- Leading coil producer cuts 300-series prices for November.

- BigMint’s assessment for 304-series HRC drops w-o-w

The domestic stainless steel market remained subdued this week amid continued weak demand in the finished segment.

Additionally, India’s leading stainless steel coil manufacturer reduced prices of its 300-series products, effective 3 November. The adjustment follows a temporary relaxation on imports, allowing the use of non-BIS-compliant material until 31 December. Consequently, 304 coils prices were reduced by INR 6,000/tonne (t) ($67/t) and 316 coils by INR 9,000/t ($101/t). This is the first price revision for November.

Finished flats prices drop

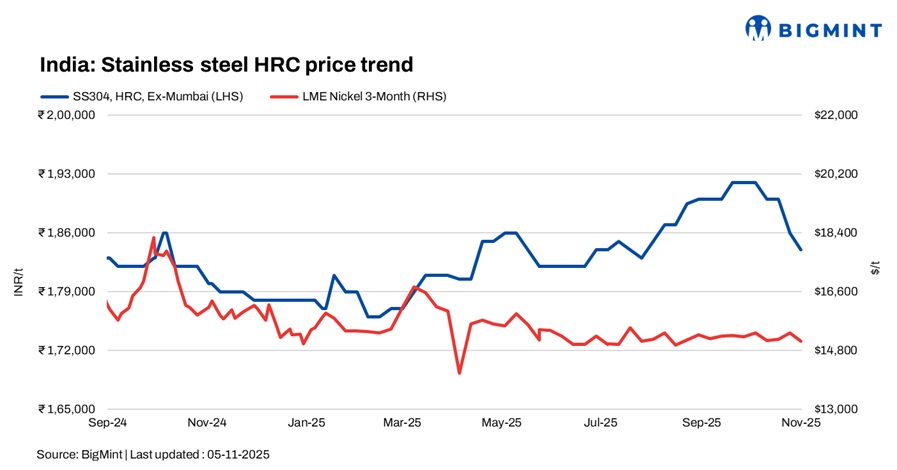

BigMint’s benchmark assessments for stainless steel (304 series) HRC stood at INR 184,000/t ex-Mumbai, down by INR 2,000/t w-o-w.

A mill source said, “Market activity remains sluggish. Actual transaction prices are below listed list prices due to abundant supply and muted demand. Overall sentiment is weak, and many suppliers are actively reaching out to secure orders.”

Similarly, BigMint’s SS 316 HRC was assessed at INR 340,000/t ex-Mumbai, down INR 3,000/t w-o-w.

A market participant said, “Demand has shown slight improvement from auto and infrastructure, but inventories in the trade segment remain heavy. With BIS norms relaxed, import pressure has returned. Around 6,000–8,000 t have reportedly been booked from Malaysia and Vietnam. However, after recent price cuts, landed import costs are nearly at par with domestic prices.”

Another market participant said, “In the Mumbai market, certain sizes are currently short due to delays in incoming shipments, although overall supply remains comfortable.”

Finished longs tags soften w-o-w

The domestic stainless steel longs market remained weak, with expectations of gradual improvement by late November as downstream operations normalize and construction activity picks up.

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars were at INR 156,000/t, ex-Mumbai, meanwhile, SS 316L black round bars were at INR 276,000/t, ex-Mumbai, both down INR 1,000/t w-o-w.

Export sentiment for SS longs to Europe remains cautious; while inquiries exist strict quality norms and price competition from Southeast Asian suppliers are limiting large bookings.

Indicative FOB prices for stainless steel longs, with Indian 304 bright bars at $2,050-2,100/t and 316 bright bars at $3,550-3,570/t, while Vietnam’s 304 bright bars are quoted at $1,850/t and 316 bright bars at $3,300/t. On the other hand, Europe domestic stainless steel 304 bright bars’ indicative levels were heard at $2,800-2,850/t and 316 bright bars were heard at $3,600-3,700/t.

LME nickel tags slip w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,100/t, down 1.7% compared to last week’s $15,355/t. Nickel stocks at LME-registered warehouses stood at 252,750 t, up slightly compared to 251,436 t t in the previous week.

Chinese stainless steel & NPI prices

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,500/t ($1,893/t) exw, while FOB tags of 304-grade CRCs were firm at $1,900/t.

Chinese portside prices of nickel pig iron (NPI) (8-12%) were at RMB 920/t ($129/t). Meanwhile, Indonesian FOB prices of NPI (10-14%) stood at $114.69/t.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices stayed largely stable last week, edging down slightly by INR 10,000/t ($113/t) as compared to the assessment on 29 October. The slight drop was likely due to weaker global prices, especially in China. However, the Indian domestic market was not much affected from it.

Ferrous scrap: India’s imported ferrous scrap market stayed muted amid weak buying interest and unworkable offers. Mills preferred domestic scrap as shredded hovered around $350/t CFR and HMS at $320–330/t. Limited deals were heard near $323/t CFR, while sluggish steel demand and falling sponge iron prices kept overall sentiment bearish.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 1,000/t w-o-w to INR 118,000/t ($/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices witnessed a slight uptick of INR 900/t ($10/t) as compared to the previous assessment on 27 October. Prices increased following the announcement of Bhutan’s November offers at INR 88,000/t ($994/t) exw, reflecting a slight increase m-o-m.

Ferro silicon prices in India were at INR 88,000/t ($994/t) exw-Guwahati, as per BigMint’s assessment on 3 November. In Bhutan, prices edged up by INR 400/t ($5/t) w-o-w to INR 88,000/t ($994/t) exw.

Outlook

The stainless steel market is expected to remain under pressure in the near term amid weak demand and ample supplies in the domestic market, and with import competition re-emerging, further price softening appears likely.

Leave a Reply