- Indonesian production surge causes regional supply shock

- High govt reserves help reduce Indonesia’s import reliance

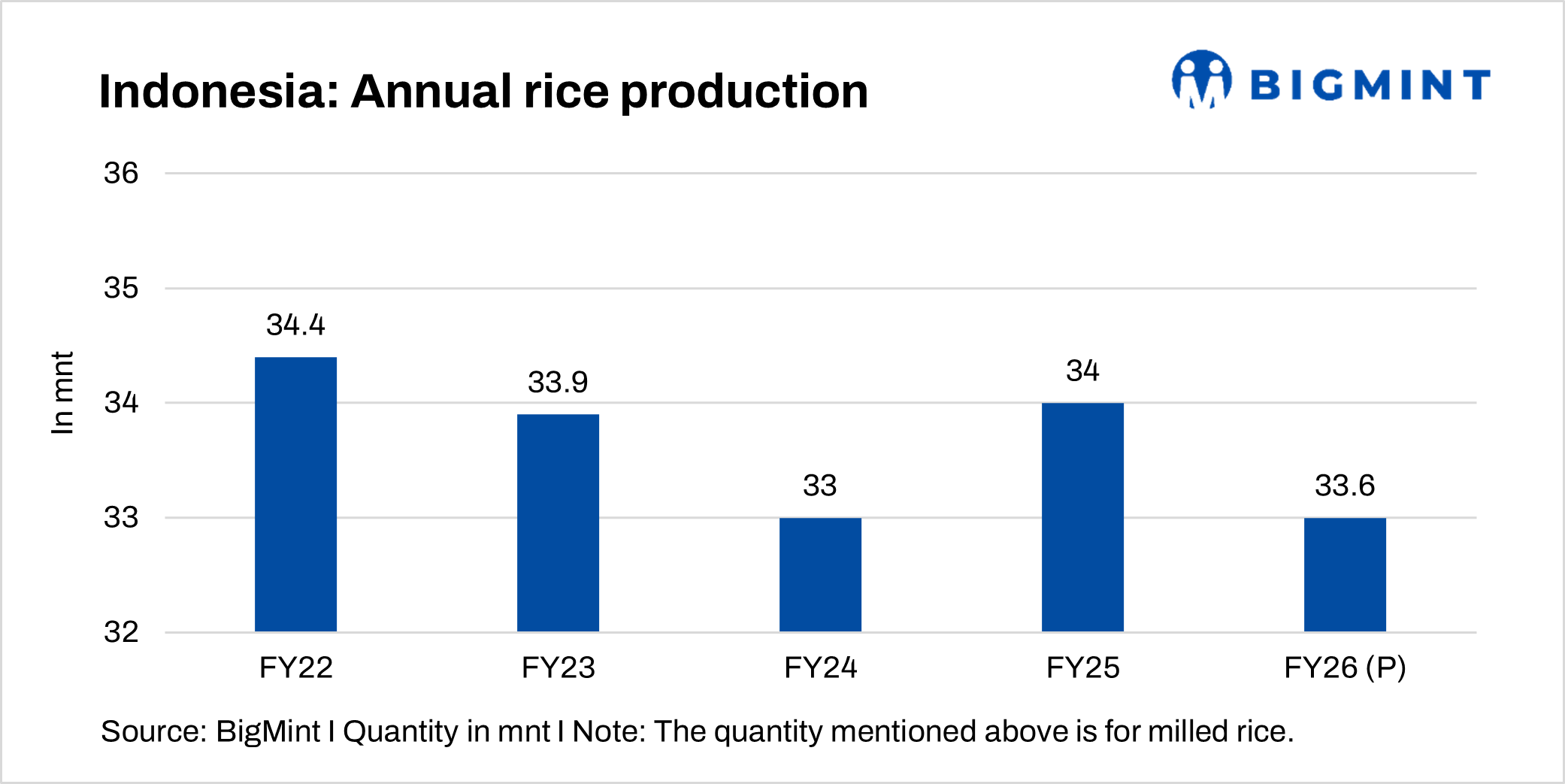

Indonesia’s agricultural authorities said this year’s harvest has delivered a “record” crop, helping relieve upward pressure on global rice markets. Speaking on 4 November, the head of the Badan Pangan Nasional (Bapanas), Andi Amran Sulaiman, noted that global rice prices have fallen from around $650/tonne (t) in the previous months to about $371/t in early November, attributing much of that fall to Indonesia’s production and reserve‐building efforts.

Indonesia’s harvest expansion comes amid government targets to phase out rice imports in 2025 and to maintain ample stocks to meet domestic demand. The government now reports a national rice reserve (Cadangan Beras Pemerintah, CBP) of 3.8 million tonnes (mnt), a buffer that could help stabilise both local and regional pricing.

Indonesia’s influence in the market

Traditionally a major rice-importing nation, Indonesia has shifted course with policies aimed at self-sufficiency. The government under Prabowo Subianto (President) is credited with directing resources to bolster domestic paddy production, milling throughput, and logistical infrastructure. Bapanas says these efforts now allow Indonesia to “play a major role in the global rice market.”

The elevated production and increased government reserves have had two key effects on the rice value chain. First, by reducing import dependency, Indonesia decreases foreign demand in world markets, taking pressure off global supply. Second, with stocks built up, the country can release supply into distribution channels as required, providing a stabilising influence on wholesale and international benchmark prices.

Market implications

The fall in benchmark rice (milled white rice) prices from roughly $650/t to $371/t signals a substantial shift in the global supply-demand balance. Indonesia’s production surge has effectively acted as a supply shock in the regional market, reversing or moderating recent price spikes. These shifts are particularly relevant for importing countries in Asia and Africa, where rice is a staple and cost pressures impact food security and fiscal policy.

For rice traders, millers and commodity analysts, the Indonesian case highlights how a major consumer-producer pivot (from import‐reliant to self-sufficient) can cascade into global markets. The ability of Indonesia to regulate its own production, reserves, and distribution may dampen volatility and ease margins for exporters and importers alike.

Challenges, outlook

Although the headline numbers appear strong, several underlying variables remain pertinent. Domestic consumption in Indonesia continues to grow, meaning production must consistently expand or efficiencies must improve to maintain the current export-reducing trajectory. The success of the Rice Price Control Task Force (set up to monitor producers, wholesalers, and retailers) will also be critical in ensuring that farm‐gate, milled, and retail prices remain aligned with policy objectives.

Moreover, global rice market dynamics depend not only on Indonesia but also on other major producers such as Thailand, Vietnam, and India, where policy changes, weather events, and logistical constraints can re-shape supply pathways. Observers will be watching whether Indonesia’s current buffer and policy stance can hold in the event of adverse weather or crop disease or if the country might again need to import and thereby re-tighten global supply.

Conclusion

Through strong production momentum and a sizeable government reserve, Indonesia is exercising newfound influence in the rice market, contributing to a notable decline in global benchmark prices. For the global rice trade, this marks a shift: the world is less reliant on import flows from Indonesia and more attuned to its ability to act as a stabiliser. That said, maintaining this dynamic will require consistent policy execution, agricultural resilience, and coordination across the value chain.

Leave a Reply