normalisation in Kalimantan could also help balance supply flows, keeping volatility contained.

Leave a Reply