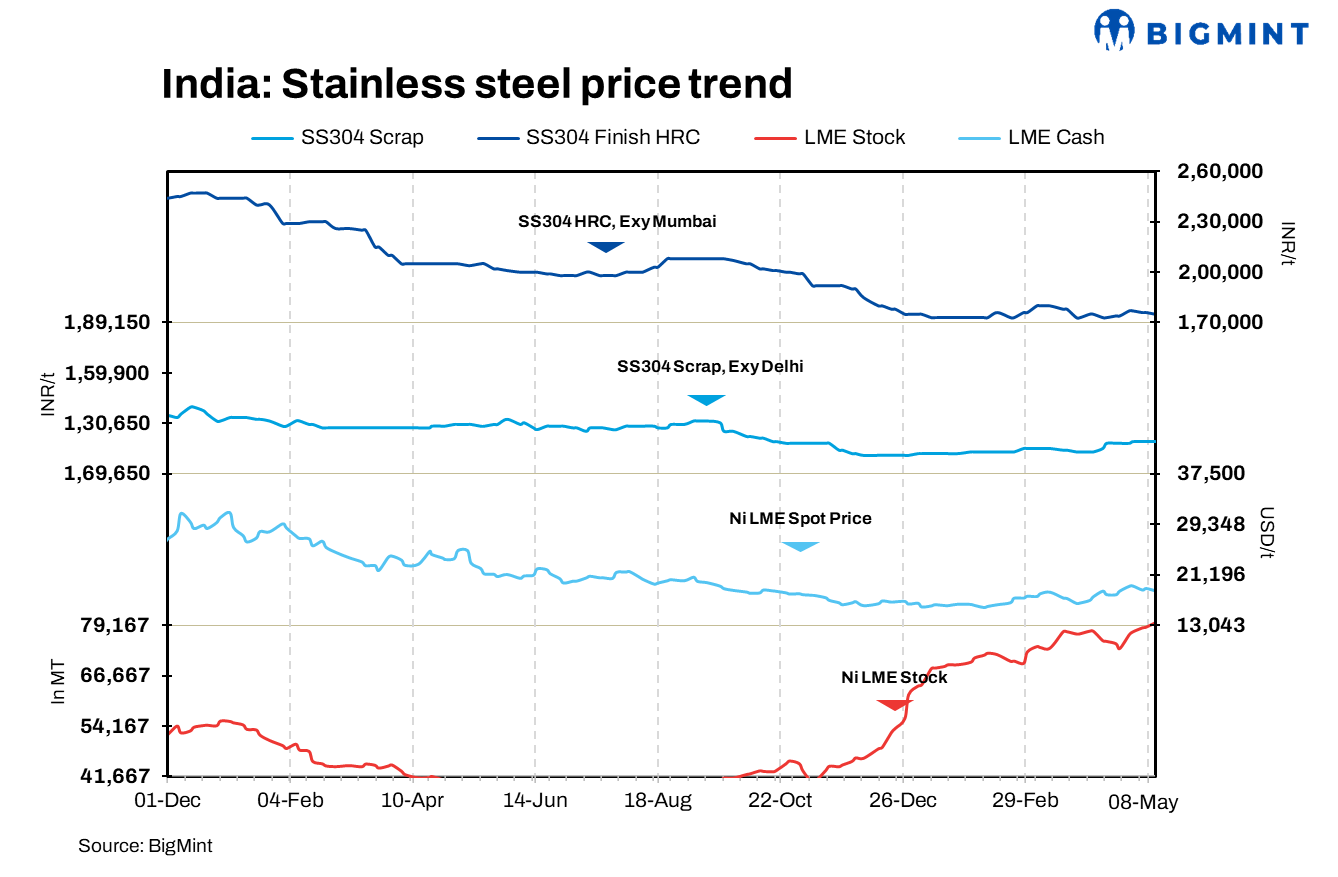

In India, finished stainless steel prices have mostly stayed stable this week, with a slight decline seen which can be linked to a minor decrease in LME nickel prices. Scrap prices in the domestic market have remained steady, while imported scrap prices have experienced a minor decrease w-o-w.

The marginal drop in finished product prices can be attributed to a drop in nickel prices on the LME, which fell by $650/t w-o-w. Nickel prices for 3-month delivery on LME saw a 3.4% decrease, reaching $18,600/t, at the time of reporting. Notably, nickel stocks in LME warehouses increased by 1.7% compared to the previous week, reaching 79,896 t.

India’s stainless steel 304 HRC prices stood at INR 175,000/t ex-Mumbai and domestic 304-grade scrap prices stood firm at INR 120,000/t ex-works Delhi, BigMint’s assessment revealed.

Scrap market

In the local scrap market, prices for 304 scrap have remained unchanged, ranging from INR 119,000 to 121,000/t ex-Delhi NCR, with cash payment terms. Sources indicate that key mills are acquiring 304 scrap at around INR 121,000 to 122,000/t DAP, with a credit period of 45 days.

A trader informed BigMint, ” The market is slow with no major bookings. At the moment only the larger mill-based buyers are active in procuring scrap in the domestic market.”

This week, there has been a minor adjustment in imported offers, with BigMint’s assessment indicating prices for 304-grade scrap at levels ranging from $1,400 to $1,410/t. Offers from the Far East region are reportedly at $1,420 to $1,430/t, while bids are at levels of $1,400/t CFR Mundra.

Prices of 316-grade scrap were observed to be at $2,565/t CFR Mundra. Although there was a slight decrease, market demand and purchasing interest have stayed subdued. Furthermore, offers for 430-grade scrap obtained from nearby locations are available at $650-$670/t.

Offers of SS 304 scrap of Middle East-origin stood at $1,440-$1,460/t, while 316 stood at $2,570-$2,580/t CFR Mundra.

Finished flat segment

As per BigMint’s assessment, 304 HRC is priced at INR 175,000/t, while 316 HRC stood at INR 306,000/t, ex-Mumbai.

According to a buyer source, “There is a prevailing trend of minimal activity in the market, driven by downward pressure on demand, primarily influenced by fluctuating LME nickel prices. Buyers are exercising caution and opting for a “wait-and-see” approach to gain better clarity on existing market dynamics.”

Additionally, SS 304 pipe prices were heard at INR 194,000-196,000/t, while SS 316 pipe prices stood at INR 325,000-330,000/t ex-Mumbai.

Meanwhile, imported offers of SS 304 HRC from China are currently at $1,880-$1,900/t CFR Mundra, India. China’s offers for SS 304 HRC remained stable as the market resumed activity following the holiday period, albeit at a slow pace.

Finished long indicative levels

In the finished long segment, price indications for 304 black round bars have been heard at INR 167,000-169,000/t, exw-Delhi. Additionally, price levels for SS 304 bright bars were heard at INR 190,000-INR 192,000/t levels, ex-Delhi.

Indicative offers levels for SS 304 hexagon stood at INR 201,000-202,000/t and SS 304 angles are at INR 195,000-INR 197,000/t, both ex-Delhi.

A manufacturer source said, “The drop in LME nickel prices have still not had any major effect on the longs product segment. However, it is anticipated the prices might see a INR 1,000-INR 2,000/t downward correction in the coming days.”

China market overview

During the week, China’s domestic stainless steel prices witnessed stability. Prices of 304 grade CRC reached RMB 14,500/t ($2,002/t) ex-works. FOB prices of 304 grade CRC stood at $2,079/t.

The stability in prices can mainly be attributed to the extended Labour Day holidays from 1-5 May, which resulted in the closure of both the SHFE and domestic markets. Additionally, the Chinese market has resumed activity after the holidays, but at a slow pace.

As per sources, China’s refined nickel production reached 24,912 t in April, marking a 2.05% increase compared to the previous month and a substantial 40.87% increase y-o-y. The total production for January-April amounted to 96,481 t, showing a notable 44.18% rise from the previous year.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices rose by INR 116,500/t (tonne) ($1,395/t) w-o-w in comparison to the previous assessment on 1 May. The price increase was reportedly the result of material shortage in both the domestic and international markets.

As per BigMint’s assessment on 8 May, Indian ferro molybdenum prices were at INR 2,612,500/t ($31,285/t) exw-Nagpur on a 60% pro rata basis.

Ferro chrome: Indian ferro-chrome prices (HC, FeCr60%) stood at INR 107,700/t exw-Jajpur. Prices witnessed a marginal drop of INR 200/t w-o-w.

Recent updates

- EU extends Indonesian CVD measures

The European Commission extended Indonesian countervailing duty (CVD) measures to imports of SSCR flat products from Taiwan, Turkey, and Vietnam, with a 20.5% duty rate on Indonesian SSCR and an extension of the 19.3% antidumping duty to include Taiwan and Vietnam. Eight companies were granted exemptions subject to monitoring for potential abuse.

- Indonesia asserts nickel reserve sufficiency

Indonesia’s nickel reserves are projected to support processing industries for decades, with high-grade reserves estimated until 2035 and low-grade until at least 2069. The ban on nickel ore exports in 2020 drove investments in nickel pig iron and EV battery materials. There are calls for diversifying smelter production amid concerns over oversupply and potential depletion of high-grade ore.

Recent deals

A deal for 100 t of SS 304 HRC was concluded at INR 175,000, ex-Mumbai.

Around 500 t South America origin of SS 446 scrap was sold at $840/t, CFR Mundra.

Outlook

Stainless steel prices are anticipated to correct in the coming weeks due to decreased demand pressure, influenced by market uncertainties arising from the decline in LME nickel prices.