- Tight retail NAPP stocks lift offers despite weak demand

- Cement buying supports NAPP as petcoke competition intensifies

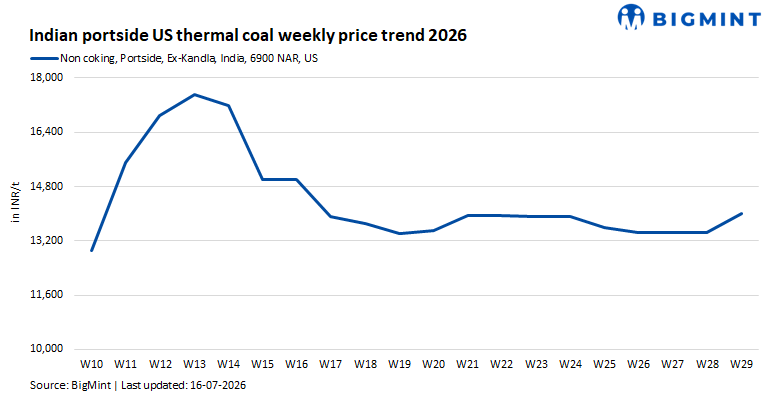

India’s US Northern Appalachian (NAPP) coal market has entered an unusual phase during the monsoon quarter. Portside lifting remains slow, industrial demand is seasonally subdued and international NAPP prices have been broadly stable. Yet domestic seller indications strengthened sharply in mid-July, with offers moving above INR 14,000/t after trading largely around INR 13,200-13,500/t only a day earlier.

The increase does not reflect a broad recovery in demand. Instead, it has been driven by tightening immediately available retail stocks, uncertainty over a disputed cargo, elevated replacement freight and concerns that some incoming tonnes may not reach the retail market. Meanwhile, direct industrial demand–particularly from cement producers–continues to provide relatively stable support.

Tight retail availability outweighs weak demand

The sharp rise in seller expectations has been driven by supply rather than consumption.

Combined NAPP stocks at Kandla and Tuna have fallen by 49.3% over the past three reporting weeks to 158,623 t, even as weekly retail lifting declined from 93,088 t to just 29,624 t. This suggests that replenishment into the retail market has lagged withdrawals, leaving traders with limited immediately available inventory despite subdued offtake.

The situation has been exacerbated by uncertainty surrounding a cargo involved in a contractual dispute. Until resolved, the material may not become available to the retail market as originally expected. Reports that some cargoes may have been diverted towards China have further unsettled sentiment, although these remain unconfirmed.

The result has been a widening bid-offer gap. Buyers continue to target the mid-INR 13,000/t, while sellers have lifted offers to INR 14,000-14,300/t in an attempt to protect scarce inventory and higher replacement costs.

Floating cargoes limit the shortage narrative

The current tightness should not be mistaken for a prolonged physical shortage.

Approximately 1.235 mnt of NAPP and ILB cargoes are scheduled to arrive in India during July and August.

However, much of this material is committed to industrial consumers, has yet to arrive, or may not be immediately available for retail sale. Consequently, today’s low port inventories do not necessarily reflect medium-term supply availability.

If even part of the unallocated cargo pipeline reaches the retail market, current tightness could ease relatively quickly.

Cement sector continues to underpin industrial demand

Industrial demand remains considerably healthier than the retail market.

Recent NAPP business has been concluded around US$134/t CFR west coast India, equivalent to approximately US$136/t CFR east coast India. Most recent purchases have reportedly originated from cement producers, reflecting their continuing need for imported high-CV fuels despite the seasonal slowdown.

At the same time, cement producers are becoming increasingly flexible in fuel procurement. Rather than relying predominantly on petcoke, they are optimising between imported coal, domestic coal, petcoke and alternative fuels depending on delivered economics and plant-specific operating requirements.

This flexibility means NAPP continues to compete not only with imported petcoke but also with improving domestic coal availability.

Petcoke remains NAPP’s principal competitor

The sharp correction in petcoke prices from recent highs has narrowed the gap between the two fuels.

US NAPP coal is currently priced at US$134–136 per tonne, with an assumed net as-received (NAR) calorific value of 6,900 kcal/kg, resulting in an estimated fuel cost of US$19.4–19.7 per GCal.

High-sulphur petcoke is priced at US$136.5–141 per tonne, with an assumed NAR of 7,500 kcal/kg, translating to a lower fuel cost of US$18.2–18.8 per GCal.

However, purchasing decisions are no longer based solely on headline fuel cost. Sulphur limits, kiln chemistry, operational flexibility, domestic coal availability and blending requirements increasingly determine fuel selection. As a result, NAPP continues to retain a place within cement producers’ fuel portfolios despite petcoke’s calorific advantage.

Replacement costs remain supportive

International NAPP prices have remained broadly stable, with FOB Baltimore assessed at US$86.75/t, indicating that the recent increase in Indian offers has not been driven by a rally in US coal prices.

Instead, replacement economics continue to be influenced by elevated freight. USEC-India Panamax freight has risen to US$52/t, while freight for US Gulf Coast petcoke cargoes remains considerably higher. These logistics costs discourage traders from aggressively discounting remaining portside inventory.

Outlook

The Indian NAPP market is likely to remain characterised by firm seller expectations but subdued transaction volumes through the remainder of the monsoon quarter.

Current strength reflects tightening retail availability rather than stronger underlying demand. Low port inventories, uncertainty over a disputed cargo and elevated replacement costs have supported offers even as lifting remains weak.

At the same time, the sizeable July-August cargo pipeline suggests that today’s tightness may prove temporary if additional material becomes available for retail sale.

Industrial demand from cement producers should continue to provide a stable outlet for imported NAPP, although competition from petcoke and domestic coal will remain intense. Consequently, the sustainability of recent price gains will depend less on demand recovery and more on how quickly fresh cargoes replenish the retail market and whether current supply disruptions are resolved.

Leave a Reply