- Tight supply and steady Asian demand support prices

- Higher exports and weaker Chinese demand may cap gains

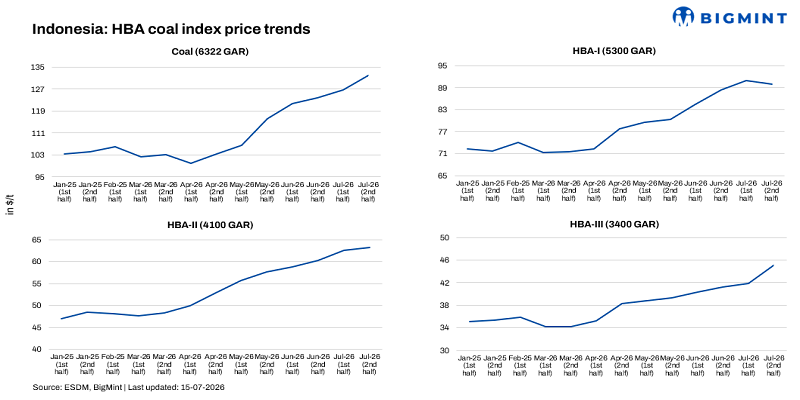

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) raised its Harga Batubara Acuan (HBA) thermal coal reference prices for most grades for the second half of July, with the benchmark 6,322 kcal/kg GAR grade rising by 4% to $131.85/t compared to the first half of the month, reflecting tightening spot supply, resilient buying interest from Asian utilities, and continued uncertainty surrounding Indonesia’s evolving export framework.

The sharp increase was primarily supported by limited export availability as several producers adopted a cautious sales strategy amid ongoing policy transitions and prioritisation of domestic coal obligations (DMO). At the same time, steady procurement from key importers, particularly China, India and other Southeast Asian nations, provided additional support to high-grade coal prices.

Mid-CV coal faces mild correction on balanced fundamentals

In contrast, the HBA-I (5,300 kcal/kg GAR) benchmark declined marginally by 1% to $89.9/t, recording its first decline since February 2026. The slight correction reflected relatively balanced market fundamentals, with adequate supply meeting stable demand. Buying interest from price-sensitive consumers remained moderate as several importers continued to rely on existing inventories while monitoring price movements. The absence of fresh procurement momentum and greater availability of mid-grade material also weighed modestly on prices.

Lower-CV coal extends uptrend on strong blending demand

Lower-calorific coal continued to outperform the broader market. The HBA-II (4,100 kcal/kg GAR) benchmark increased by nearly 1% to $63.25/t, while HBA-III (3,400 kcal/kg GAR) recorded a significant 8% increase to $45.08/t, with both benchmarks reaching record highs. The gains were driven by sustained demand from cost-conscious power utilities across emerging Asian markets, where lower-grade coal remains an attractive fuel for blending strategies to reduce overall generation costs. Despite their relatively lower energy content, these grades continue to benefit from their competitive pricing compared with higher-CV coal and alternative fuels.

Key market drivers

- Tight spot export availability as producers remain cautious amid evolving export regulations.

- Persistent uncertainty over Indonesia’s coal export governance, prompting sellers to limit spot offerings until policy implementation becomes clearer.

- Strong procurement by Asian utilities, particularly from China, India and Southeast Asia, driven by seasonal electricity demand.

- Higher demand for lower-CV coal due to fuel cost optimisation and blending requirements at thermal power plants.

- Domestic Market Obligation (DMO) prioritisation, which continues to restrict export availability for several producers.

- Production quota expansion under RKAB, Indonesia’s work plan and budget, improving medium-term supply visibility but remaining below last year’s actual production levels.

- Limited availability of premium high-CV cargoes, supporting prices despite higher approved production.

Indonesian coal market scenario

The Indonesian coal market currently remains fundamentally firm despite the government’s decision to increase the approved production quota. While production approvals have improved, immediate spot availability continues to remain constrained due to cautious producer selling, regulatory uncertainty and continued prioritisation of domestic supply obligations.

Demand from major Asian importing countries remains healthy, particularly for high-CV coal during the summer power generation season, while lower-CV coal continues to witness robust buying due to its economic advantage in blending applications. Consequently, supply-side constraints are currently outweighing the impact of higher production approvals, keeping export prices well supported.

Market outlook

Indonesia’s thermal coal market is expected to remain firm in the near term, supported by tight spot supply, steady Asian utility demand, and ongoing export policy uncertainty. However, upside may be limited if higher RKAB production boosts exports or Chinese import demand softens.

Leave a Reply